The takeoff of electric vehicles (EVs) has hit full velocity. By 2030, roughly one-quarter of all cars and light trucks on the road will be EVs, including hybrids and fully electric vehicles.

The rise of EVs is part of a broader shift toward electricity as the fuel of choice for mobility—what is known as transportation electrification (TE). This change includes not only the development of EVs but also the modification of infrastructure, such as roadways and ports, to allow charging. The shift has major implications for utilities. They must prepare to meet the energy demands posed by TE in a way that positions them to be both the drivers and the beneficiaries of the transition. There is significant opportunity for utilities that are able to do this: Boston Consulting Group estimates that the rise of EVs could create $3 billion to $10 billion of new value for the average utility.

The rise of EVs could create $3 billion to $10 billion of new value for the average utility.

To capture that value, utilities must take action in three areas. First, they need to make smart investments to enhance grid infrastructure. While the net impact on total kilowatt hours (kWh) of energy demanded by EVs will not be massive, the capacity of the grid (in terms of total kilowatts) will need to expand to handle surges in demand in certain locations and at certain times when charging is common. Second, they need to support governmental TE efforts and policies. Utilities can take a variety of actions to support TE, including developing new rate plans, rebates, and promotions. Third, they should enter new markets with EV-related products and services, such as installing, operating, and maintaining EV charging equipment.

Utilities should plan now and then act right away to overcome challenges to the realization of value from TE. This includes creating a vision and plan for TE, establishing clear governance and cross-functional collaboration, ensuring effective planning and execution of new TE-related projects, developing new capabilities to succeed in the EV era, and adjusting to the much shorter planning and execution timelines for TE-related opportunities. Utilities that fail to move aggressively will cede the opportunities—and value—created by EVs not only to other utilities but also to savvy players, such as car makers and oil and gas companies.

Electric Vehicles Go Mainstream

The future of the auto industry has come into focus—and it is electric. Over the next dozen years, four factors—technology, regulatory mandates, consumer adoption, and autonomous-vehicle and ride sharing—will propel and shape the transition to EVs.

Technology, regulatory mandates, consumer adoption, and autonomous-vehicle and ride sharing will propel and shape the transition to EVs.

Technological progress, which is driving a steep decline in EV battery costs, is perhaps the most potent force. The cost per kWh of an EV battery, which constitutes the largest share of total cost of ownership (TCO) for plug-in hybrid and fully electric cars and trucks (known as battery EVs), has decreased from $700 in 2009 to a range of $150 to $175 in late 2017. And it is expected to continue to decline, hitting $80 to $105 by 2025 and $70 to $90 by 2030. As battery costs decrease, the economic case for buying an EV rises. We estimate that in the US, the five-year TCO for a battery EV will be lower than that for a vehicle with an internal combustion engine by 2028. In addition, government policies and regulations are driving purchases of EVs. And the development of shared autonomous electric vehicles (SAEVs) will likely fuel even greater momentum in the years ahead.

As these forces gain strength, EV market share will expand. By 2030, we expect EVs—including mild and full hybrids, plug-in hybrids, and battery EVs—to account for 50% to 60% of new-car sales and 21% to 27% of all light-duty vehicles (such as passenger cars and SUVs) on the road. The vehicles that will have the most impact on utility operations—plug-in hybrids and battery EVs—will account for 20% to 30% of new sales and 7% to 12% of all cars and trucks.

A Massive Value Creation Opportunity for Utilities

Of the three types of TE opportunities for utilities, the first two—enhancing the grid and supporting TE policy—are generally regulated activities. The third—entering new product and service markets—may or may not be regulated, depending on the specifics of the market. Assuming that EV adoption ramps up as outlined above, these three opportunities could create an additional $3 billion to $10 billion in value through 2030 for an average utility with 2 million to 3 million customers. This comprises investments that the utility will make to support EVs and that will be included in the rate base. (See Exhibit 1.)

Enhance the grid. Utilities will earn a return on capital investments in the new grid infrastructure that is required to meet the increased demand from EVs. The bulk of this investment will need to be made in distribution.

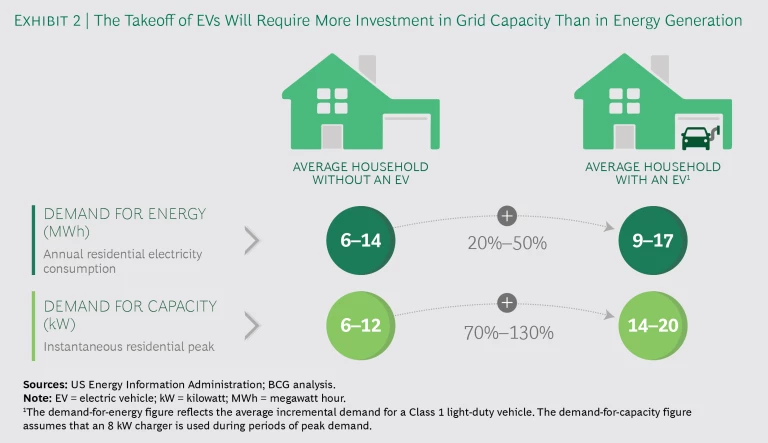

These investments will be primarily related to increasing capacity—the amount of energy that can be delivered at one time—as opposed to increasing overall electricity production. That’s because we expect EV penetration to have a relatively small impact on total energy demand (including residential, business, and industrial uses) through 2030. However, significant increases in demand in certain locations or at certain times of the day will stretch the capacity of the current grid.

Stretch it by how much? Looking specifically at the residential sector, the addition of a charger that can recharge an EV in four to six hours would lead to an increase of 20% to 50% in megawatt hours of electricity consumed by the average household. When you consider that such increased consumption will be spread out throughout the day, however, the amount of increased energy generation capacity that would be required for the system as a whole (including commercial, industrial, and other sectors) is not massive. By contrast, charging that EV would require a much larger increase—70% to 130%—in grid capacity for the average household. (See Exhibit 2.) That increase in demand is roughly equivalent to the addition of an entire new home in the neighborhood. At the same time, the installation of public chargers, especially commercial rapid chargers, will put even more strain on the grid.

Ultimately, the amount of investment to boost transmission and distribution capacity required by an individual utility will depend on the degree to which utilities can successfully encourage EV owners to charge their vehicles during periods of relatively low demand and in locations where the capacity of the grid is not constrained. Assuming that the market share for battery EVs ramps up from 1% to 15% from 2019 to 2030, we project that the required transmission and distribution upgrades will range from $1,700 to $5,800 for each electric vehicle that comes online, depending on when and where people charge. That translates to an estimated $1.8 billion to $6.2 billion in cumulative value from grid enhancement by 2030 for the average utility.

Take action to support TE. The rise of EVs and TE poses a win-win scenario for utilities and policymakers. TE will allow utilities to add customers and load to the grid while supporting the environmental and policy goals of regulators.

To capitalize on that win-win opportunity, utilities need to develop a clear strategy for supporting TE. In particular, they will need to communicate clearly to regulators how their programs and actions align with overall regulatory goals. As part of their strategy, utilities should also develop solid EV-related objectives and metrics. These can include the projected effect the utility’s EV strategy will have on greenhouse gas emissions in their territory, total expected EV-related investments and the resulting impact on rates, and targets for EV adoption in disadvantaged communities.

To capitalize on that win-win opportunity, utilities need to develop a clear strategy for supporting TE.

With such a strategy in place, utilities should move ahead aggressively to execute. To stimulate the EV market, utilities can offer EV-specific rates, assist with customer adoption, provide rebates and promotions, and construct “make ready” charging-station infrastructure. As more EVs charge, electricity load will increase. Forward-looking utilities are beginning to implement lower rates for EV charging during off-peak periods. They are also starting to experiment with dynamic pricing through smart chargers to shift charging to off-peak or mid- or shoulder-pricing periods. And they are likely to introduce entirely new rate designs, potentially including such approaches as subscription plans for electricity services. A subscription plan could, for example, impose a fixed fee for EV charging on customers, providing them with a free smart EV charger that automatically shifts charg-ing to periods of low overall demand on the grid.

At the same time, utilities should take aggressive steps to support the development and adoption of SAEVs—a trend that will be a powerful driver of demand for EVs overall. (See the sidebar “The Potential of Shared Autonomous EVs.”)

The Potential of Shared Autonomous EVs

The Potential of Shared Autonomous EVs

Mobility is being disrupted in a major way. Among the biggest shifts: the emergence of shared autonomous vehicles. As this trend takes off, it will fuel demand for EVs that are well suited to fleets of shared autonomous vehicles. That’s why utilities should take steps now to support the development of the shared autonomous market.

Consumers today are increasingly balking at car ownership and leveraging a connected world to hail rides and share vehicles. Automation will eliminate the need for a human driver, dramatically lowering costs and enabling greater vehicle utilization. It also has the potential to improve safety and address any lack of trust and confidence in ride sharing.

We expect the owners and operators of shared autonomous vehicle fleets to gravitate toward EVs as the fleets assume a bigger share of the vehicle customer base. That’s partially because the EV total cost of ownership is declining rapidly. But it’s also because, unlike individual consumers, fleet owners and operators won’t have to worry about how far EVs can travel on one charge: they can switch vehicles as needed and route autonomous vehicles to charging points. In the long run, a shared autonomous electric vehicle (SAEV) will provide lower operating costs for fleet owners because of reduced maintenance, no driver wages, and higher utilization. For these reasons, SAEVs will eventually dominate in such categories as ride-sharing commuter cars, taxis, mass-transit buses, commercial vehicles, and heavy trucks.

Utilities in both the regulated space and the unregulated space will need to strike new partnerships, influence customer behaviors to adopt shared autonomous vehicles, and pilot technologies to speed SAEV adoption. At the same time, they need to anticipate and plan for the increased load demands that SAEVs will put on the current grid. This should include striking new partnerships to pilot, test, advance, and scale technologies that will help control the highly localized demand that will come with the mass adoption of SAEVs. And their efforts to support TE overall, including through innovative rates and education programs, become even more critical given the coming market shift toward large SAEV fleets.

Ultimately, utilities will find that supporting the shift to SAEVs will be one of the most powerful ways to fuel demand for EVs overall—and create new value for their business.

Already a number of utilities are moving to seize some of these opportunities. In California, regulators have approved roughly $1.1 billion of TE-related expenditures by the state’s three large investor-owned utilities: Southern California Edison, Pacific Gas and Electric, and San Diego Gas and Electric. These expenditures include rebates to encourage the installation of residential chargers, a program to support charging infrastructure for medium- and heavy-duty vehicles, and a program to drive the electrification of infrastructure at the Port of Long Beach.

We estimate that the cumulative value from supporting TE will range from $50 million to $1 billion through 2030, or roughly $50 to $950 per EV, for the average utility. This range reflects the wide variation in policy and regulatory support regimens across jurisdictions, with the high end representing the opportunity for utilities in states that have ambitious TE targets, such as California and New Jersey.

Enter new competitive markets for TE-related products and services. TE creates new product and service opportunities for utilities. They include EV operations and maintenance; the installation, operation, maintenance, and servicing of EV charging points; software solutions for such things as energy management and fleet routing; and consulting services.

Already, some utilities—including Innogy, Enel, E.On, and Vattenfall—have emerged as end-to-end owners and operators of charging infrastructure, covering installation, operations, maintenance, and service.

Given the relatively low penetration of EVs today, an immediate push into charging infrastructure does not make sense for all players. That’s because, until EV penetration reaches a high level, any given charging point will have a low utilization rate. As a result, it will be difficult for utilities to introduce public charging in many markets without subsidies or the development of creative revenue opportunities.

However, utilities can take steps now to build an ecosystem that supports EV demand while also positioning themselves to compete in the charging-infrastructure space. New partnerships with EV manufacturers or large fleet owners—such as ride-sharing companies or public transportation operators, for example—can increase charge point utilization. In Madrid, Endesa and Car2go rolled out an EV fleet of 500 cars with charging points; and in Sweden, Vattenfall has partnered with Volvo to deliver, install, and service charging boxes for Volvo EV owners.

In addition, utilities can explore value-added services that improve the economics of charging investments. Among the possibilities: bundling charging with other services, such as parking and roadside assistance, grocery or package delivery, and EV maintenance and repairs.

There may also be opportunities in vehicle-to-grid (V2G) technologies, which allow EVs to deliver power and energy services back to the grid. Auto manufacturers have already started developing these capabilities. Nissan Motor, for example, is offering a V2G system and home battery pack that allows consumers to both provide energy services to the grid and store energy for use in the home. Certainly, the long-term potential of V2G is unclear, especially given the potential reduction in total battery life from providing V2G services. Still, utilities should monitor the technological development in this area for emerging revenue opportunities, such as the distribution services for companies manufacturing V2G equipment.

The new product and services opportunities vary widely—and, as a result, so do our estimates of potential value for the industry. Given that a core offering for utilities may be the provision of EV operations and maintenance (O&M) services, we used the costs of O&M services for consumers as a proxy for the value of these services. As a result, our projections in this category are fairly conservative. Our low-end value is based on expected O&M costs for EV owners, while our high-end value is based on O&M costs for owners of internal combustion engine vehicles. Assuming that each vehicle is driven about 13,000 miles per year, we estimate the cumulative value of new TE-related products and services to be $3,400 to $7,400 per EV from 2019 through 2030. This implies a value of $1.3 billion to $2.9 billion for an average utility with 2 million to 3 million customers.

Surmounting Challenges to Success

First movers will be able to shape—and capture—the value created by TE. And other players, including those in the oil and gas and auto industries, are already staking their positions. That’s why it is critical for utilities to plan now and act right away to influence and support TE regulation and policy and position themselves at the center of TE ecosystems.

Utilities must take six actions to address the key challenges they face in pursuing a new, fast-changing business opportunity:

- Ensure alignment around their vision for TE and a clear strategic plan to support it. Utilities operate in a complex environment, where they must support the goals of regulators, minimize rate hikes for consumers, and comply with federal and state policies. Creating alignment with all stakeholders about the vision for TE, therefore, can be a formidable exercise. Utilities that succeed in doing so will be better positioned than others to build a strong portfolio of new programs and offerings.

- Create an ecosystem of partners to help expand the variety of EV-related products and services that utilities provide. Utilities have not typically needed to do this in their core business. And, in the past, many have struggled to build the right network of partners when pushing into new service offerings. But given the speed with which the EV market is developing, and the complexity of products and services opportunities that are emerging, partnerships will be critical. Utilities need to link up with players along the value chain to make sure that their offerings are competitive and reliable.

- Develop effective cross-functional collaboration in organizations that have traditionally been highly siloed. This should include, for example, driving collaboration between customer-facing teams that work with EV customers and grid engineers who make sure that customers have a seamless experience when setting up their EV chargers. Such collaboration requires new ways of working and can be particularly challenging in an industry long characterized by a predictable mission and, as a result, strongly prescribed roles.

- Enable well-coordinated planning and implementation, both for broad utility efforts on initiatives such as grid enhancement and for individual TE programs. Too often, there is little coordination of various programs across the company, resulting in fragmented efforts that have less impact than they could otherwise.

- Build new capabilities for the TE push. This includes skills and expertise in charging-infrastructure engineering and construction, data and analytics, development of go-to-market approaches, customer experience, and the management of the B2B sales process.

- Adjust to shorter planning and execution timelines. Traditionally, utility planning occurs over a multiyear period. And while grid-related investments and opportunities will indeed span years, the timelines for capturing TE opportunities, especially unregulated competitive plays, will be much shorter.

Given the rapid pace of disruption in mobility, it is imperative for utilities to move swiftly in each area. If they do, they will set themselves up to be drivers—rather than passengers—on the journey to large-scale electricity-driven transportation.