A global survey of treasurers at multinational corporations around the world reveals that while banks remain valued partners, a more open and digitized playing field has changed what it takes to compete effectively in transaction banking. Treasurers expect banks to do four things: serve as a leading aggregator for the entire treasury ecosystem, use IT capabilities to provide efficient and personalized service, offer superior risk management and advisory capabilities, and tailor big-data analytics and digital capabilities to improve the overall treasury experience.

About This Report

This report was developed based on a proprietary cross-industry survey of 750 corporate treasurers and CFOs from organizations around the world with consolidated annual revenue of more than $500 million. The survey was conducted by Expand Research (a wholly owned subsidiary of The Boston Consulting Group) for BNP Paribas and BCG. In addition, interviews were conducted with 25 corporate treasurers and CFOs at multinational organizations included in the survey.

This second edition builds on the findings of the 2015 Corporate Treasury Insights study and adds two topics that increasingly concern treasurers: cybersecurity and advanced analytics.

A Premium on Price and Service

Several trends observed in the 2015 Corporate Treasury Insights survey picked up momentum in 2016. Treasurers indicated that their responsibilities continue to expand. Moreover, in the face of continued market uncertainty and operational complexity, the 2016 survey found that treasurers are less interested in product enhancements than they are in having their transaction banking partners deliver predictable, reliable solutions backed by excellent execution. As one interviewee noted, “We are old-fashioned and traditional in the products we use. We focus on keeping things simple.” Product depth, market leadership, and value-added services fell low on the list of transaction-banking-partner selection criteria, at 14%, 12%, and 2%, respectively. Instead, the majority of participants said that pricing (70%) and service quality (60%) are their primary considerations.

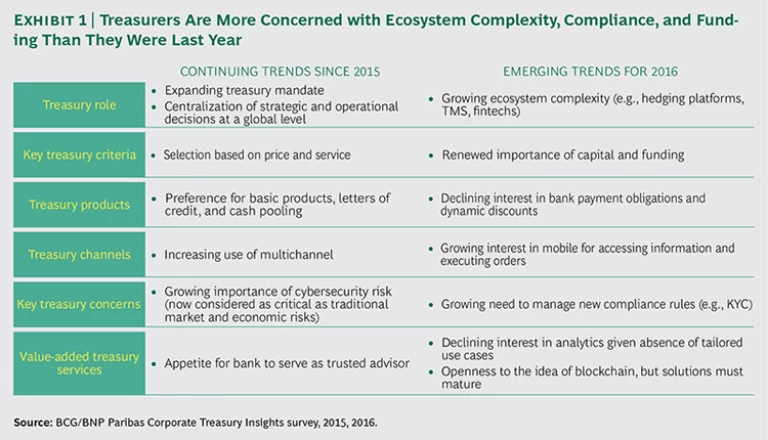

Comparison with last year’s survey also revealed a number of emerging issues for 2016. These include a growing interest in mobile for accessing information and executing orders, a renewed interest in capital and funding management, and an increasingly urgent need for effective solutions to address compliance rules. In addition, lower barriers to entry, greater product choice, and sophisticated financial services integration platforms have commoditized some core bank offerings and led to greater disintermediation. While fintechs and other digital players are not likely to displace transaction banking business models outright, many entrants (such as Adyen and FXall) are successfully nibbling away at the edges with specialized services and customer-friendly interfaces. In addition, the increasing adoption of treasury management systems (TMS) and enterprise resource planning (ERP) platforms that can integrate and automate cash management, payment, reporting, and other functions gives treasurers a powerful alternative to bank portals, providing them with a more complete picture of their treasury operations. (See Exhibit 1.)

Low Growth In Core Transaction Banking Products

While working capital financing (WCF) solutions and trade finance products will continue to court a loyal user base, the survey findings suggest relatively low additional growth in these areas.

Working Capital Financing. Survey responses indicate that treasurers continue to find WCF products attractive. That is especially true with respect to supplier and receivables financing offerings, which nearly 70% of treasurers said they have used in the past two years. The overall base of users, however, is not expected to grow, since nearly 95% of non-WCF users in this year’s survey said they had no plans to begin using these offerings. (Other corporate functions beyond treasury may feel differently.)

Cash Management. Global physical and notional cash pooling remain attractive, but the current low-interest-rate environment has reduced the benefit. Forty percent of respondents to the survey said that these arrangements are now less of a priority.

Trade Finance Products. Export and import letters of credit continue to be the predominant choice for international trade despite the emergence of new digital payment instruments, and we expect that treasurers will continue to favor the use of letters in the near term. The survey also showed a slight decline in the use of bank bilateral/syndicated guarantees, trade loans, and document collection. The use of bank payment obligations (and dynamic discounts for WCF) by treasurers across regions and company size continues to fall—and that decline grew more precipitous in 2016.

Regional Variations. In the Asia-Pacific region, receivables financing was down slightly this year. In North America, interest in inventory financing, payment, and collection factories grew, and interest in electronic bank account management and signature management waned.

A Rapidly Evolving Digital Landscape

The digital technology landscape has introduced an array of platforms, expanded the functionality available on those platforms, and opened the market to nontraditional competitors.

A Call for Platform Flexibility. Treasurers want a consolidated view of their liquidity and financial positions, detailed reporting, and greater consistency across geographies. They want platforms to aggregate such areas as cash management, trade, working capital management, and foreign exchange (FX) hedging. But they don’t want to be tied to a single banking platform. Despite banks’ investment in building their own platforms, treasurers consider such solutions to be intrusive and binding. TMS and other external platforms, by contrast, offer treasurers an integrated, multibank offering, while ensuring neutrality. Looking ahead, we expect more treasurers to choose TMS or ERP over single-bank platforms. As one respondent noted, “There is a conflict of interest in having a bank provide a multibank platform. TMS have the advantage of being neutral.”

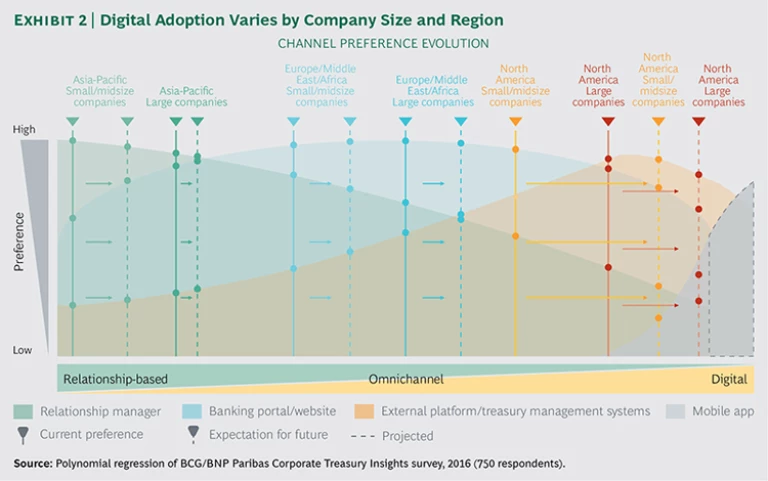

Not all treasurers, however, are ready to embrace external platforms. Channel adoption varies by company size and region, with some treasurers preferring a relationship-manager-driven model, while others want more-advanced digital capabilities. (See Exhibit 2.) Small companies in Asia-Pacific, for instance, tend to embrace traditional banking portals, with relationship managers playing a prominent role in day-to-day operations, while in North America, most large companies have already migrated to external platforms and TMS and are now looking to add greater mobile capabilities. In fact, while relatively few treasurers expressed interest in mobile as a channel in 2015, roughly 30% of respondents to this year’s survey, led by those from North America, indicated that they would like mobile access to facilitate reporting and information sharing and to provide transaction alerts and confirmations.

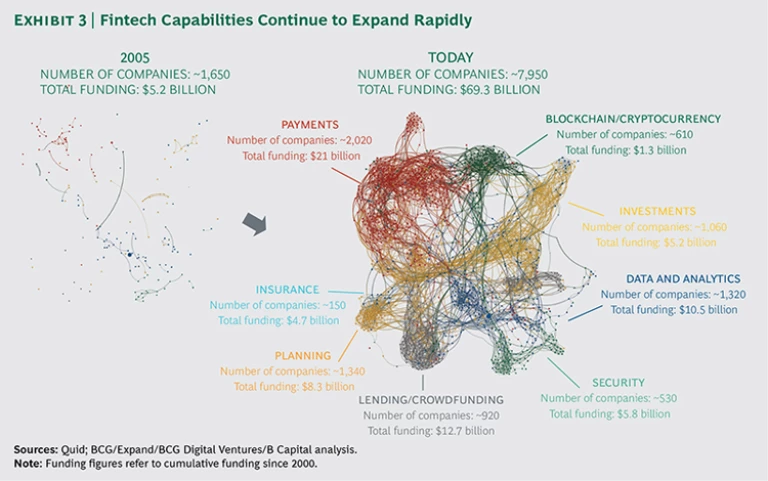

The Emergence of Fintechs. Fragmentation in the provider ecosystem will increase. Over the last couple of years, many new fintechs have entered the transaction banking market seeking to position themselves as alternatives to traditional banks by offering solutions that optimize specific elements of the transaction banking value chain. (See Exhibit 3.) While treasurers like the specialized value propositions and the often-cheaper price points that fintechs provide, 90% indicated that fintechs are not yet capable of meeting the full array of corporate treasury needs. They cite the small scale and relative youth of these businesses (many of which have yet to weather a full economic cycle) and perceive the fintech environment to be less secure. One trend that we expect to gather momentum is for fintechs and large transaction banks to partner with each other for their mutual advantage. As one participant noted, “If banks don’t react, they will get ‘Uberized’ by fintechs.”

Treasurers Expect Banks to Respond to Their Needs in Four Ways

Treasurers want their banking partners to evolve their service models in the following ways.

Orchestrate the full treasury ecosystem. While some treasurers in large corporations may have the IT capabilities in-house to get the data they need, others expect their banking partners to provide a convenient, integrated, and seamless customer journey across providers, systems, and products.

Banks are in a strong position to do just that. They have the resources, expertise, and long-standing relationship insights to understand what treasurers need in order to deliver a qualitatively superior customer experience—one that covers the spectrum of treasury needs, from cash management and payments to reporting, across all providers. But making good on that aspiration and creating a one-stop-shop platform will require banks to embrace open architectures, standardize data (to eliminate inconsistencies), and provide timely, customer-specific analyses.

Most treasurers in our survey, for instance, still complain of undue process complexity within banking systems. They want banks to go further in simplifying administrative tasks, especially those related to compliance procedures. Offering electronic bank accounts, signature management, and automatic form filling, for instance, would reduce a significant amount of treasury department time and paperwork, particularly on the regulatory side. More integrated information-sharing processes within banks would allow treasurers to access insights more quickly. And by sharing more data with third-party providers, banks could help treasurers save time on routine tasks; for example, know-your-customer forms could be reused on an external FX trading platform. But treasurers want banks to do more than just automate existing processes. They want them to redesign core treasury activities—those within the bank and across the value chain—to make the end user experience fast, simple, and convenient.

As one interviewee stated, banks need to offer “real plug-and-play solutions.” The use of open-architecture platforms would allow banks to create a powerful ecosystem in which third parties could participate—adding and augmenting services—with the bank serving as overall coordinator and aggregator. One interviewee we spoke with noted, “Just as Facebook allows users to access a number of other sites and functionality from just one platform, banks need to make the transaction banking experience that simple.”

Make IT capabilities central to the value proposition. Treasurers are highly sensitive to any form of technical disruption that might put business continuity at risk. They see IT excellence to be every bit as important as product excellence. For them, the reliability of bank systems is not only an operational issue but a strategic one. As the treasurer of one of the largest companies in the world put it, “The key to success in this environment is systems, systems, and systems.” A strong IT infrastructure is a must.

Treasurers expect their banking partners to leverage their IT capabilities to improve consistency and reliability in five ways:

- Lower error rates

- Better visibility overall and better traceability with respect to incidents

- More responsive local support teams that can detect and resolve issues rapidly and with greater consistency across geographies

- Standardized, global performance metrics

- More frequent and relevant communication

In a competitive market, a bank that can demonstrate zero-error delivery, for example, would have a distinct advantage. It could extend that lead further by establishing joint IT/commercial client service teams able to extract, package, and deliver insights in a rapid, customer-friendly way. In the words of one participant, “Banks are now IT companies selling financial solutions.” So long as these moves are seen as authentic (and not window dressing for a proposal), IT leadership can help banks advance their own market leadership.

Embody a trusted advisory role, especially on risk. Treasurers are looking for trusted partners who can help them tackle market uncertainty, regulatory changes, and cybersecurity and fraud. Market and counterparty risks remain high in the current negative-yield environment, with foreign-exchange volatility, the collapse of commodity markets, and growing economic uncertainty in emerging markets and Europe among the driving factors. “I never want to go through another 2008/2009 crisis,” said one interviewee. The survey found treasurers paying much closer attention to counterparty risks and cyberthreats. Those risks now rank on par with market and economic risks among those surveyed. Compliance is another concern, especially in light of recent heavy regulatory fines imposed on some corporations in North America.

Banks have an opportunity to serve as valued advisors in helping treasurers understand and mitigate their risks. As one interviewee stated, “We need expertise from banks in areas that TMS and nonbanking providers will never be able to provide.” Banks can extend that expertise in a few ways: by securing company funding; by leveraging their knowledge to provide in-depth support and advanced advisory services to improve FX hedging strategies and other treasury activities; by helping treasurers better assess counterparty credit risks; and by helping treasurers navigate the complexities of the local regulatory environment. Our survey revealed that roughly 30% of treasurers are willing to pay for such advisory services, and that number is even higher among respondents from large corporations in Europe, the Middle East, and Africa.

Among the top issues are cybersecurity and fraud. One interviewee recalled a situation in which a hacking attack knocked an entire division offline for several days. “We were operating with no visibility,” he said. “Had the situation lasted any longer, we would have been in deep trouble.” Fraudulent payments are another major risk concern. Most interviewees reported that fraud attempts were on the rise and that those attempts were becoming more sophisticated and harder to track.

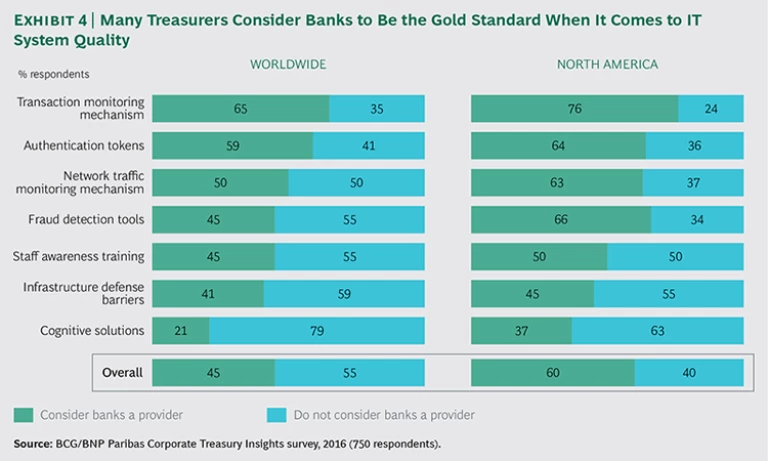

Among treasurers who flagged cyberattacks as a high risk factor, more than half reported that they have not deployed (or are unaware of) common mitigation measures, such as staff awareness training, authentication tokens, and fraud detection tools. In addition, approximately 75% of this group said they do not use cognitive systems, infrastructure defense barriers, and network traffic monitoring mechanisms.

In fact, to date, treasurers have mainly concentrated on strengthening their internal control procedures (using such things as systematic double signatures to authorize payments, regular screening, and updating authorized suppliers’ lists, as well as appropriate segregation of tasks between departments), while delegating other security measures to the IT department and folding them into broader company-wide efforts. That leaves treasurers to rely on the security layers embedded into their banking platforms, the strength of which they can largely only guess at.

Banks can fill that void by providing external certification of the strength of a business’s treasury IT infrastructure security. The survey revealed that many treasurers consider banks to be the gold standard when it comes to IT system quality, given the high security thresholds they require in their own operations. More than half of respondents consider banks a preferred provider for traditional mitigation measures, such as transaction and network traffic monitoring mechanisms and staff training. (See Exhibit 4.) In addition, 20% to 40% would consider using bank solutions for all their IT-based treasury needs. “Banks can talk in a language that treasurers understand,” said one interviewee. Treasurers signaled that they would look favorably on banks that take proactive measures to share their expertise and internal best practices to help treasurers strengthen their internal control procedures and secure their IT infrastructure. That is especially true for companies with limited internal IT capabilities. One treasurer noted, “I would pay for advisory services from my bank to diagnose such things as the security level of my systems and help me understand what I should improve.”

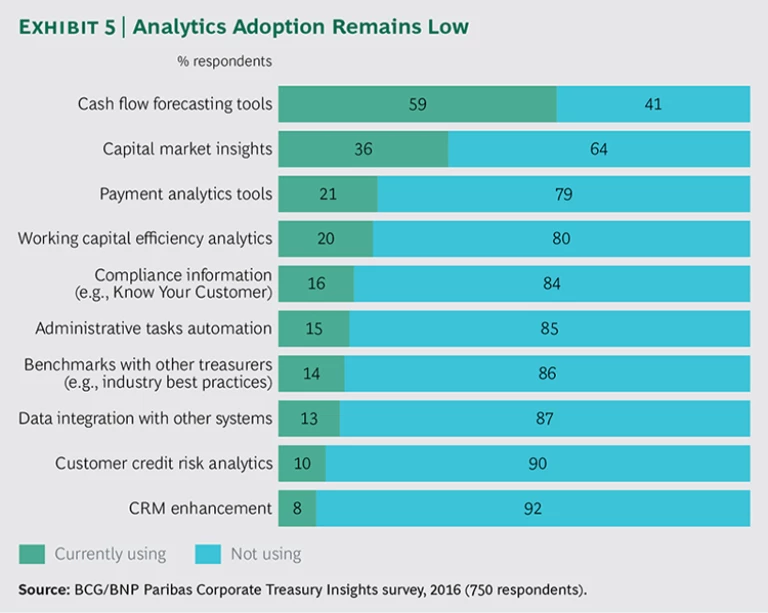

Help treasurers take advantage of analytics and other digital capabilities. With the exception of cash flow forecasting, relatively few treasurers indicated that they are using advanced analytics currently, and of those who are, roughly 60% rely on in-house solutions. (See Exhibit 5.) Treasurer interest in analytics solutions has softened over the last year. Our interviews suggested that the low uptake has to do with the lack of tailored, relevant, and concrete use cases. Nevertheless, treasurers remain conceptually interested, especially in cash flow forecasting tools, advanced capital market insights, peer group metrics, working capital efficiency analytics, and payment analytics tools—but they want banks to tailor these solutions to the treasury and their own corporate environment. Banks can respond to this interest by using their data capabilities to provide such things as detailed market intelligence, which treasurers working at large multinationals would find especially valuable.

Banks, of course, are not the only ones looking to capitalize on such opportunities. Specialized start-ups that have the advantage of independence, client-centric business models, and cutting-edge technologies will be competing for the same business. The small size and scale of these entrants mean they are unlikely to dominate the market, but as with other fintechs with market-leading capabilities, several could prove to be attractive partners.

As to other areas, while many banks are experimenting with blockchain technologies to manage and authenticate payments and transactions, few treasurers have yet to employ blockchain (although many said that they find the technology to be conceptually appealing). One interviewee noted that blockchain has the potential to be “a real disruptor in the transaction banking industry.” For blockchain to gain traction, however, banks will need to provide clear use cases and tested solutions that provide the right aggregation, control, and regulation. In addition, while blockchain could emerge as an alternative to traditional back-end banking operations, treasurers will still need a bank or other trusted party to coordinate the ecosystem and manage front-end activities.

Banks will have to work harder to meet the sophisticated needs and expanding remit of their treasury clients. At a time of increasing fragmentation, treasurers expect banks to offer a streamlined, transparent, digitized, and customer-friendly experience and serve as a one-stop shop to address the full set of treasury needs. Banks can meet those expectations by leveraging their traditional IT strengths and trusted advisor status and by partnering with fintechs to provide tailored solutions and data-driven insights. Banks that deliver best-in-class execution, enrich their advisory value proposition, and incorporate fintechs into their offering will hold a formidable competitive advantage. In the end, it will be all about security and client experience.

Acknowledgments

The authors would like to thank Mylène Delahaye, Alec Mclaurin, and Anna Segura from BNP Paribas for their valuable contribution to this report and their helpful thought partnership. They also extend their thanks to Franck Vialaron, Steve Mwenifumbo, Boris Lavrov, and Emily Chapman of Expand Research for their support and advice in designing and executing the proprietary global survey and their experience in conducting large-scale global quantitative analysis. Finally, they thank Ali Kchia, Ankit Mathur, Anubhav Mital, and Maarten Peeters from BCG for their valuable help.