The typical pharmaceutical business is far more complex today than in the industry’s blockbuster era, when fewer products, more stable demand, and high margins were the norm. For pharma companies to meet the growing complexity of the industry and the varying demands of their business segments, they need supply chain models that support the strategic priorities—agility, service, or cost effectiveness—of those different segments. A recent benchmarking study by The Boston Consulting Group identified four supply-chain models that can lead to optimal performance. This segmented approach to supply chain design is becoming the most effective way for pharma companies to address the challenges and tradeoffs they face today.

The complexity of pharmaceutical supply chains is growing exponentially. Prescription drugs are often just one aspect of the business as companies seek to offset shrinking margins by expanding into new areas: generics, over-the-counter (OTC) products, health services, companion devices, and many other segments. At the same time, companies are using direct-to-consumer, direct-to-pharmacy, and other new distribution channels, and they are relying more on external partners for manufacturing, selling, and other services. The business is rapidly becoming more global, too. Emerging markets are expected to drive 50 percent of the industry’s growth by 2014, and some of those markets require local access sites. The result is a proliferation of plants, products, suppliers, trade channels, customers, demand profiles, and service requirements—and minimal standardization of processes, procedures, and interfaces.

Despite these profound changes, few pharma companies have redesigned their supply chains. (See “Is Your Supply Chain Evolving with the Times?”) Instead, they’re using outdated models—ones that don’t meet today’s need for strategic segmentation. Because of this disconnect, the supply chain is still operating in a tactical manner instead of as a powerful competitive weapon.

Is Your Supply Chain Evolving with the Times?

Many supply chains in the pharmaceutical industry haven’t kept up with today’s business requirements. To evaluate where your company stands, answer the following questions:

- Are your markets, products, profit margins, customer requirements, and distribution channels the same today as they were a decade ago?

- If not, does your company understand the implications of these changes—and their effect on your supply chain?

- Have you redesigned your supply chain to improve performance and better coordinate your operations with current realities?

- Have you identified the strategic priorities of each product and customer segment and incorporated those priorities into the planning process to ensure that your company delivers on them?

- How are you balancing the agility, cost, and service tradeoffs?

- Do you know which segments are hurting supply chain performance, and do you understand the true underlying drivers of these problems?

If you’re finding that the growing complexity of your business is hindering supply chain performance, a fundamental redesign and transformation may be necessary.

Evolving Challenges, Competing Agendas

The pressures generated by these fundamental changes tend to affect all functional areas within the pharma organization—and competing agendas can lead to conflicts of interest. Country managers demand higher service levels. Finance looks for cost and capital optimization. Supply chain leaders seek to streamline the network structure and use external suppliers when possible. The head of operations marches down the continuous-improvement path. A more strategic approach to supply chain design can increase alignment across functions and be a competitive differentiator for the business.

The pharma industry has a unique set of challenges that has constrained past efforts to improve supply chains. For instance, quality standards can never be sacrificed in the pursuit of cost savings, and regulatory restrictions can inhibit some initiatives that could improve economies of scale. Moreover, to avoid the risk of running out of life-saving drugs, most pharma companies would rather err on the side of oversupply. But in today’s competitive business environment, companies must rethink the status quo and look for innovative ways to stay one step ahead—even if it means making tough decisions and profound changes. Pharma companies must capitalize on emerging markets, new distribution channels, and new areas of growth that demand cost efficiency and agility, such as generics, vaccines, and OTC products. At the same time, success requires an ability to guarantee the supply of targeted specialty-care and vaccine products to providers and patients.

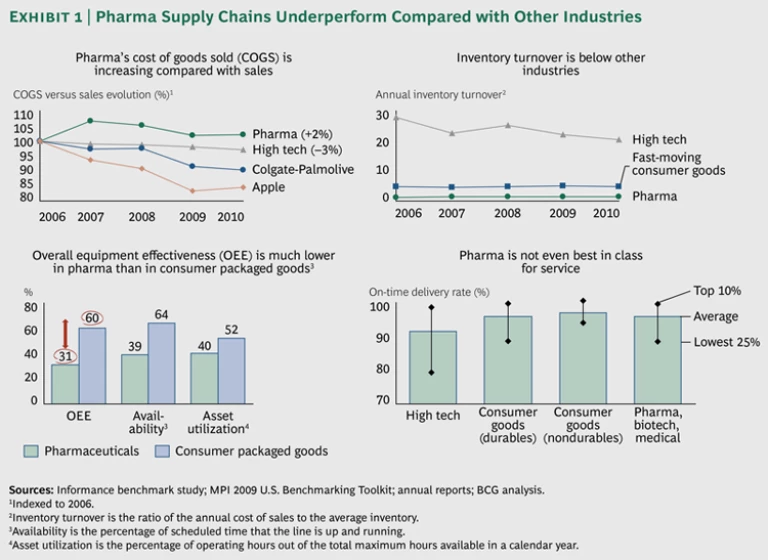

To succeed, the pharma supply chain must be lean, low cost, and flexible—without sacrificing product quality and service. Unfortunately, the typical pharma supply chain—with its fundamental steps of purchasing, producing active pharmaceutical ingredients, manufacturing, and distribution—is subpar relative to that of other industries. It shows weaknesses in critical areas of performance, including cost of goods sold, overall equipment effectiveness, inventory turnover, and even service. (See Exhibit 1.) This is not surprising, because pharma supply chains were designed to focus on maximizing service levels in a stable business environment, not to respond quickly to demand variability, which is a growing issue. In the past, demand was relatively predictable after the launch of a product and relatively stable in the developed markets that generated the bulk of sales. Supply disruptions were prevented by investing heavily in inventory and production capacity—a costly approach but one that was justified by high product margins. With these preexisting constraints and inefficiencies, pharma supply chains are forced to be reactive at all times, and they can barely meet today’s business requirements without extraordinary effort. Companies that continue on this path will lose their ability to compete and are putting their future viability at risk.

Lessons from Other Industries

Pharma companies have much to learn from other industries, especially those that have developed a deep understanding of the needs of their business segments and aligned their supply chains to achieve competitive advantage.

Zara upended the fashion industry with its design, manufacturing, and distribution processes, which dramatically shortened the time needed for new items to reach the company’s stores. To stay ahead of fast-changing fashion trends, Zara developed a very agile supply chain with short lead times to bring new styles to market more quickly. For its basic lines of clothing, which tend to change less frequently, the company developed a more cost-effective supply chain with longer lead times. Following Zara’s example, pharma companies should identify different business segments’ needs and design fit-for-purpose supply chains.

Apple has built a supply chain that ensures high service levels and agility by developing a closely integrated network of supplier partners, primarily in China. The company works closely with these key suppliers, securing their production capacity to ensure product availability and speed to market. Apple also minimizes the complexity of product components and finished goods so it can manage demand volatility across markets and product styles. Taking a page from Apple’s playbook, pharma companies should aim to integrate more closely with their suppliers and strategically manage complexity in order to gain flexibility and access to new skills.

Ikea has built a low-cost supply chain to stock its stores with merchandise at prices that are 30 to 50 percent below the competition. How? By focusing on cost effectiveness at each step of the supply chain, making tradeoffs on product complexity, and closely collaborating with key suppliers. Like Ikea, pharma companies can go beyond narrow, functional cost improvements by rethinking and improving the end-to-end supply chain.

Procter & Gamble has adopted an agile, cost-effective model that allows the company to respond quickly to changes in demand. P&G gets real-time demand data from retail stores and is at the forefront of vendor-managed inventory and collaborative planning, forecasting, and replenishment. In addition, P&G has set up different lead times for different customer types, depending on their needs. This customized approach and high level of service make the company a favored supplier—and help keep competing products at bay. Similarly, pharma companies could improve their planning and customer segmentation in order to increase service levels and respond more quickly to changes in demand.

Balancing the New Priorities: Service, Cost Effectiveness, and Agility

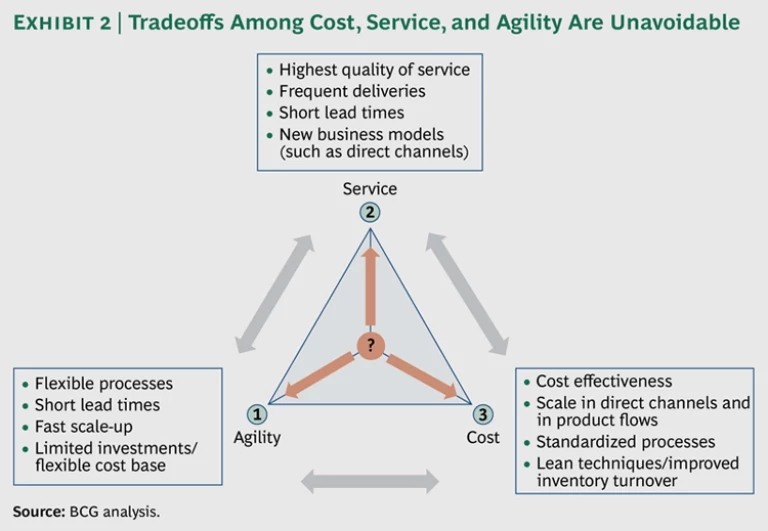

To meet the current industry challenges and increase overall competitiveness, pharma supply chains must improve how they manufacture and deliver finished goods, create new channel strategies, and drive revenue and margin performance. This ambitious agenda requires excelling in three critical dimensions:

- Service. Supply chains must continue to ensure that the right products are at the right place at the right time. For some segments, this is the most important supply-chain priority, and cost effectiveness and agility are secondary considerations. When this is the case, pharma companies should design their supply chains to focus on product availability. An analysis of demand patterns will reveal which products have stable, predictable demand—and which have more volatile demand, possibly requiring investments in capacity and inventory. Once product availability is in place, companies can focus on offering greater speed, convenience, and other services to their customers.

- Cost Effectiveness. Most pharma companies have already taken their supply chains down a long path of cost improvement, but success in some segments requires even lower upstream and downstream costs. For further savings, aim for standardized processes, lean techniques, faster inventory turnover, higher capacity utilization, and larger scale benefits.

- Agility. Some segments require a highly responsive supply chain, one that can react quickly to changes in the business landscape. This agility can help pharma companies speed up product launches, extend the life cycle of existing products, enter new markets more quickly, and be more responsive to changes in demand and new business opportunities. Key features that lead to agility include effective planning and scheduling, rapid changeover of production lines, strategic use of inventory, production postponement, sourcing from multiple suppliers, and external production capacity for greater flexibility.

Maximizing all three dimensions at the same time is impossible, of course, and tradeoffs are unavoidable. High service levels often come at a higher cost, for instance. (See Exhibit 2.) With a deeper understanding of business requirements, business and supply chain leaders can develop the insights needed to decide which tradeoffs should be made for which products; to align the often-diverging priorities of R&D, operations, and marketing; and to deliver on these important priorities.

Priority-Driven Segmentation: Four Models

To manage these competing demands and the inevitable tradeoffs, pharma companies must determine their business priorities for each product and customer segment. They also need to create tailored supply-chain strategies on the basis of factors such as sales volume, demand volatility, product characteristics, life cycle maturity, customer needs, and competitive differentiation.

Different markets, therapeutic areas, and product types—including prescription drugs, generics, biologics, and OTCs—will have different strategic priorities that should determine the supply chain design. For instance, the priorities for a patent-protected oncology drug may be to minimize quality risks, enable market access, and ensure product availability using direct-to-hospital distribution. For a generic cardiovascular product, however, availability would still be important, but the top priorities would likely be to optimize cost efficiency in order to compete against other generics in this class and to develop the ability to manage a tender business steeped in uncertainty and volatility.

A single product type might have different priorities based on market dynamics, customer needs, and life cycle stage. During a product launch, for instance, the key priorities are apt to be service and agility, thereby ensuring product availability to physicians—who must start changing prescription patterns—and the ability to respond effectively to potential upside demand. Cost effectiveness may only become a priority at later stages of the product life cycle, during its maturity and decline. The same product can have a very stable demand pattern in a mature market such as the U.S. and a volatile one in an emerging market like Brazil, requiring different supply-chain approaches.

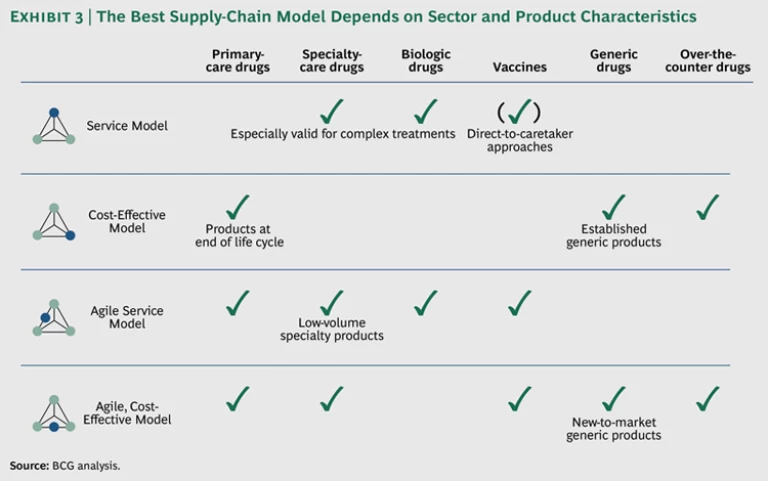

Using the three key business priorities of service, cost effectiveness, and agility, BCG identified four segmentation models that pharma companies can apply to their operations. The applicability of each supply-chain model depends on the business segment, customer needs, and key product behaviors and characteristics. (See Exhibit 3.)

The Service Model. This supply-chain model is well suited to segments in which the cost of an unavailable product is high, either due to reputational impact (in the case of medically necessary products), the availability of competing products, or basic economics if the product margins are high. Because aiming for 100 percent product availability is costly, the service model works best for high-margin products and those with predictable demand. The model requires investing in capacity and inventory to achieve high service levels. To get the highest return on these investments, pharma companies should optimize their production systems and inventory levels, capitalizing on demand predictability. Forward-looking companies are also rethinking traditional pharma products and their distribution and are looking for innovative service components that would be a source of competitive advantage and added revenues. For example, providing a country’s ministry of health with an uninterrupted, temperature-controlled supply chain for vaccine distribution is a valuable service and makes demand more “sticky,” but it increases the complexity of the supply chain.

The Cost-Effective Model. For segments with shrinking margins, inefficiency and waste must become relics of the past. Lean operations are critical when selling to emerging markets with significant pricing pressures, when competing against low-cost providers, and when selling lower-margin products such as generics and OTC drugs. The low-cost supply chain aims for manufacturing scale, high capacity utilization, streamlined processes, minimal complexity and waste, minimal transportation costs, and process reliability to keep costs low while maintaining high-quality standards. In many cases, these improvements require a step change in capability beyond what typical continuous-improvement programs will deliver. This model’s goals of maximizing capacity utilization and minimizing costs limit agility and make it necessary to allocate production across different markets and products. For example, manufacturers of generic products will pursue global scale, reduce product complexity, set up facilities in low-cost locations, and keep prices low, aiming for high volume rather than high margins. Generic companies must constantly rebalance their portfolios, adding new products and dropping those that no longer fit.

The Agile Service Model. Availability and fast response times are critical when new products are launching, customer demand is volatile, and sales volumes fluctuate due to factors such as competitors moving in and out of a market and the introduction of competing drugs in a therapeutic area. The goal of the agility model is to create a flexible, highly responsive manufacturing and distribution network by rethinking current processes, production strategies, and network design; outsourcing noncore activities; and using partnerships, contract manufacturing, and logistics providers to increase flexibility. Strong end-to-end supply-and-demand planning and information flows are also critical in order to optimize inventory levels. Segments that will benefit the most from this model are those in which product enhancements have resulted in a proliferation of stock-keeping units, new priority markets have highly uncertain forecasts, and constraints of a technical nature such as cold chain or shelf life require supply chains that are more flexible and responsive. A good example of a segment well suited to this model is a patented product with strong growth prospects in a large emerging market such as Brazil.

The Agile, Cost-Effective Model. While high service and low cost tend to be mutually exclusive, agility and cost effectiveness can coexist to a certain degree in the same supply chain if companies thoroughly understand their business needs, plan rigorously, improve end-to-end processes, keep operations lean, and outsource noncore activities. They must also be ready to use partnerships, contract manufacturing, and logistics providers as needed to increase flexibility. This model requires ongoing communication between the business and supply chain operations through an effective sales and operations planning (S&OP) process. For instance, in competitive tender situations, demand can be hard to predict and downward pressure on prices means operations must be lean. To succeed, supply chain operations and the business must maintain an active dialogue to plan production and align priorities so that they can allocate product if supply is constrained. Moreover, the business must agree to accept potential product shortages in certain markets—a necessary tradeoff to allow for the coexistence of cost and agility. For example, after its key primary-care product lost patent exclusivity, one pharma company had to redesign its supply chain, moving from a service model to a focus on cost effectiveness and agility in order to compete against generic manufacturers. The company consolidated its supply network, increased capacity utilization, minimized inventory levels, and redesigned production processes.

Getting Started

Tailored supply-chain models offer a range of benefits. They can increase manufacturing flexibility for products with more volatile demand; help ensure that resources and capabilities are allocated in ways that better meet the needs of specific customer segments; and support growing complexity at a competitive cost. In short, more effective supply-chain designs can be both economical and a strong source of competitive advantage, yet few pharma companies segment their supply chains beyond product type or business. Those that do may segment some production steps based on volume and volatility profiles. For instance, they may move to a make-to-order strategy for low-volume, low-volatility products to eliminate inventory, or they may drive down levels of inventory for high-volume, low-volatility products. But companies can go much further than this to fully capitalize on the potential benefits of supply chain segmentation by making segment-specific decisions along each step in their supply chains. This requires a strong analytical and programmatic approach.

As a first step toward developing more tailored, effective supply chains, pharma companies must truly understand the demand and performance patterns of their different segments. To this end, companies must analyze each segment’s volume, market-demand volatility, and margins. It is equally critical to analyze the end-to-end supply-chain performance for each segment in areas such as cost to serve, service levels, and inventory levels. This analysis can reveal preexisting problems with supply chain design that the new strategic realignment can address. This clarity leads to better communication and decision making among supply chain and business leaders—and to a more strategic supply chain explicitly designed around segments’ needs. The new design must consider how to reshape the manufacturing and sourcing network; when and where to collaborate with external partners; and what new systems, processes, and metrics to put in place. (See “Improving Supply Chain Performance.”)

Improving Supply Chain Performance

On the basis of our work and experience, BCG has identified a set of key levers along the supply chain that leaders can use to improve supply chain performance:

- Product Complexity Management. The proliferation of stock-keeping units driven by individual market specifications limits flexibility in the supply chain, such as the ability to absorb demand volatility by reallocating products across markets. Component complexity upstream in the supply chain—such as with bulk products and active pharmaceutical ingredients—can have major repercussions on flexibility downstream.

- End-to-End Supply-Chain Planning. Intensity and frequency of network-level demand planning and S&OP processes can be adjusted by product, market, and customer segment. Special attention should be paid to hard-to-forecast segments—such as competitive tenders—in which companies need a clear understanding of the return on investment of active planning versus alternative models such as so-called at-risk production (production that occurs when there is no clear sign that the product is needed).

- Inventory Strategy. Strategic positioning of inventory buffers along multiple stages of the supply chain—as well as improving inventory levels based on the variability of demand and supply—allow supply model segmentation while ensuring appropriate use of working capital.

- Production System Strategy. Selecting the right production model—such as the make-to-order or make-to-stock model—and the right equipment for different demand segments can help companies get more from the existing asset base. Applying this lever across multiple assets and putting in place a platform for continuous improvement can reveal other opportunities to reduce the asset base and achieve significant savings.

- Enterprise Supplier Management. Segmented production strategies shouldn’t be limited to company-owned manufacturing and packaging assets only. Companies that optimize the production strategies and inventory policies of their external suppliers and contract manufacturers can lower costs and add flexibility throughout the supply network.

- Transportation Management. Companies can offer different service levels and response times according to customer segments’ needs, strategic importance, and willingness to pay. Options such as shipment routing and services such as expediting and tracking can differentiate a company from its competitors.

- Visibility Platforms. Companies often do not have the data and analytics to understand their end-to-end supply-chain performance in the areas of cost, service, and responsiveness across all product groups. Visibility and performance management tools can provide greater clarity and pinpoint the drivers of underperformance.

Once the right design is selected, the next steps are to align execution at each plant and distribution point, build the required tools and skills, and ensure data transparency across the network. Finally, it will be necessary to install simple coordination mechanisms along the supply chain and ensure agreement among all end-to-end players.

All functions along the supply chain will be involved in the transformation, increasing the importance of a programmatic approach to change management and senior-leader alignment. Particularly critical to enabling and embedding the transformation will be leadership’s commitment to capability development, organizational alignment, analytics, data access, and full end-to-end cost analysis.

Major change is always challenging, but this evolution has been a long time coming for the pharma industry. The forward-looking companies that embrace these new models will finally have supply chains that help rather than hinder their strategic priorities—and will gain a powerful competitive advantage.