Today’s Chinese biopharmaceutical firms offer a major opportunity for both multinational companies (MNCs) and local companies. Thanks to a decade of sustained government support—including policy reform, talent development, and funding—China is now vying aggressively with MNCs for domestic market share in the innovative drugs sector. Over the next five to ten years, these homegrown companies will continue to improve their innovation capabilities and eventually compete directly with MNCs outside of China—even in Europe and the US.

Indeed, as the world’s second-largest market after the US, and the only major market expected to grow in the high single digits annually over the next five years, China deserves close scrutiny by MNCs. By cultivating a detailed understanding of how China’s biopharma industry is developing, MNCs can begin to map a strategy for tapping into the country’s growth and innovation.

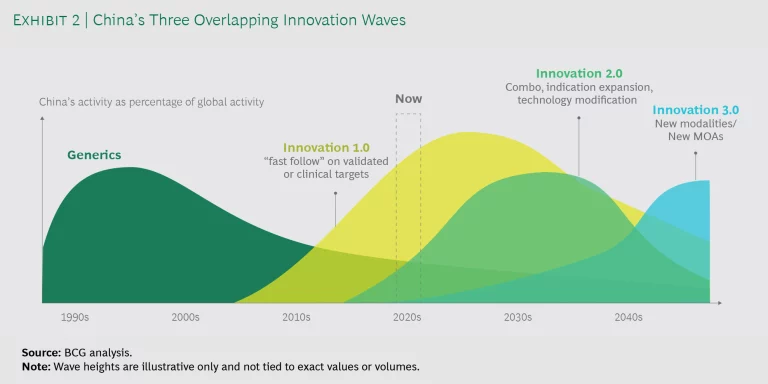

To this end, BCG has conducted an in-depth study of the Chinese biopharma industry. We found that innovation in the country is occurring in three powerful waves, which are overlapping for the first time and will reshape the global biopharma landscape.

Structural Changes Beget New Companies

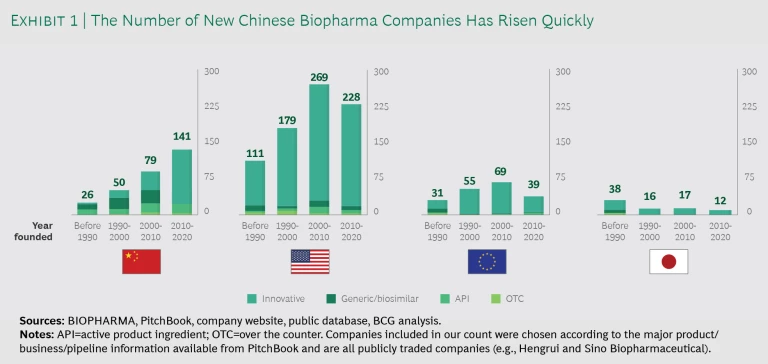

The number of new Chinese biopharma companies has risen steadily over the past three decades, accelerating dramatically in the last ten years. While company formation declined in other major markets such as the US, Europe, and Japan, more than 140 new biotech companies emerged in China from 2010 to 2020. (See Exhibit 1.)

Such accelerated innovation and company formation grew partly from pent-up domestic demand in what’s become the world’s second-largest biopharma market—one whose demographic is aging dramatically, with increasing prevalance of many diseases including cancers, cardivascular diseases, and diabetes. In additon, some c ancers such as gastric, HCC, and esophageal, and diseases such as HBV, are more prevalent in China than in the West and so haven’t received the same attention from Western MNCs.

While company formation declined in other major markets such as the US, Europe, and Japan, more than 140 new biotech companies emerged in China from 2010 to 2020.

While competition and the Chinese government’s contract negotiations will hold down prices that companies can charge for even their most innovative drugs, the sheer numbers of patients in China makes the market very attractive for companies that win bids and are listed on the government’s National Reimbursement Drug List. These demographic and demand trends have created an opportunity for domestic biopharma to pursue innovation in China for China, which dovetails nicely with the Chinese government’s focus on the industry over the past decade. Tellingly, in its last two five-year plans, the Chinese government named biopharma as one of eight key strategic industries to develop. Four structural changes underpin that development.

Funding. More and more private capital is available to the industry through venture and private equity (PE) funds, which underwrite most R&D in China. (Note that such funding helped the US leapfrog the EU 30 years ago.) Government and institutional funding through the China National Science Foundation and government grants are also channeled through PE firms and are an important source of funding. Today, China has the second-highest funding globally, although the US still leads by a siginficant margin: $212 billion vs. China’s $60 billion—adjusted for purchasing power parity—in 2018-2019.

More and more private capital is available to the industry through venture and private equity (PE) funds, which underwrite most R&D in China.

This surge in private funding has coincided with the development of public markets and the promise of lucrative “exits” through IPOs. Early stage pharmaceuticals, even pre-revenue companies, can now access public capital, expanding the R&D funding pool. Moreover, pharmaceutical companies listed in the mainland and Hong Kong exchanges show higher valuations than those listed in the US, providing a strong public capital source for R&D. All this means that biopharma companies in China have access to some of the cheapest capital in the world.

Policy. Over the past five years, China has enacted several policies explicitly to improve market access and support innovation. The government has worked to significantly ease the registration process for innovative drugs and harmonize the approval process with global norms. For example, in 2011 it took 31 months to get a clinical trial application approved in China; by 2018 it took just two months. And since 2017, the government has held national contract negotations for high-priced innovative drugs, which previously had limited to no access to public insurance reimbursement.

Infrastructure. The Chinese government has also supported the development of science parks and city hubs for innovation and R&D by offering land to developers on very attractive terms. From 2016 to 2020, the number of biotech science parks grew 50%—from about 400 to about 600—and the total value of their output has grown by more than 80% in that time.

More than 75% of the top talent in China have at least five years of overseas research experience.

Talent. China’s talent pool is still smaller than in the US, but it’s rapidly expanding as local talent continues to develop and Western-trained scientists steadily return. Returnees have been without question the key driver behind the formation of innovation companies in China over the past ten years. More than 75% of the top talent in China have at least five years of overseas research experience. While the government has actively encouraged their return, the attractive market dynamics have already superceded government incentives.

Three Waves of Chinese Innovation

How exactly is the biopharma industry developing in China? That’s a key question for MNCs that wish to understand the opportunities and challenges and formulate an effective response, especially given the flurry of company formation, local demand, and structural changes taking hold in the country. For example, should MNCs continue to compete with only their own global pipelines in China (pipelines often not best suited for China)? Or should they invest and find ways to participate in local innovation to complement their global portfolios?

To help MNCs answer these and other questions about the Chinese biopharma market, BCG conducted an in-depth study of the industry. We found that innovation in the country is occurring in three distinct phases: from monotherapy “me-too” and “me-better” companies, to indication

Before these three innovation waves, and until about ten years ago, generics dominated China’s biopharma landscape. Since then, China’s biopharma industry has transformed from essentially a generics industry to one focused on many novel products and technologies. In fact, legacy generic players are also becoming more innovative. Several have more than half their pipelines targeting innovative biologics or are tapping into novel modalities, such as cell therapies.

China’s biopharma industry has transformed from essentially a generics industry to one focused on many novel products and technologies.

The question is not whether China will be an innovative force in biopharma in the future—but when. Let’s take a closer look at the three waves of Chinese innovation.

Innovation Wave 1.0. Starting in the early 2000s, a first wave of new generation innovative pharma companies formed in China. Focused on being fast followers for me-too and me-better drugs, they sought new molecules on validated or late-stage clinical targets or combination therapies. As this innovation wave continues, the focus is shifting more toward me-better innovations. For example, more than 50 Chinese companies are focused on

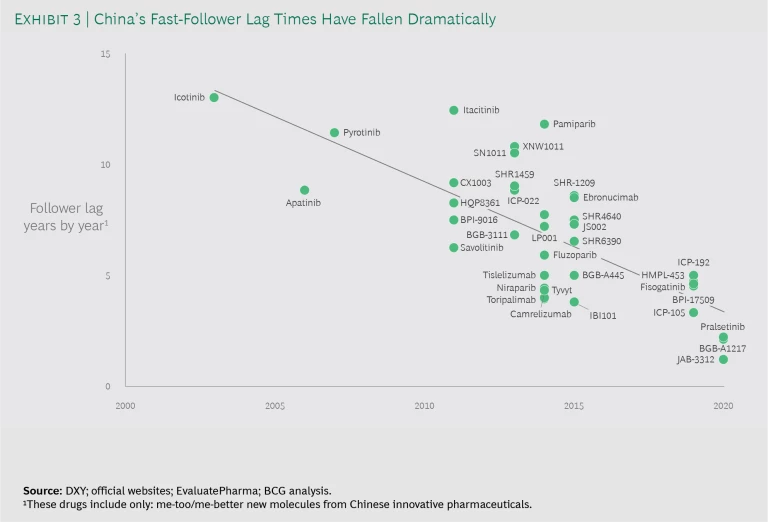

The competition among fast followers in China has dramatically reduced the time between global first-in-class (FIC) and fast followers. Three factors are helping China to close the timeline gap. First, Chinese biopharma are developing compounds earlier—and thus taking on more risk—to follow the FIC players more quickly. Second, China has streamlined approval timelines. For example, the average time between IND application and approval has shrunk from 10 months for me-too companies before 2015, to about 3.8 months since then. Third, China’s pharma companies can execute trials faster, thanks to more mature trial recruiting and execution systems. (See Exhibit 3.)

Going forward, we expect the fast-follower trend to persist. New targets discovered in the US, Europe, and Japan will continue to fuel market opportunities for Chinese biopharma to bring “lower priced” innovative drugs to market.

Innovation Wave 2.0. Beginning around 2016, we began to see more activity in original indication expansion, combo therapies, and novel antibodies (such as bispecific, fusion proteins, and ADC). These areas, while still not FIC, demand more risk taking than simply being a fast follower. These areas also demand more innovation expertise, from hypothesis to clinical translation. As China deepens its understanding in areas such as oncology pathogenesis, biological mechanisms, and antibody engineering, we expect this progress to continue.

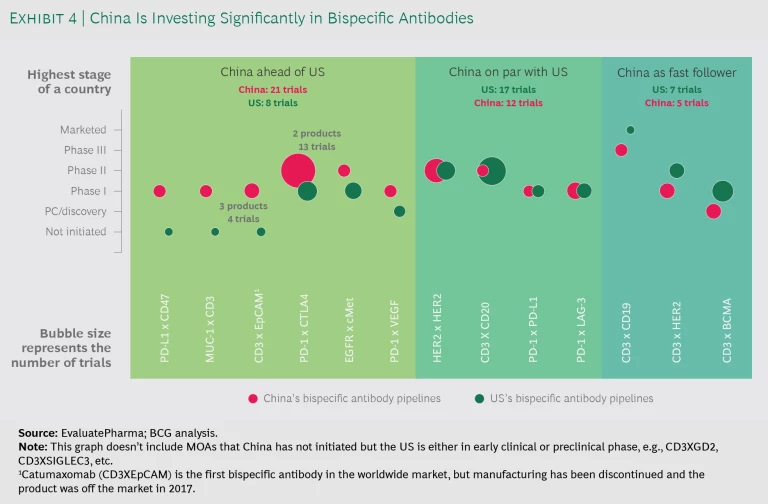

- Novel Antibodies. China is increasingly leading the exploration of novel antibodies, particularly on bispecific antibodies. Among the 13 combinations China is currently exploring, 10 are in an advanced stage or on par with worldwide efforts. (See Exhibit 4.) China’s innovation on bispecific antibodies is not limited to new combinations of targets, but includes platform technologies crucial to the success of bispecifics. Among biopharmas pursuing bispecific monoclonal antibodies in China, 12 have original technologies to improve the function, stability, and safety of bispecific antibodies. Some have licensed the platform technologies to global companies.

- Indication Expansion. As noted earlier, local firms are pursuing “China for China” innovation. This has yielded some original indication expansions in oncology. For example, local pharma has explored three original PD-1 indication expansions in areas with high unmet needs (such as nasopharyngeal carcinoma, advanced HCC, advanced esophageal squamous cell carcinoma), with promising study results (for example, 100% objective response rate for nasopharyngeal cancer). With more oncology me-too, me-better, and combo companies succeeding, we believe original indication expansion activities will dramatically increase in the next few years.

- Biologics Combos. After the launch of the first PD-1 in China in 2018, biologics combo activity worldwide has grown exponentially, with 75% of activity focused on immuno-oncology (IO) combos. China is following a similar pattern, although its biologic combo activity lags MNCs in both the number of targets and the novelty of mechanisms of action (MOAs). For example, local pharma focus more on combos with mature MOAs that include more than one targeted therapy and usually chemo. This is partially driven by the fact that China’s activities on other IO targets are still at an early stage, which impairs the country’s ability to conduct biologic combos in more advanced mechanisms. But some Chinese pharma companies are seeking ways to collaborate with MNCs to mitigate this.

China is increasingly leading the exploration of novel antibodies, particularly on bispecific antibodies. Among the 13 combinations China is currently exploring, 10 are in an advanced stage or on par with worldwide efforts.

Innovation Wave 3.0. The most recent and advanced level of innovations involves completely new MOAs or novel technologies. Though still early, we see some Innovation 3.0 activities occurring in China. These activities have focused on cell therapies and gene editing, where thanks to a supportive regulatory environment for investigator-initiated trials in some novel modalities, China has the potential to leapfrog other countries. For example, China has been actively conducting clinical trials with the gene-editing technology CRISPR (clustered regularly interspaced short palindromic repeats), most of which are conducted by academic professors or hospital principal investigators. The US and Europe pushed the frontier of scientific discovery for CRISPR. But China, after being almost completely absent in the basic science aspect, has seized the headlines by leading the application in human trials.

The most recent and advanced level of innovations involves completely new MOAs or novel technologies.

To truly excel in these new frontiers, China will need a strong translational capability as well as a deeper understanding of basic science and molecular mechanisms. But China is catching up to world leaders, evidenced by the growth in the number of articles published in high-profile biomedical journals. Another sign of increased innovation is the number of patents filed from China. From 2014 to 2017, China’s biomedical-related patents increased at a compound annual growth rate of 16%, way ahead of the US (3%) and European countries, such as France (3%) and the UK (6%). For cell therapy patents specifically, China is leading in both growth and absolute amount. From 2014-2017, China’s patents increased 40% to 1,264, while in the US patents increased by 14% to 600.

Over a longer time horizon, we expect China to develop original new MOAs/technologies in selected areas. But in the near term, Innovation 1.0 and 2.0 will account for a large part of biopharma R&D activity in China, with many commercial products coming to market in the next five to ten years.

Going Forward

There’s little doubt that MNCs with long-term global ambtions need to be in China. It’s already the second biggest market, with its own specific therapeutic needs and opportunities, and innovation is decidely on the upswing. An MNC might choose to collaborate in local R&D through different structures (such as JVs, alliances, or co-development by molecule). Or it might contribute to the innovation ecosystem in other ways, such as setting up incubators to help local companies accelerate their development. Perhaps it could even help local companies begin to market their products globally.

There’s little doubt that MNCs with long-term global ambtions need to be in China. It’s already the second biggest market, with its own specific therapeutic needs and opportunities, and innovation is decidely on the upswing.

Consider what’s happened with COVID-19. Within eight months, China generated six original vaccines and six antibody candidates that entered clinical trials. One of them, from Shanghai Junshi Biosciences (TopAlliance), has been licensed by Eli Lilly for outside-China rights—with a price tag of more than $250 million. It is currently in Phase II in the US and Phase I in China.

Each MNC’s China strategy will be specific to its own circumstances and expertise, but it’s critical to begin mapping this strategy immediately. The three waves of Chinese innovation will continue to break over the global biopharma industry for decades to come, and these homegrown companies will eventually compete more aggressively with MNCs inside and outside of China. For long-term success, every MNC will need to decide how best to ride China’s innovation waves.