Last year was a turning point for sustainability in the fashion industry . Our 2018 Pulse of the Fashion Industry report found that 75% of fashion companies improved their score in 2017 compared to 2016, raising the pulse of the industry by six points. This is an impressive and encouraging development. However, more needs to be done.

The fashion industry has a responsibility to continue to improve its environmental and social performance. As a large and creative industry, it has a vital interest in securing a prosperous and sustainable future. Environmental and social stresses are enormous and continue to grow, in line with customer demand . In addition, consumer behaviors and rapidly evolving technology will soon shape and challenge the industry in unpredictable ways. It is undeniable: the industry has to adapt.

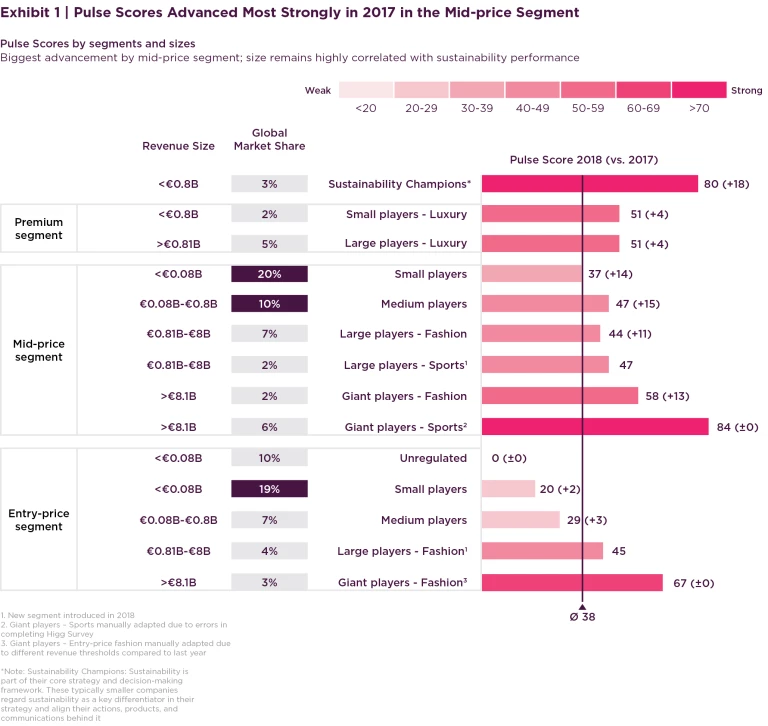

The direction is set. Almost half of the fashion players (as gauged by market share) indicates that laying the foundation for change and initiating action can boost Pulse Scores, a performance measure of the sector developed by The Boston Consulting Group (BCG) and the Global Fashion Agenda (GFA), and powered by the Sustainable Apparel Coalition’s Higg Index. Companies in the mid-price segment drove most of this year’s improvement in Pulse Scores, evidence that moving to better practices has reached the mass market and is no longer a question of values or a privilege of large companies’ resources. Even some smaller companies gained strong momentum and are beginning to catch up to the frontrunners.

ROOM FOR IMPROVEMENT

Progress at the very top and among the weakest performers has lagged, however, for different reasons. Many strong-performing giant companies and luxury players are finding further advances increasingly difficult to achieve. At the same time, about one-third of the fashion industry has yet to take action.

The Pace of Change Doesn’t Go Far or Fast Enough

Putting fashion on a path to long-term financial, social, and environmental prosperity will require more than individual companies realizing incremental improvements. Now the industry’s leaders need to actively collaborate on and clearly commit to prioritizing a responsible long-term strategy, despite the pressure to generate positive quarterly results.

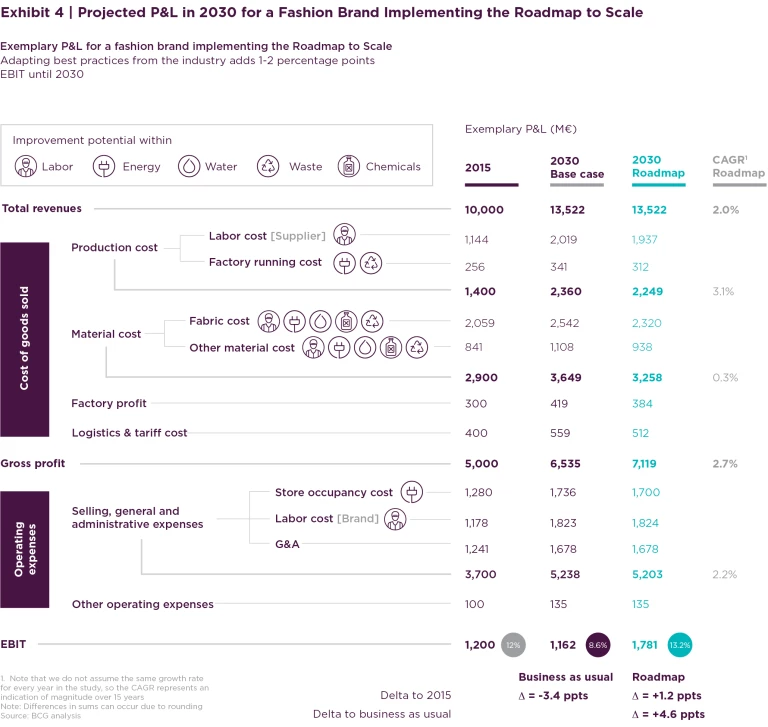

This year’s report aims to offer guidance to companies looking to start or find further advances toward more responsible ways of doing business, by sharing proven best practices and defining bigger and bolder steps the industry must take. Taking action not only improves the social and environmental performance of the industry, but results in a strong business case – raising the EBIT margin by 1 to 2 percentage points.

Building on the Pulse Score, BCG and GFA worked with leading fashion players to develop two important frameworks for guidance and inspiration: the Pulse Curve and the Roadmap to Scale. The Pulse Curve, enables companies to compare their actions and performance against other industry players and evaluate their progress over time. The Roadmap to Scale, is an inspiring guide that offers concrete actions that companies can take to prioritize and plan sustainability efforts.

Building a Better Industry Takes Collaboration

Given the pace and magnitude of change, leveraging existing solutions and best practices will not be enough. Frontrunners are already reaching these limits and experiencing a leveling-off of impact. These companies are blazing the trail for the rest of the industry, so their continued progress is critical. To regain momentum, they must find innovative solutions and explore different business models.

Individual companies recognize that they cannot create this disruptive change on their own. The industry as a whole must develop partnerships and ecosystems that can commercialize and scale the most promising innovations on the horizon. This type of collaboration is what will achieve the speed of change needed to boost the fashion industry’s long-term environmental and social performance—and profitability.

THE PULSE OF THE INDUSTRY

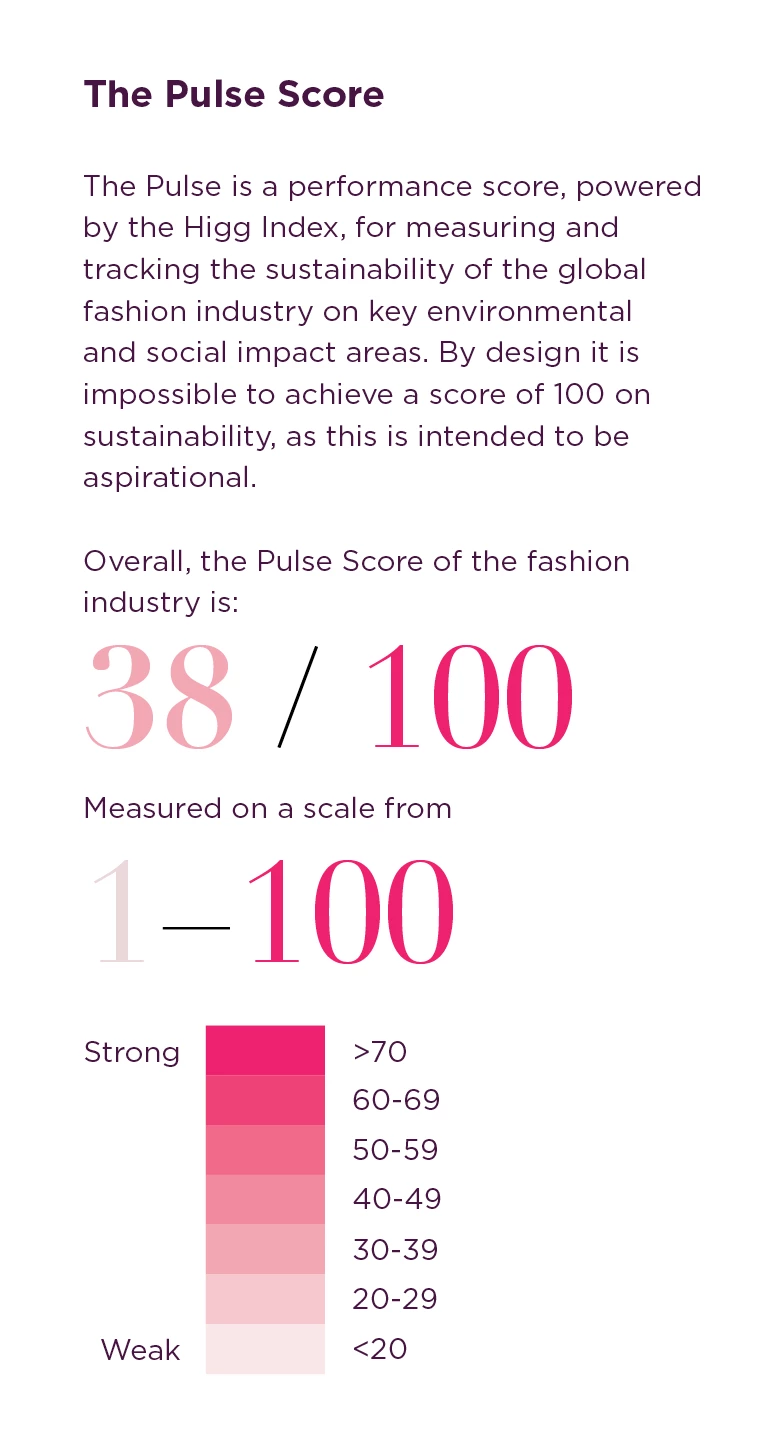

In the past year, the fashion industry’s Pulse Score improved from 32 to 38 (out of 100). The Pulse Survey, representing all industry segments, confirms that the topic is rising on the industry’s agenda. Of the executives polled, 52% reported using sustainability targets as a guiding principle for nearly every strategic decision they made—an 18-percentage-point increase from last year.

Nearly all of this year’s progress came from companies in the mid-price segment. (See Exhibit 1.) Because this segment accounts for almost half of the industry by revenue, progress here is encouraging. However, other industry segments showed little progress in addressing their environmental and social footprints. Small and midsize enterprises in the entry-price segment have not performed well; in fact, 2017’s report found that they represented a blind spot in addressing sustainability. They are likely unsure about where to start with these complex issues. Size continues to be a major determinant of performance on sustainability for the industry as a whole.

The largest companies and sustainability champions remain in the lead. But the largest companies’ Pulse Scores have not risen as much as the industry on average, a clear indication that they’re finding it harder to make the large leaps of progress they made in the past. These diminishing returns are not from lack of effort or progress within existing initiatives, but rather from the lack of scalable and commercially viable technology solutions, as well as from pain points in global infrastructure and regulation.

The overall increase of the Pulse Score is reflected in the value chain. Last year’s most advanced steps (processing, manufacturing, and transportation) continue to be the strongest areas. But weaker steps, such as design and development and end of use, saw the biggest gains this year and have narrowed the gap—a promising turn of events.

Here, too, incremental improvements, though good, are not proceeding fast enough. The ambition should be to raise the Pulse Score by well more than six points per year—and that entails going beyond small improvements to generate disruptive change at a much greater speed, applying existing technologies more broadly, and adopting and scaling next-generation innovation to the fullest extent possible.

The overall Pulse Score gap from 38 to 100 indicates the size of the industry’s opportunity to create new value for society and individual businesses.

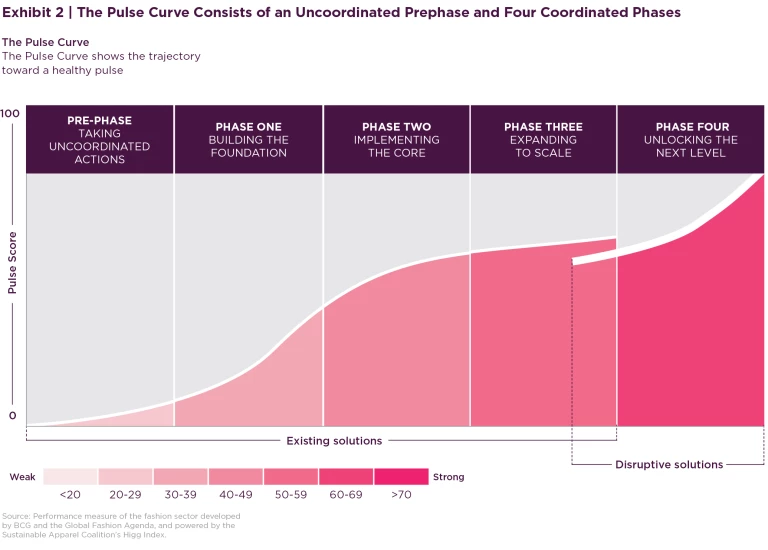

THE PULSE CURVE: TRAJECTORY TOWARD A HEALTHY PULSE

This year’s Pulse Report aims to share existing best practices and proven solutions, as guidance to the industry as a whole. In extensive interviews, advanced industry players identified the actions they took to achieve their gains. We found that most companies’ sustainability journeys follow a similar pattern, in which environmental and social performance improve in phases. Building on those insights, we created the Pulse Curve, which charts the trajectory from a company’s first steps toward improved performance to its implementation of the most advanced practices. (See Exhibit 2.) Industry players can use the Pulse Curve to assess and accelerate their own journeys, deploying the frontrunners’ lessons. The process is ongoing: as industry leaders continue to experiment and advance, the rest of the industry learns from them, moving the whole industry to better practices.

The Pulse Curve begins with a pre-phase, in which a company takes uncoordinated action before developing a clear strategy, and then progresses through four phases. At the beginning, a company’s movement along the curve is almost flat. Entry-level companies displaying the lowest Pulse Scores cluster in this section. The curve rises along with increasing Pulse Scores as companies set strategies and targets. They begin to reach the next level as they implement collaborative initiatives and improvement measures in their value chains. As they work with partners along the supply chain to introduce efficient production techniques, improve working conditions, and adjust their sustainable materials mix, brands and retailers continue to progress upward along the curve.

At a certain point, however, improvement tends to level off, as companies reach the limits of available technologies and infrastructure. To unlock the next level, companies must collaborate with other stakeholders, driving systemic change through bold leadership and creating innovation ecosystems that lead to the disruptive technologies truly needed.

SCALING UP EXISTING SOLUTIONS

Successful scaling is critical to improvement at this stage of development.

The Roadmap to Scale

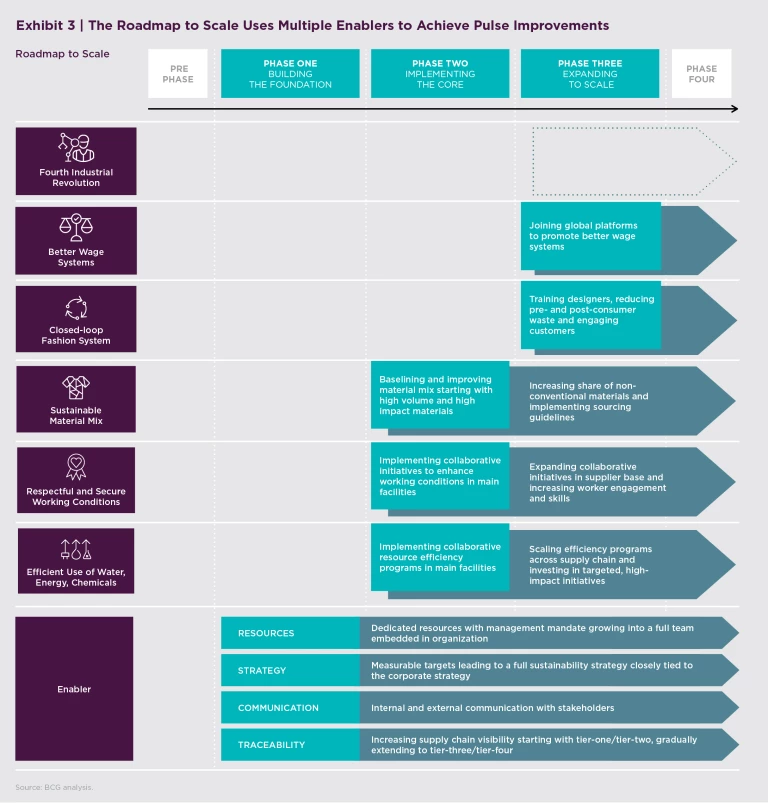

Building further on the comprehensive knowledge that we gathered from industry frontrunners, we collected existing high-impact solutions and best practices to develop our Roadmap to Scale. This guide for the industry offers inspiration and concrete actions that companies can begin implementing immediately. (See Exhibit 3.)

The roadmap presents a potential path for fashion brands and retailers—regardless of size, price positioning, or geography—to improve their environmental and social performance. It is a suggestive rather than definitive framework that reflects a range of experiences and insights. Each brand or retailer will have to develop its own interpretation of the roadmap depending on starting point, aspiration, and available resources.

Whatever their starting point, companies that use and adapt these best practices will improve their environmental and social performance, and raise their profitability. Successful implementation of the roadmap will give fashion companies a well-grounded foundation, including an ambitious strategy and dedicated team, as well as sustainability embedded deep within the core of the business.

The Roadmap to Scale consists of three phases: building the foundation, implementing core actions, and expanding to scale.

Building the Foundation

Phase one of the roadmap starts at the point after a company has decided to move beyond uncoordinated action and begins to lay out the key enablers of success, the most central of which is committing to sustainability. Other enablers include setting a clear strategy and goals, assembling a dedicated team and resources (though not many are needed at first), maintaining frequent communication both internally and externally, and ensuring traceability along the supply chain.

Devising strategies with short-term and long-term targets is the cornerstone of any major business endeavor, including reducing a company’s environmental and social footprint. While the adoption of targets is a valuable step, fashion companies also need to link these efforts to their overall business strategy, embedding sustainability into their core business.

Internal communication unites the organization around the ongoing effort to improve environmental and social viability. Companies need to share the top management’s commitment, explain the strategy and targets, and set transparent expectations for the supply chain. Only when cascaded through the entire organization can sustainability become an integral part of the company’s core business, values, and, ultimately, DNA.

Traceability in the supply chain is a prerequisite if companies are to understand the social and environmental impact of business practices and products. It enables brands to identify risks and challenges—and opportunities to increase operational efficiency—while building strong and trusting relationships with suppliers.

As a first step, a fashion company gradually invests in these enablers, which lay the groundwork for implementing initiatives along the roadmap and determining the brand's ability to scale its efforts later on. The quality of the enablers will determine the duration of the individual phases, the ease of implementation of any activity, and the ultimate environmental, social, and financial impact of the fashion company’s activities.

As the company pushes its efforts to scale, it adds members to the team, the strategy becomes more elaborate with bolder ambitious, and visibility into the supply chain extends toward tier-three and tier-four suppliers.

Implementing the Core

Phase two is where companies begin to see actual returns on investment in their commitment to environmental and social progress. With heightened visibility into their supply chain, organizations can see where they can take specific actions to improve their environmental and social performance, and increase efficiency. Implementing collaborative existing programs and initiatives enables companies to make significant progress in a relatively short amount of time. They can start improving their materials mix; use water, energy, and chemicals more efficiently; and strengthen their partnerships with suppliers to make improvements backed by a positive business case.

In the same vein, this heightened visibility helps companies cultivate more respectful and secure working conditions. Brands benefit most in this phase by joining collaborative initiatives that are already active and provide frameworks, standards, assessment methods, and training materials that participants may use and apply within their own sustainability work. In addition to improving safety and labor conditions, these initiatives address social topics such as financial inclusion, health, diversity, and gender equality.

Both types of activities simultaneously boost companies’ Pulse Scores and build capabilities and proof-points to unlock greater organizational support. This is where the investments start to pay off financially.

Expanding to Scale

Phase three involves building on the successes established in phase two. Only 10% of the industry— mostly the largest companies and sustainability champions—has reached this point so far. These frontrunners have secured organizational backing and managerial support to arrive at this phase. In a sense, scaling up sustainability efforts is no different from expanding any other business model or operational transformation: take the actions that yield initial successes, and roll them out across more of the supply chain. But scaling up also means intensifying efforts; and this, given the need for new ways of doing business in the fashion industry, requires looking further at available solutions.

Such solutions include using nonconventional fibers, adopting advanced methods of water and energy conservation, and collaborating to promote better wage systems. They may also include building closed-loop systems by training designers to consider the impact of their choices on the rest of the value chain, influencing consumer behavior, and increasing the reuse of pre-consumer waste. The environmental and social impact of change made at this level is significant for both environmental and social performance and for boosting profitability.

Driving initiatives to scale often requires enlarging the company’s investments, cultivating or acquiring specific expert knowledge, and increasing the operation’s size. In our experience, the companies that have the greatest ability to foster sustainability tend to be large organizations. In order to drive impact beyond previously achieved levels, companies undertake many of the activities during this phase in collaboration with peers or other players within the industry.

The Business Case is All Positive

Even when considered apart from the beneficial impact that investing in sustainability can have on brand building and risk management, the business case is compelling: improving a fashion brand’s environmental and social performance boosts profitability. Our discussions with industry frontrunners indicate that investments in resource efficiency, secure work environments, and sustainable materials go beyond counteracting projected losses to increase profitability.

Companies that implement and scale the activities showcased in the Roadmap to Scale can expect a positive EBIT margin uplift of 1 to 2 percentage points by 2030, in comparison with the 2015 baseline outlined in last year’s report. The case for sustainability is even stronger in a profitability comparison between implementing the roadmap and continuing business as usual. We calculate that continuing business as usual will result in an EBIT margin decline of 3 to 4 percentage points by 2030, in view of the expected rise in the cost of labor and other resources.

Comparing the decline in EBIT margin of 3 to 4 percentage points (business as usual) with the positive EBIT uplift of 1 to 2 percentage points from roadmap implementation reveals the true value of sustainability. (See Exhibit 4.)

MOVING INTO DISRUPTIVE SOLUTIONS

Even under optimistic assumptions, the industry’s existing solutions and business models will not deliver the impact needed to transform the industry. Fashion needs a deeper change. To break through to the fourth phase on the Roadmap to Scale, fashion companies need access to new technologies and models that are only just beginning to emerge.

Emerging Innovations

Developing these new technologies and models will not be easy in such an asset-intensive industry. Many of the innovations require collaboration to become commercially viable. This is especially so in areas of the value chain that have the lowest Pulse Scores, such as raw materials and end of use. Companies cannot develop these initiatives on their own.

On the basis of discussions with industry players and other actors, we have prioritized three of the most promising areas where we see new innovations: sustainable materials mix, closed-loop practices, and Industry 4.0. In other areas where the need for transformation is intense—such as in wage systems—innovation and development are still too far away, and thus cry out for ambitious collaborative efforts.

Sustainable materials mix refers to innovations in new and existing materials to reduce environmental impact. Examples of advances here include the development of nonconventional fibers made from substances such as citrus juice, grape plants, or kelp; bioengineered leather; and the further promotion of bast fibers. This category of innovations also extends to processes, such as chemical-free binding technology.

Collaborative research into and promotion of sustainable materials should be a high priority for the industry because current efforts to lower the negative impact of cotton and recycled polyester are far from adequate to resolve the problem. Companies have had trouble scaling solutions for sustainable materials, particularly in view of the volume of global demand and the complexity of sourcing.

Closing the loop involves minimizing the consumption of resources by facilitating their reentry into the value chain. In other words, it refers to repeatedly recycling and reusing materials until they become biodegradable waste. The current linear business model stresses the environment by generating waste throughout the value chain, whereas a closed-loop system seeks to minimize waste and to put unavoidable leftover material to use. Closing the loop can address the finite land, water, and energy resources that the fashion industry uses intensively.

Emerging innovations that support closed-loop systems include recycling technologies to produce new fibers comparable in quality to virgin fibers, optical fiber-sorting technologies to facilitate scalable recycling mapping and tracking systems to support pre-consumer waste upcycling and recycling, and consumer-focused fashion-as-a-service subscription programs.

Industry 4.0 has the potential to disrupt the way the fashion industry runs today, by leveraging the constantly increasing capabilities of automation and other technologies. While this level of change hasn’t yet begun in the fashion industry, it is inevitable and will likely affect every step in the value chain, making it leaner and driving much higher productivity.

Examples of such technologies that are now appearing include virtual design software that connects 3D design with the 2D pattern environment, and on-demand and 3D printing that have the potential to reduce waste and shorten time-to-market dramatically. In addition, sensors and Internet of Things technologies offer tracking and tracing opportunities that could serve multiple uses.

Only a Strong Innovation Ecosystem Will Turn Opportunity Into Reality

In order to accelerate these innovations and generate new ones, fashion’s stakeholders must work cooperatively to incubate and scale new ideas. Innovators in this industry need both funding and a strong network of support: extensive mentorship, patient capital, and close collaboration throughout the fashion value chain.

This calls for the development of an ecosystem, anchored by major brands, that addresses typical innovation boundaries:

- Deep, Often Specialized Topics Expertise. Supply chain innovations require advanced chemical or engineering skills, capabilities that most fashion brands do not have in-house, and that are rare among innovators.

- Time-Consuming Innovation Cycle. Fixed-assets innovation requires long R&D and capital expenditure cycles, unlike easily scaled virtual innovation.

- Capital- and Pilot-Intensive Proof-of-Concept Hurdle. Asset-intensive innovations have to be tested in facilities resembling the actual production, meaning that innovators depend on either the cooperation of suppliers to proof their concept or the support of investors. Neither is easy to come by, and investors are unlikely to invest in testing facilities prior to a successful proof-of-concept.

An Outlook Into a Disruptive Future

Fashion in the future may look dramatically different from the way it looks today. Innovation may fully disrupt how clothes are made and consumed. Global trends and forces are likely to shape consumer behaviors—and the role of brands and retailers—in unpredictable ways.

To help the fashion industry grasp potential developments, GFA and BCG have investigated disruptive patterns in other industries and interviewed thought leaders in scenario planning and digital disruption. On the basis of these findings, we present three scenarios of disruptive business models.

These scenarios are not predictions but a visionary look into the future—with a call for conversations on how companies might prepare and safeguard the future. The fashion industry must be vigilant about recognizing as early as possible the trends that will challenge their business models, and must plan effective responses that will lead to continued growth.

- Instant Fashion. Consumers order and receive the apparel they want, when they want it and how they want it, using technologies such as 3D printing and other on-demand production that happen at the point of sale. Such a production system has a smaller environmental footprint and a heightened ability to meet consumer demand.

- Fashion as a Service. The sharing economy comes to fashion to better promote reuse. In the same way that customers subscribe to software as a service (SaaS) rather than buying it outright, consumers in effect rent clothing. The lowered need for manufacturing in quantity significantly reduces the industry’s environmental footprint.

- Smart Fashion. Apparel becomes electronically enabled to instantly adjust to the wearer’s preferences. Smart fibers allow garments to alter colors, for example, improving environmental impact by reducing the need for multiple versions of the same item.

The fashion industry continues to face an enormous challenge in reducing its environmental and social footprint. BCG and GFA hope brands and retailers will follow the call for future collaboration and innovation. Only a joint effort will enable many of these disruptive innovations to reach the scale needed. Even in the best circumstances, the endeavor will require joint investments and efforts spanning several years. The urgency and the potential for value creation are as great as ever. We are confident that the creativity and commitment of fashion industry leaders can create a prosperous fashion industry.