Europe’s mobile industry faces a next-generation conundrum with major ramifications for mobile network operators (MNOs), policymakers, consumers, and businesses. The ability of current 4G technology to handle fast-rising traffic demand, led by exploding video consumption, is rapidly approaching its end. We estimate that 4G capacity in the typical large European city will be exhausted by 2021, and expensive and often-unpopular network “densification” measures —increasing the number of cell towers and antennas in heavy traffic areas—will then be required to handle traffic growth. Advanced 5G technologies present the best, and least expensive, way to avoid near-term densification and accommodate traffic increases. In Europe, however, thanks in part to the widespread use of unlimited data plans and relatively low prices, monetization of traffic growth is a major challenge, and investing in, and building out, 5G infrastructure already lags in countries in North America and Asia-Pacific.

While operators in Europe have not been idle—one Scandinavian telco claims to have created the first commercial 5G network—the transition is not happening broadly or quickly enough. Clearly no one benefits if Europe falls further behind. Consumers will not be able to make full use of the latest technologies and advanced applications, such as real-time translation, connected medical devices, and augmented reality. Businesses will not be able to take full advantage of the Internet of Things (IoT) and Industry 4.0 applications, which will affect their global competitiveness. European nations and the EU as a whole will not realize the full contributions that the wireless sector can make, directly and indirectly, to their economies. European countries will also find themselves at a competitive disadvantage with regard to other nations in the global arena for the development of new businesses and jobs. All of which seems unnecessary at the macro level, since research has shown that the economic payback on digital infrastructure investment is inordinately quick—often less than one year. (See Financing a Forward-Looking Internet for All , a report by the World Economic Forum in collaboration with BCG, May 2018.)

Europe and its mobile telco industry have the opportunity and the obligation to solve the problem of exponential traffic growth, but all participants—network operators, policymakers, regulators, and telco ecosystem partners—need to ramp up their commitment to 5G. As we argue in our new report , the industry must lead, with the support of the other participants. As network operators assess infrastructure investments, they need to think through the opportunities for new pricing structures and products and services that enhanced network capabilities present. Sticking with 4G is not a sustainable option. Neither is building out and operating a 5G network on 4G business models.

4G Runs Out of Room

Europe faces three interconnected problems for mobile networks: exponential traffic growth, unsustainable site densification, and little incentive to invest in building out networks.

First, cellular traffic demand continues to grow exponentially, driven largely by video applications, and we expect this growth to continue for at least the next decade. Traffic growth forecasts vary among countries and operators, but according to the Cisco Visual Networking Index, consumed gigabytes (GB) per user per month ranged from 0.7 GB to 4.4 GB at the end of 2017, and growth rates are expected to range from 30% to 58% annually until 2021. BCG’s case experience confirms this view.

This leads to the second problem: current 4G networks cannot support this enormous data growth without massive site densification, which has significant economic and social implications. Our simulations show that in a typical large Western European city (Berlin, London, Milan, or Paris, for example), network infrastructure density will need to almost triple after 2021 to accommodate continued growth. This is an unrealistic expectation given the expense, time, and unpopularity involved in adding new sites. MNOs already struggle to commission a few new sites in urban areas because of legal and regulatory issues. The lead time for new permits is long. Local opposition to new towers can be intense. In addition, already-dense network grids with low intersite distances prevent operators in many markets from further densification within current power limits.

Third, network operators have little incentive for investment. Traffic growth today is largely driven by video applications, which telcos struggle to monetize, especially in the increasing number of markets that have unlimited data plans. In fact, as the internet and associated new industries have disrupted network operators’ traditional revenue streams (such as communication and entertainment services), telco revenues have either remained mostly constant or declined slowly: the average revenue per user (ARPU) fell by about 3% from 2013 to 2018. We do not expect this situation to change, even with the introduction of next-generation, high-quality broadband connectivity.

5G to the Rescue?

The package of technologies that go under the name 5G has the ability to both substantially expand network capacity and lower that capacity’s cost since the data capacity of 5G networks is far greater than that of 4G networks, even when the latter employ the latest LTE Advanced Pro technologies. This is the result of two factors: 5G technology’s ability to use much more spectrum (hundreds of megahertz versus tens of megahertz) and new technologies, such as massive multiple-input, multiple-output antennas, which together can deliver a seven-fold increase in capacity over the current state-of-the-art 4G configuration.

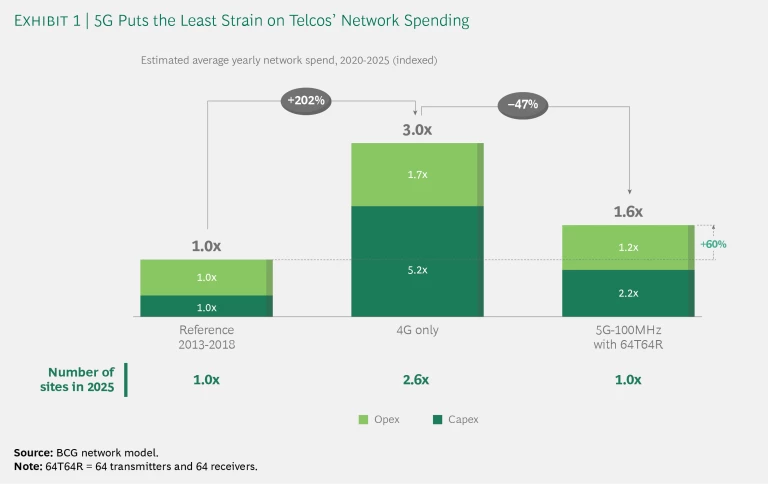

The problem is that many European telcos have little ability to monetize incremental traffic under unlimited data plans, which is illustrated by an analysis of operators’ network costs (including both capital and operating expenditures—capex and opex.). We looked at the costs for a typical operator in a large European city, starting with actual capex and opex from 2013 to 2018, the typical 4G investment cycle. Our projections showed that the costs of serving increasing traffic demand with 4G technology would triple from 2020 to 2025, driven largely by site densification. (See Exhibit 1.) Under a 5G scenario, however, an operator would not need to resort to network densification until 2025, with the exception of a few select hot spots or indoor areas. As a result, its average annual network spending would be about half of what it would be under 4G, although the absolute cost would still be 60% higher than the reference period of 2013 to 2018, which constitutes a serious financial challenge for telcos. This challenge causes mobile operators to hesitate and delay.

A 5G Playbook

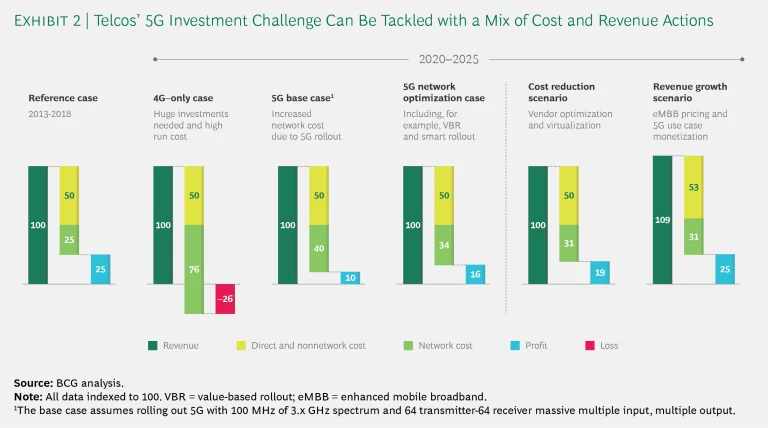

BCG has developed a playbook for the profitable deployment of 5G in Europe. We began by modeling a series of cost-lowering and revenue-enhancing measures for telcos, using as a point of reference the mobile-only revenues, costs, and profits of a typical integrated network operator for the five years from 2013 to 2018. We then built a series of scenarios based on different assumptions:

- A 4G-only case

- A 5G base case

- The 5G case applying network optimization measures (such as smart deployment and value-based rollout)

- The 5G optimized case adding cost reduction measures (including better contracts with equipment partners and tower companies, new technologies, such as automation and virtualization, and efficiencies)

- The cost reduction scenario with revenue enhancement steps, such as restructured pricing plans for 5G and developing new 5G use cases.

Notably, our increased revenue scenario shows a revenue boost of only 9%—hardly a substantial increase over six years. The results of each scenario are shown in Exhibit 2.

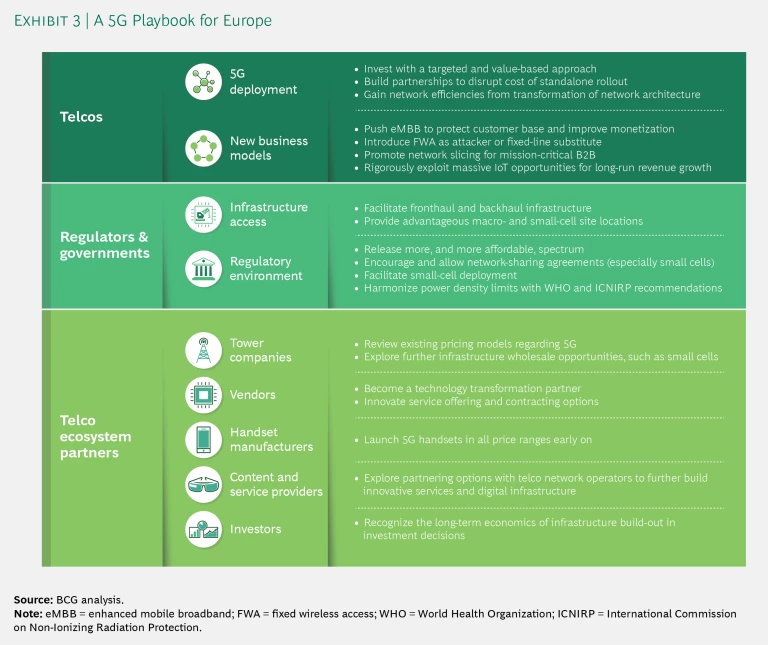

Our analysis suggests that it should be possible to drive a profit increase from 5G when either costs are reduced or the new revenue potential is larger than the (hardly ambitious) 9%. Telcos can at least match their current levels of profitability with an integrated plan that incorporates all of the network optimization, cost reduction, and revenue-boosting measures. They can also benefit from help from other players in the public sector and the broader telco ecosystem. Here are the actions each needs to take. (See Exhibit 3; full recommendations can be found in the report.)

Network Operators

More than anything, MNOs needs to change how they think about 5G, which has multiple aspects—more capacity, lower latency, network slicing by quality of service, for example—each with its own opportunities for monetization. Operators need to lower the cost of network deployment, stabilize or increase ARPUs, and create new revenue streams.

For example, our simulations show that smart deployment using a site-specific traffic forecast can improve the relationship between network capacity supply and demand, and thus reduce average network spending by 4%. Prioritizing site construction and capacity upgrades in a value-oriented way can further reduce network spending. We estimate from project experience that such an approach can reduce average network spending by 15%, with no negative impact on revenue. Smart partnerships and efficient deployment models developed on the basis of both passive and active infrastructure network sharing (often used when cost reduction is more important than network differentiation for the sharing partners) can lead to capex savings of 50% and opex savings of more than 20%. Network sharing will become more important with 5G, particularly in two areas: small-cell networks in urban and concentrated business areas, and suburban and rural regions where 5G investments otherwise could be significantly delayed by cost considerations.

Many mobile networks today operate multiple technologies—such as 2G, 3G, 4G, and narrow-band IoT—and require a significant degree of manual intervention, which increases complexity and cost. Operators that do not have legacy infrastructure and can employ a high degree of automation can benefit from a significant cost advantage. As others shut down inefficient legacy 2G and 3G networks, they will also need to work toward much more automation and virtualization to help manage the rising cost and complexity of the remaining networks.

Some operators also have the opportunity to repurpose 4G equipment from urban to suburban or rural sites. This can help them deploy 5G at more sustainable network spending levels without compromising on the value creation of new use case and applications.

There are also multiple opportunities in 5G deployments for MNOs to expand existing revenue streams and develop new ones. These include enhanced mobile broadband, which is both a key to protecting their current revenue base and an opportunity to price 5G as a new technology because it delivers better customer experience and quality. Network operators can use fixed-wireless access (FWA, also known as wireless to the home) to enter fixed-line broadband markets. The business cases for 5G FWA vary strongly by market, wholesale environment, competitive setting, and available infrastructure, but we forecast an average revenue contribution of 5% to 10% for MNOs in 2025.

Network slicing enables multiple virtual networks to run on a shared physical infrastructure. With this ability, operators can offer dedicated networks to service providers with mission-critical needs—emergency services, industrial automation, and medical devices, for example—including companies, such as railways, that have built their own dedicated wireless capabilities. Devices and sensors on the so-called massive IoT (such as those in smart homes and capillary networks) have their own set of network requirements that differ from those on the critical IoT (devices with mission-critical applications). Networks using 5G are well suited to serve customers needing low-power, low-bandwidth connectivity that can handle lots of low-energy devices emitting combined high quantities of data. Moreover, these networks can be deployed quickly and with limited capex.

Policymakers and Regulators

As with telcos, policymakers and regulators need a change in thinking and approach on the part of public-sector stakeholders. Past policy has focused on incentivizing competition and keeping prices low, which have benefited consumers and underpinned development of a competitive market. Today, however, with traffic rising and ARPUs stable or falling, the new priority for both policy and regulation should be investment, especially in the next-generation infrastructure that can enable further technological advances. In most markets, current policy and regulations actually inhibit investment in advanced infrastructure.

A number of areas are ripe for reexamination. In our 2018 report with the GSMA, Delivering the Digital Revolution , we identified six areas in which reform could collectively cut operators’ network opex and capex costs by approximately 30% to 50%. These include the following:

- Access to fronthaul and backhaul infrastructure

- Access to advantageous site locations for macro and small cells

- Additional, affordable spectrum

- Freedom and incentive to establish small-cell network-sharing agreements

- Regulatory facilitation of small-cell deployment

- Harmonized power density limits based on recommendations by the World Health Organization and the International Commission on Non-Ionizing Radiation Protection

In addition to the above, governments are also in an excellent position to lead by example—implementing technology in the public sector that requires or incentivizes deployment of 5G.

Telco Ecosystem Partners

A number of nonoperator participants in the telco ecosystem can also facilitate deployment of 5G. Tower companies need to develop their own business models for 5G. In particular, pricing, which is often based on antenna size and weight, could be reviewed and potentially reworked to incentivize operators to accelerate 5G rollout. Tower companies can also play a key role in advancing smart network sharing among operators.

Telco vendors, such as equipment makers and software companies, need to work closely with their operator partners to pilot 5G equipment and make sure that operators are aware of the technological possibilities that 5G encompasses. In addition to their commitment to robust 5G roadmaps, network vendors can develop planning tools for the most effective deployments for their telco clients.

Handset makers need to design, test, manufacture, and distribute 5G-ready handsets in parallel with the still-evolving development of 5G technical specifications. Handsets also need to be able to work on both legacy and new 5G networks, in particular the 3.x GHz band, which will be the major capacity band for 5G in the near term.

Over-the-top (OTT) content and service providers benefit from 5G digital infrastructure, which enables them to enhance their offerings and create innovative new products. The largely cost-free content and service delivery approach taken by OTT companies in the past may be less effective in this transition, especially because ultra-low latency is an important feature for advanced services, and service providers will want to integrate their offerings into the telco infrastructure for that. OTT players should explore partnering options with network operators to build innovative services that depend on advanced digital infrastructure.

Investors need to understand the underlying economics of 5G network rollout and transformation. The upfront (peak) investments in the 5G cycle will be higher than the ones associated with 4G, and investors may need to adopt a longer-term perspective when considering how they deploy their capital.

Europe needs to catch up. If it does not, the deployment of 5G will be delayed and fragmented. In addition to the telecommunications industry, the losers will include Europe’s consumers, businesses, and national economies. If, on the other hand, the stakeholders of the mobile ecosystem pull together, Europe’s telcos—as well as its consumers, businesses, and nations—can all stand among the winners in the mobile and digital economies of the future.