By many measures, the private equity (PE) industry is in a golden age right now. Never have there been so many PE firms and so many new players. The amount of uninvested capital, or dry powder, is at an all-time high, and funds continue to outperform most other asset classes—keeping investors happy.

Yet maintaining these returns is anything but guaranteed, thanks to emerging challenges on multiple fronts. As the field grows more crowded and capital floods in, firms will struggle to differentiate themselves, competition for deals will increase, and (if past experience is any guide) many will face pressure to boost returns through higher deal multiples and leverage.

In addition, the once-standard “2 and 20” fee structure is under pressure as investors look to lower costs. Some investors are revamping their relationships with PE firms, seeking direct access to investment opportunities and consolidating their investments among a smaller number of high-performing funds.

Given these challenges, PE firms need to take concerted action today. Specifically, based on our experience, they should do the following:

- Turn their operational playbooks inward.

- Develop a true talent strategy.

- Upgrade their approach to value creation.

Looming Challenges

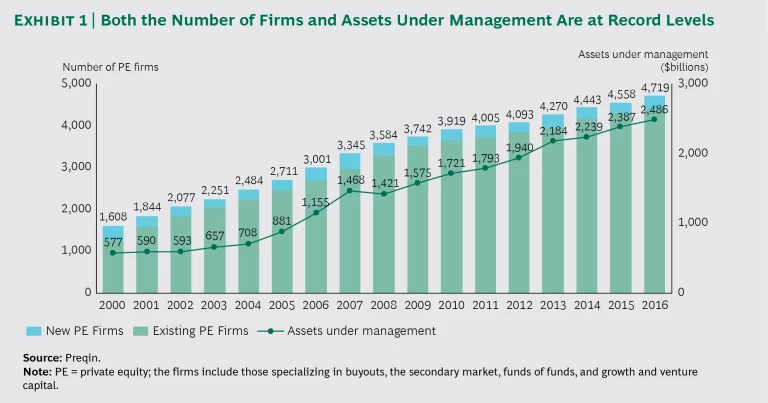

It is an understatement to say that PE firms are thriving. At the end of 2016, the industry had a record $2.49 trillion in assets, and 319 new firms launched in 2016 alone. (See Exhibit 1.) The industry now has nearly $900 billion in dry powder; and global savings from pension, mutual, and sovereign funds, as well as capital from other financial institutions and insurance firms, will likely continue to flow in. PE firms are outperforming public equities, fixed income, and real estate, and given the woeful performance of hedge funds in particular, investors are directing more capital into the PE sector as they hunt for higher yields. Fully 95% of PE investors are satisfied with the performance of the asset class, and more than 94% intend to commit at least the same amount of capital to PE next year, according to the 2016 Preqin Global Private Equity & Venture Capital Report.

As a result, top-performing firms are routinely closing their largest funds—which are bigger than ever—and oversubscription is common. Even new funds with scant performance history are benefiting. Valuation multiples have exceeded the peaks last seen in 2006 and 2007 for deals above $500 million, and deals above $250 million are nearing precrisis levels, thanks to competition for quality assets and readily available financing at historically low interest rates. (Leverage has not yet reached precrisis levels, but it is getting close.) In some cases, the amount of private equity cash that is chasing scarce assets has led to “express auctions” that decide hotly contested bidding battles in a matter of hours.

The rush of new entrants has also increased the competition for every deal. New entrants from China, for example, are putting money to work in developed markets. They are adapting to Western deal processes, innovating in how they are getting money out of China, and establishing creative offshore vehicles. But the most notable change in competition is likely to come from the firms’ “customers”—the limited partners (LPs). Increasingly, LPs now seek a more active role in the investing process. After years of staying behind the scenes and watching general partners (GPs) in action, LPs are beginning to make direct investments in high-performing assets themselves or seeking co-investment opportunities with GPs. In some cases, such LPs as sovereign wealth funds are demanding that PE firms educate their staff or even help them build their own internal direct-investment teams—essentially compelling firms to create more competition for themselves.

There is a clear payoff for making such moves. According to a recent Palico survey, roughly 90% of LP investors reported that returns from their co-investments have matched or outperformed their PE fund investments. More than two-fifths said that their co-investments have done better than their fund investments, and only 10% stated that their co-investments have done worse than their funds.

In addition to their demand for co-investment, which typically serves to lower net fees paid, LPs are increasingly challenging the traditional 2-and-20 fee structure. (In part, the fee pressure stems from the sheer amount of dry powder, which reduces fund returns.) Already, management fees have decreased by 20 basis points, on average, and some funds have reduced their carrying fees from 20% to 10%. In other cases, GPs are offering their LPs flexibility through other measures, such as co-investment opportunities, separate accounts, and joint ventures.

To be clear, the best firms are still able to hold the line on fees, and smaller LPs lack the clout to refuse. (They could take their capital elsewhere, but that is unlikely.) We expect to see a continued split between the top funds, which can maintain fee levels, and the laggards, which have to make concessions.

Another shift in the industry is that LPs are consolidating their relationships and working with a smaller number of firms. Such moves allow LPs to reduce their internal operating costs, simplify compliance and performance reporting, gain leverage in fee negotiations, and secure access to top-quartile funds and co-investment opportunities. Similarly, LPs increasingly demand customized products based on their specific investment mandates and yield targets. For example, separately managed accounts are gaining prominence as a way for LPs to capture higher net returns by deploying a chunk of capital across all strategies within a fund.

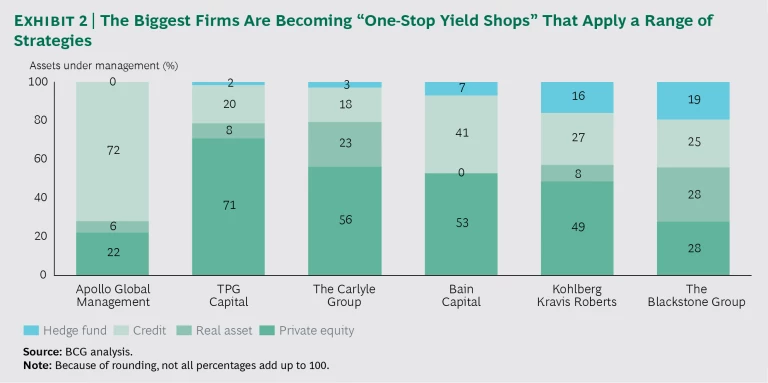

As LPs increasingly seek a range of strategies and yields, firms with the requisite scale and resources (primarily the megafunds) are becoming “one-stop yield shops.” (See Exhibit 2.) They have the resources to run multiple funds across different investment strategies and approaches, including venture assets, growth, buyouts, credit, hedge funds, and infrastructure. The Blackstone Group, for instance, now has 28% of its assets under management in buyouts, 28% in real assets, 25% in credit, and 19% in hedge funds. Diversified investment strategies like these can better accommodate LPs that would prefer to work with a single firm that can meet all their needs.

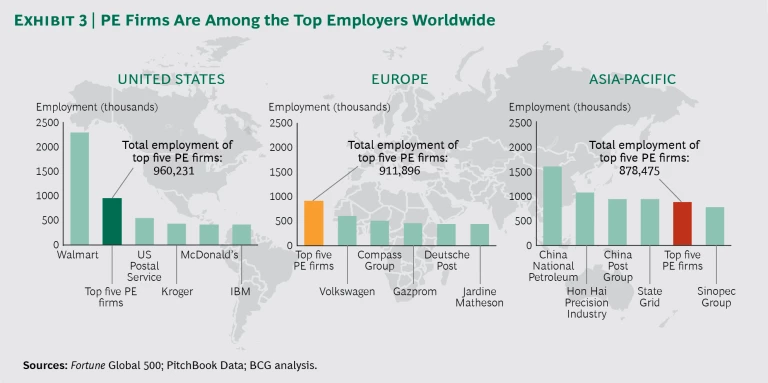

As the PE sector takes on a greater role in the global economy, firms will find themselves increasingly in the public eye, whether they like it or not. The top five PE firms in the US collectively employ nearly 1 million people in their portfolio companies, more than any other private-sector business except Walmart. PE firms in Europe and Asia-Pacific have similar clout. (See Exhibit 3.) As a result, the industry is coming under increased scrutiny from lawmakers and regulators alike. At the same time, many LPs—which are typically long-term, if not multigenerational, investors—are pressing firms to focus on environmental, social, and governance (ESG) metrics, rather than financial performance alone. Given these trends, the PE sector has an opportunity to be a leader in ESG investing and to contribute to efforts that address ongoing social concerns around the world.

Three Priorities

To become a top performer, or remain on top, PE firms must take definitive measures to improve their operations. Specifically, we believe they should do the following.

Turn their operational playbooks inward. The current golden age of readily available capital creates an opportunity—in fact, a near imperative—for firms to grow and to better define their market positions. The need to differentiate is not new; firms have struggled to stand out for at least the past decade. Yet in an increasingly crowded industry, it is critical that firms establish a clear point of view and a replicable means of creating value from portfolio investments—one that differentiates them from the competition in the eyes of LPs and gives them a competitive advantage.

The choice of market position will naturally point to a specific operating model that firms will need to develop. But almost all PE firms hold their own operating models in high regard and are more likely to scrutinize the operational playbooks of their portfolio companies than they are their own. For most firms, the biggest priority in improving the operating model is digital technology. For example, many PE funds, especially those in the midmarket, are recognizing the need to digitize. Among clients, we see firms creating new positions, such as digital directors and chief digital officers, whose sole responsibility is to drive the digital agenda. (Other firms are creating a digital transformation position tasked with assessing the potential of digital initiatives at portfolio companies.) These are nascent efforts, however, and most firms can do far more.

In terms of sourcing, firms need to understand the disruptive effects of new technology in the industries where they have—or plan to make—portfolio investments. The impact from digital disruption will almost certainly outweigh any kind of cost-reduction initiative or operational streamlining.

Internally, firms can digitize core functions, which will improve efficiency and allow the firms to invest in and manage larger portfolios of assets. For example, digital technology can streamline standardized communications, such as quarterly reports to LPs and investment committees. Digital processes can also help firms manage financing terms more efficiently and set up automated triggers and alerts related to financing affirmative covenants. And networking tools within the broader PE ecosystem can connect bankers, consultants, and other stakeholders, as well as manage incentives, such as broken-deal fees for transactions that don’t actually close.

Develop a true talent strategy. Of course, digitization—indeed, any improvement initiative—is simply not possible without the right people to make it happen. Yet most firms must step up their efforts in talent management. Many big firms have enjoyed a meteoric rise from small shop to big, multiasset management firm in a very short time. The talent models that served them well until recently are no longer appropriate for organizations that are now far more sophisticated and complex. Today, given the massive shifts in the sector—particularly the evolving relationships with LPs—firms must excel in managing their own talent.

To begin with, they now need to build teams with a wider range of experience and expertise—former investment bankers and consultants, as well as executives who were leaders in their industries. Firms also need people with highly developed digital skill sets at all stages of the investment process—on the deal teams evaluating the opportunities, in the portfolio companies anticipating digital disruptions, and in the funds themselves, to digitize internal processes and procedures.

Succession planning is a similar challenge at many firms, especially those whose founding partners are close to retirement, have equity stakes in the company, and are key players in LP commitment agreements. We have seen instances in which a lack of succession planning led to LPs’ withdrawal from commitments, internal fighting among members of the leadership team, plummeting morale, and the departure of star performers, among other things. In our experience, the best succession plans come from the very top, where founders help identify the next phase of leadership, communicate decisions throughout the firm in a transparent manner, and institute a phased plan for their eventual departure. The advent of minority positions that are being taken by secondary funds is one method being used to monetize and disentangle historical equity stakes held by founders.

The last area of emphasis for talent is diversity. Increasingly, LPs are signaling that they want to see more women in firms’ management ranks and more diversity across other dimensions. Continued pressure, coupled with shareholder sentiment influencing publicly traded funds such as the Carlyle Group and Blackstone, will have significant impact on the makeup of PE management teams.

The sector’s leaders are listening—and acting. Kohlberg Kravis Roberts recently hired a head of diversity and inclusion and established a council of senior partners to oversee the firm’s efforts. Blackstone, for its part, has a program that brings high-achieving junior women to the firm’s New York and London offices each spring to give them early exposure to finance and business through interactive information seminars, networking, and critical-skill-building sessions. The initiative is one of several at the firm designed to attract women to the investing side.

Upgrade their approach to value creation. In our experience, PEs almost universally—and justifiably—view themselves as paragons of value creation. Yet classic operational improvement programs, such as “check the box” exercises to reduce costs and boost revenues, are hitting their limits of effectiveness. Similarly, the relatively passive, monitor-only approaches of yesteryear are no longer enough; industries as varied as retail and health care are being jostled and jolted so much that today’s portfolio businesses require constant interaction, exposure, and insights from experts—either internal or external—as well as a constant recalibration of the growth assumptions behind the investments themselves.

The bottom line: firms need a fresh look at the way they interact with their portfolio companies, moving away from merely acting as a source of private capital and toward true strategic partnerships. Leading firms are rewriting the traditional value creation playbooks with innovative approaches, including the following:

- Digital and tech-focused strategies that call for much closer interactions with the management teams of portfolio assets.

- Pricing initiatives that not only seek to reduce discounts but also aim to better align price with underlying value for both B2B and B2C products and services.

- Steps to quickly improve operations at underperforming portfolio companies, unlock working capital, and free up the resources needed to fund longer-term transformations. (See “ Desperate Times Call for Effective Turnarounds ,” BCG article, November 2016.)

- A systematic approach to implement value creation initiatives across all companies in the portfolio, such as a centralized project management office at the portfolio companies.

- Accelerated buy-and-build strategies and faster postmerger integration, through measures to quickly combine organizations from a financial, operational, and cultural standpoint.

Some firms—such as Advent International, Bain Capital, and EQT—have already taken big strides in those areas. These firms don’t limit themselves to taking action in just one or two areas of their portfolio companies. Instead, they work hard to map out detailed value creation plans; they regularly tailor their top management teams depending on the competencies required; they bring in the skills needed to implement the solution; and they fully align top management with the plan. Rather than simply relying on the tools the deal team or firm knows best, these organizations continually seek out new approaches to create value.

These are challenging times for the PE industry. More money than ever is up for grabs, and many more firms are competing for it, though they are finding fewer opportunities to put it to work. Yet, just as their portfolio companies must adapt to turbulence and change, so must PE firms. They need to systematically improve internal processes, largely through digital transformations. They also need access to top talent more than they need access to money. And they need to devise new ways to deliver value to LPs. That’s a tall order, to be sure, but it’s what’s needed if firms want to capitalize on the current golden age.