Power and utility (P&U) players, like companies in other sectors, are struggling to make sense of a post-COVID-19 world. Lockdowns worldwide have reduced power consumption, impacting the companies that produce and supply it. The deeper the pandemic-induced recession and the longer the economic recovery, the greater the effect on the sector.

P&U players have weathered similar shocks before. And they have responded by changing their business models, embracing new technologies to cut costs, and expanding into additional market areas.

Crises have a way of creating or accelerating transformational change. When the COVID-19 pandemic hit, the industry was in the midst of a fundamental shift away from centralized conventional generation and toward a more distributed and digital era. Regardless of how quickly the world recovers from the pandemic, we expect the crisis to accelerate this trend. Companies that reach scale in a decarbonizing world, adopt new data-driven solutions, prioritize best-in-class cost reduction programs and cash management, and identify new pockets of value will emerge as value creation leaders in the coming decade.

In this report, we analyze the historical performances of leading European and North American P&U companies to identify the key value creation drivers during the pre-COVID-19 period. We then examine the impact of COVID-19 on the sector to understand how companies should adjust their strategies to prosper in the new post-pandemic reality.

A Decade of Change

The world’s P&U companies encountered significant challenges during the past decade. Overall demand was flat and wholesale power prices were weak, but technological advances and rapidly declining costs made renewable energy highly competitive, prompting a widespread shift toward wind and solar power. In parallel, the shale revolution in the US created an abundant supply of inexpensive gas, lowering generation costs for P&U players but also depressing wholesale prices.

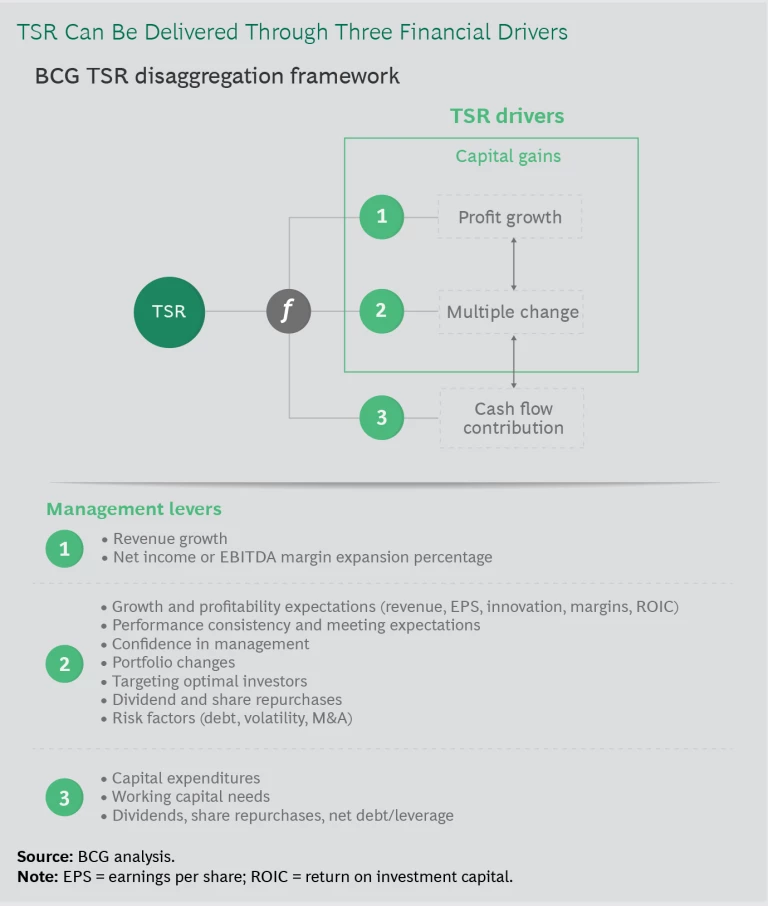

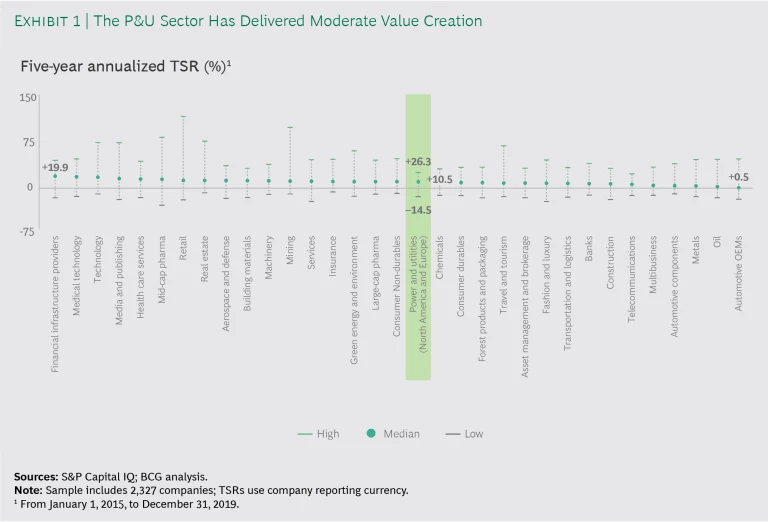

European and North American power and utility companies delivered a median annual TSR of 10.5% for the five years from January 1, 2015, to December 31, 2019.

Against the backdrop of healthy global stock markets, European and North American P&U companies delivered a median annual TSR (share price appreciation plus dividends) of 10.5% for the five years from January 1, 2015, to December 31, 2019, placing the sector in the middle of the 33 industries analyzed in BCG’s 2020 Value Creators Rankings . (See the sidebar “The Components of TSR.”)

The Components of TSR

Investors were attracted by new energy opportunities in solar and wind but also by the sector’s appeal as a relatively safe investment due to market regulation. As a result of these qualities, P&U companies had the second-narrowest spread in TSR results among all sectors, after telecommunications. (See Exhibit 1.)

Nevertheless, all players grappled with the question of how to respond to the sector’s transition toward renewable energy and distributed power generation . TSR leaders grew their renewables portfolios, built new businesses, and added new digital capabilities, although these weren’t the only actions that set them apart.

What the Data Shows

Our research included a survey of 53 P&U companies. (See the sidebar “Companies in Our Sample.”) We examined the companies’ TSR performance through four lenses: region, business model, leaders and laggards, and value drivers.

Companies in Our Sample

Our sample contained companies that focus on different points along the power and gas value chain. To account for different business models, we grouped players into three main segments according to their position in the value chain: transmission and distribution (grid) companies, fully regulated utilities, and semiregulated integrated utilities. Both fully regulated and semiregulated utilities own power transmission/distribution and generation businesses and, in some cases, retail ones. We included at least ten players from each of these three segments. We also included a small number of pure power generation companies—gentailers, comprising generation and retail but no grid business—and grid sales companies, with distribution and retail but no generation, in the sample. (See the exhibit.) We examined the TSR performance of our three main segments in more detail in the report but excluded other segments because they lacked sufficient players.

All of the fully regulated integrated utilities in our sample were based in the US or Canada. These companies had a combined market capitalization of $404 billion, making this the second most valuable segment. More than 75% of their income came from businesses in regulated markets. Semiregulated integrated utilities, in contrast, draw a significant portion of their income from businesses in more competitive regimes, such as unregulated retail or renewable power generation. Semiregulated integrated utilities, the most valuable segment, had a combined market capitalization of $747 billion, divided equally between North America and Europe.

Region

North American P&U players generally outperformed their European counterparts, delivering a median annual TSR over our five-year period of 11% versus 6% in Europe. However, the range of results in Europe was wider, indicating that the region faced greater exposure to unregulated and more volatile businesses than did North America.

In both regions, flat demand led to weak or negative sales growth during the period. But in North America, players moved out of riskier, competitive generation and into regulated businesses, boosting their EBITDA margins and valuation multiples. Actively driving industry consolidation and improving operational efficiency also helped bolster both. In contrast, dividend payouts were by far the biggest contributor to TSR performance in Europe, where changes in margins and multiples had only a small impact.

Business Model

Exposure to regulated markets contributed significantly to TSR success during our study period. Grid companies and fully regulated integrated utilities were the best-performing segments, with median TSRs of 11.5% and 11.7%, respectively, and no negative results. Semiregulated integrated utilities performed slightly worse, at 10.2%, but they also contained both the best and the worst TSR performers in our sample. The difference in results was due to the utilities’ expansion into potentially more lucrative—but also riskier and less regulated—areas such as renewable power generation and energy storage.

Although valuation multiples and cash flow contributions were important across all P&U segments, different levers drove TSR performance in different segments.

Grid Companies. Transmission and distribution players took advantage of low interest rates to invest in their networks to meet regulatory demands for increased integration of renewables, greater reliability, or improved interregional grid connections. As a result of hikes in customer bills to pay for these investments, grid companies were the only segment whose revenues grew during the period.

Fully Regulated Integrated Utilities. Improvements in profit margins and valuation multiples contributed more to the TSR performance of fully integrated utilities than to the TSR of any other segment. Like grid companies, the group benefited from investors’ appetite for resilient, more regulated businesses. At the same time, replacing operations and maintenance expenses with capital spending may have boosted the segment’s median margins. By investing in their generation assets (for example, by replacing aging thermal power plants that require high maintenance with new low- or zero-maintenance renewable capacity) as well as in their distribution networks, fully regulated players were able to improve their margins more than all other segments while keeping revenues (and their customers’ bills) flat.

Semiregulated Integrated Utilities. This segment’s TSR performance improved as a result of significant moves by some companies into renewable generation, which saw gains from declining costs and supportive government incentives. In general, semiregulated integrated utilities rewarded their investors with handsome dividend payouts. Cash flow contributions were the main driver of TSR for the segment as a whole.

Leaders and Laggards

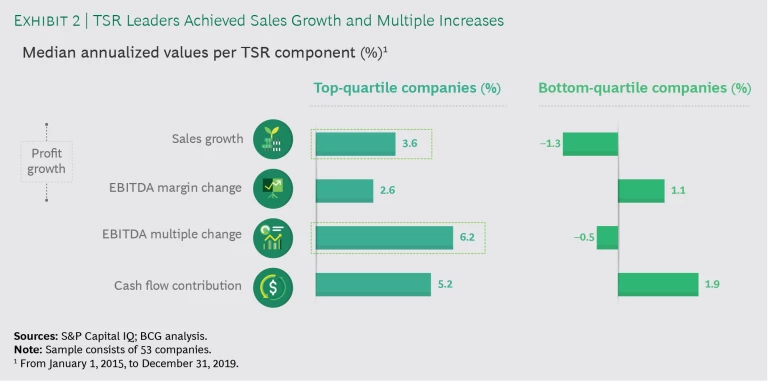

Strong yet profitable sales growth and changes in valuation multiples were key factors distinguishing leaders from laggards, although dividend payouts were an important driver of good TSR performance across our company sample. (See Exhibit 2.) And even though grid companies were the only segment to increase sales as a whole, individual players in other segments grew sales too—and some achieved double-digit growth.

Overall, top-quartile companies increased sales by a median of 3.6% per year over the five-year study period. Median valuation multiples for this group increased by 6.2% per year, as investors gained greater confidence in their prospects. The magnitude of the multiple uplift is noteworthy because it corresponds to a 35% uplift of the EV/EBITDA multiple over five years. Investors had to significantly reassess a company’s outlook in terms of either the sustainability or the growth of its business model. In contrast, sales and valuation multiples at bottom-quartile companies contracted.

Value Drivers

When we examined the key drivers that created shareholder value, we found several important trends that apply broadly to companies in the P&U sector.

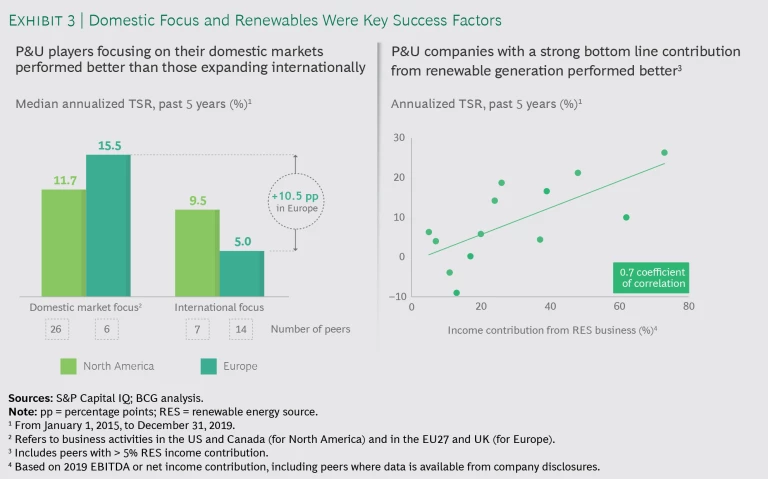

Maintaining a Strong Domestic Focus. North American and European players that focused on their continental home market and shunned further international expansion improved their valuation multiple and profit margin relative to companies with more of an international orientation. The median TSR for the handful of European players with a strong domestic or continental focus was 10.5 percentage points higher than that of internationally minded European companies, while the corresponding difference among North American players was 2 percentage points. The subsequent performance of P&U companies during the pandemic amplifies this finding, as investors penalized players with a higher exposure to emerging markets. Many companies lack the local market know-how—such as insights into customer preferences or effective regulatory management—that is essential for successful international expansion.

Players that invested in renewable energy generation and successfully adopted new technologies outperformed those with high exposure to conventional generation.

Betting on Renewables. Players that invested in renewable energy generation and successfully adopted new technologies outperformed those with high exposure to conventional generation. (See the sidebar “How the Sector’s TSR Leaders Rose to the Top.”)

How the Sector’s TSR Leaders Rose to the Top

Faster-than-expected growth in solar and wind installations—together with cost reductions, government subsidies, and the positive impact of rising prices for carbon emissions allowances on green energy sources—helped renewable players. Owing to scale effects, the greater the share of renewables in a company’s power generation portfolio, the bigger the boost to TSR performance. (See Exhibit 3.) The outstanding performance of renewables-focused utilities was visible across the entire sector. Companies such as Denmark’s Ørsted, whose shares have traded publicly only since mid-2016, significantly increased their market valuations in recent years (and would have ended up high in our ranking if they had been around long enough to have recorded five years’ worth of TSR data). However, we found that renewable ownership was highly concentrated. Just ten companies—nearly all of them European—accounted for more than three quarters of the sample’s renewable capacity.

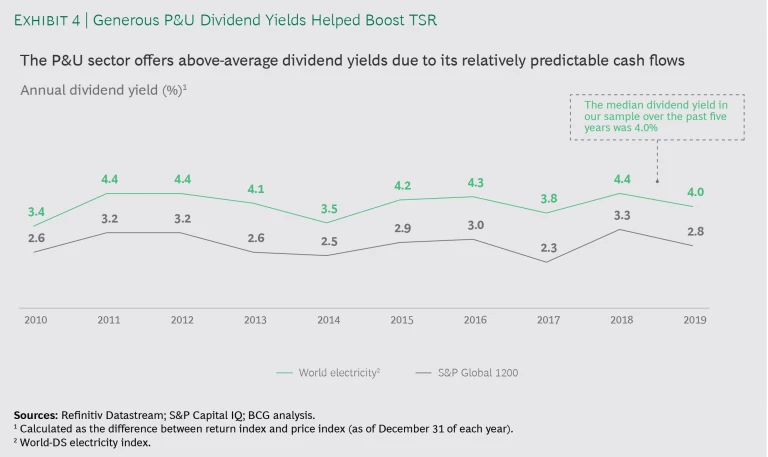

Generous Dividend Yields. For all P&U players, generous dividend yields were a relatively important value driver. While companies in other sectors typically paid dividend yields of 2% to 3%, the companies in our sample consistently offered yields of 4% to 5%, thanks to the predictable nature of their cash flows. (See Exhibit 4.) Combined with a lower risk profile due to regulation, this attracted investors seeking to reduce risk and position their portfolios more defensively.

Our analysis suggests that TSR leaders tend to operate in regulated markets where cash flows are stable and resilient. They have avoided risks arising from international expansion. They have expanded into renewables businesses. And they provide an attractive dividend play. We expect many of these factors to continue to be differentiators in a post-COVID-19 world, but players will also need to address the question of where to find future growth opportunities and tap new value creation sources. We investigate this question in more detail in the section “What Does the Future Hold?”

COVID-19’s Impact on the P&U Sector

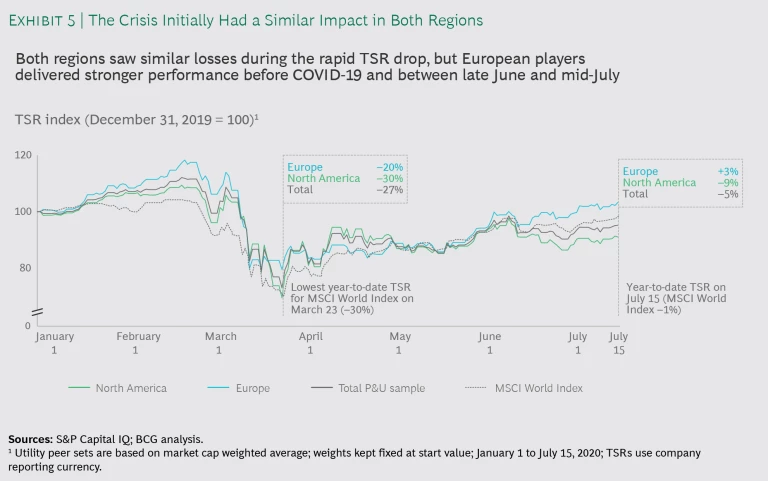

The lockdown measures introduced in response to the COVID-19 pandemic inevitably curbed the demand for power. In particular, industrial and commercial companies needed less energy, as they shuttered factories and offices and as people worked from home. The short-term impact of the crisis on P&U TSR was broadly in line with that on global stock markets. Following adoption of a wave of containment measures worldwide in mid-March 2020, the MSCI World Index (a global index covering multiple industries) hit its low point for the year on March 23, with the index’s constituent companies delivering median TSR of –30% from the start of the year. On the same day, the TSR for our P&U sample was –27% over the same period. The subsequent recovery was similar for the global stock market index and for our P&U sample. As a result, the index’s TSR from the beginning of 2020 to July 15 was –1%, while for the P&U companies in our sample it was –5%.

P&U players on both sides of the Atlantic experienced similar challenges—and a similarly steep decline in median TSR performance—due to national lockdowns. (See Exhibit 5.) In both regions, companies grappled with a drop in consumption, an increase in bad debts, and supply chain frictions. And in both, containment measures hit some business areas harder than others. For example, the profitability of P&U companies’ commercial and industrial retail businesses has come under serious threat as sharply reduced consumption left many players with excess power. Despite collapsing wholesale spot prices, some companies had to sell the surplus power back to the market, realizing significant losses and eroding years of profits in just a few months. On the flip side, sharply lower commodity prices reduced players’ power generation costs.

Regulatory actions introduced in response to the crisis impacted P&U players in both regions similarly. These measures, which include permitting customers to defer utility payments or banning disconnections, will continue to affect P&U companies going forward, increasing the pressure on companies to manage their costs and liquidity positions better and to manage their relationship with the regulator more effectively.

From late March through mid-July, the TSR performance of European P&U players recovered steadily. As a result, the median TSR for these companies from January 1 to July 15 was 3%. The median TSR for North American P&U companies has been more volatile, however, and the impact of COVID-19 on the region’s economy remains more uncertain.

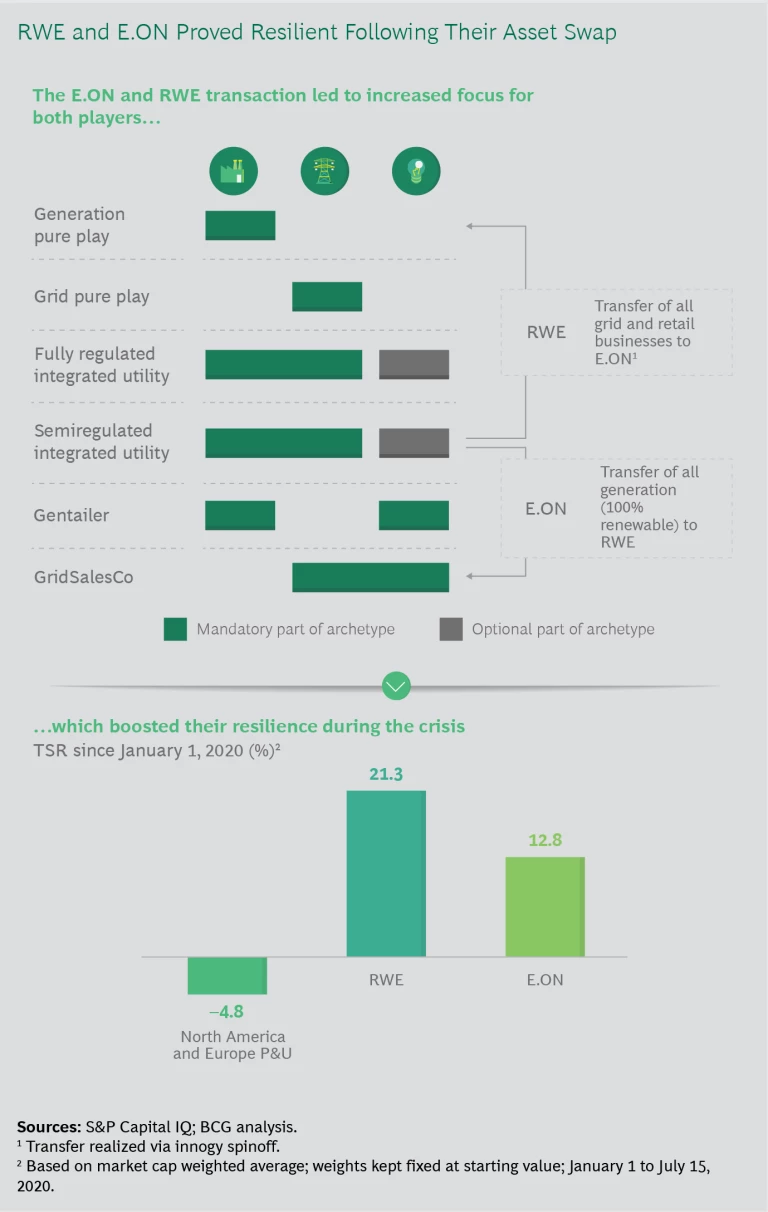

In general, P&U companies were better positioned to weather the effects of the pandemic than other sectors because they entered the crisis with a robust level of liquidity. Nearly all of the companies in our sample had a Standard & Poor’s investment grade rating of BBB– or better. What’s more, as of May, the median current ratio for companies’ last reported 12 months was 1.3, indicating that companies had enough current assets on their balance sheets to meet short-term liabilities without having to borrow. Even so, some leading companies took steps to increase their focus and resilience—and, as a result, the crisis affected them less severely than it did their peers. (See the sidebar “Creating Resilience from a Transformational Deal.”)

Creating Resilience from a Transformational Deal

Interviews conducted with investors during the second quarter of 2020 underscore our quantitative findings. Investors favored European P&U players that confirmed their short-term earnings guidance and dividend payout and showed signs of having greater resilience to the crisis in their business portfolio and geographic exposure. On the flip side, players that revised earnings and dividend guidance, or faced greater scrutiny of their cash flows due to higher international exposure and lower protection from regulations or long-term contracts, were less appealing to investors and so performed worse in the short term. Investors will probably continue to view stable cash flows as an important differentiator in the medium to long term.

What Does the Future Hold?

P&U players face multiple challenges arising from the COVID-19 pandemic, including weaker demand, lower wholesale prices, rising bad debts, and increasing cost pressures. The extent of the lockdowns in North America and Europe and the pace and trajectory of the economic recovery will determine how these challenges play out. Rather than a quick-rebound V-shape economic recovery, a longer U-shape recovery is looking more likely for many countries. Such an outcome would prolong the decline in demand, keep wholesale prices low, force P&U companies to adopt significant mitigation measures, and delay the sector’s return to its long-term growth trend.

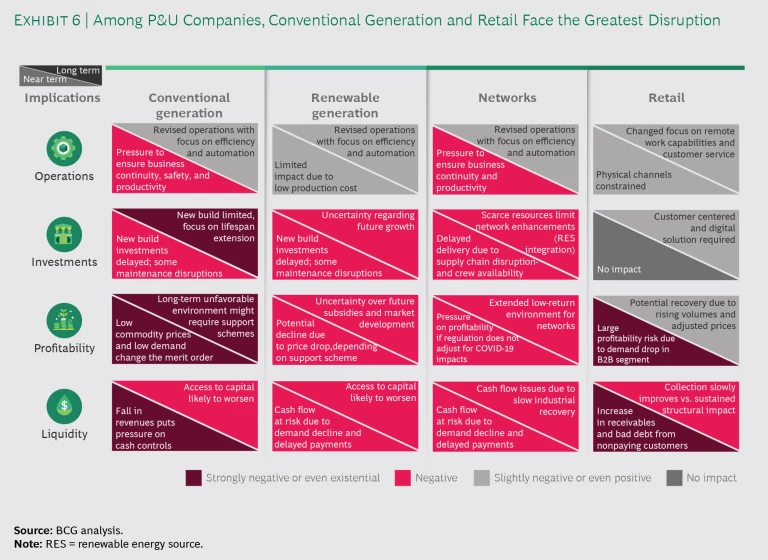

Beyond the near-term impact of these challenges during lockdown, P&U players must also manage their medium-term effects on operations, investments, profitability, and liquidity as the sector starts to recover from pandemic-induced containment measures. We expect to see different impacts in different parts of the value chain, with conventional generation and retail facing the greatest risks to their current ways of working. (See Exhibit 6.)

Conventional Generation. Following the easing of lockdown restrictions, companies’ conventional generation businesses will likely benefit from increased efficiencies and greater use of digital technologies. However, weak demand, continued growth in renewables, and changes in commodity prices might worsen the position of some conventional power generation sources in the merit order (a ranking of different energy sources by marginal production costs). Already, companies are deploying fewer coal-fired plants than in the past, and they are taking some plants offline and replacing them with cheaper and cleaner gas-fired ones. Lower utilization could significantly erode the profitability of some generating assets, requiring government support programs to make them commercially viable. In addition, a weak environment could jeopardize investments necessary to extend the life of the current fleet, while falling revenues would hamper companies’ ability to maintain healthy cash balances.

Renewables. COVID-19 lockdowns will probably have less impact on the operations of renewable energy generators than of conventional power plants, since solar and wind technologies require fewer workers to operate. Like conventional plants, renewables will also see greater efficiencies and digitization as governments relax pandemic containment measures. In recent years, renewable generators have benefited from the increased cost of carbon permits, declining technology costs, and the growing relevance of environmental, social, and governance (ESG) principles to investors in the utilities sector. These trends seem likely to continue. But the fallout from COVID-19 could still lead to reduced investment levels, greater uncertainty about future government subsidies, and lower profits, although the dangers for renewables are not as great as for conventional power plants. On the flipside, post-pandemic economic stimulus programs, such as the European Green Deal, could boost renewables as policymakers prioritize the transition to green energy.

Grid. The introduction of artificial intelligence (AI), smart sensors, and digitally enabled predictive maintenance will transform grid companies’ operations , make their field forces more productive, and help them overcome pandemic-related work- force mobility restrictions. Among other issues, companies could see weaker cash flows due to falling demand and lengthening payment delays. Large-scale improvements in energy efficiency could affect demand, especially in markets like North America, where consumption is very inefficient. The need to reinforce networks in order to increase renewables integration will continue to drive investment programs at grid companies. But the timing and extent of these investments may be uncertain, and the investments could be subject to delays. In addition, companies could face prolonged periods when the regulator requires them to accept low returns.

Retail. While lockdown measures continue, P&U companies’ retail businesses face the prospect of a steep decline in demand, especially from commercial and industrial customers, and a sharp rise in bad debts from nonpayments. Although companies in our sample generally entered the COVID-19 crisis with a robust liquidity position, demand is unlikely to reach pre-pandemic levels for quite awhile. Energy retailers’ cash flows are already under increasing pressure as a result of mounting customer insolvencies and government interventions that prohibit disconnections and allow payment deferrals. On a more positive note, however, COVID-19 will have little impact on energy retailers’ operations, in both the near term and the medium term, because of their growing reliance on digital technologies.

The Shape of the Recovery

The global drop in demand for power is already more severe than it was during the 2008 global financial crisis. According to the International Energy Agency, demand has fallen by 10% in Europe and by 6.5% in North America from pre-lockdown levels. By comparison, demand fell by 5% in Europe and by 4% in North America following the global financial crisis. Nevertheless, the P&U sector’s recovery from the COVID-19 pandemic may follow a similar trajectory, since energy demand closely tracks improving economic activity. After the 2008 crisis, demand in Europe didn’t return to the pre-crisis levels of 2007 until 2010; in North America, the recovery took even longer—between three and seven years, depending on the state. In both regions, interest rate cuts and government investment programs were responsible for the eventual pickup in demand. The sector’s recovery from COVID-19 could depend to a similar degree on governments’ economic stimulus efforts.

The accumulated earnings gap for the top 33 investor-owned utilities in North America from 2020 to 2024 is likely to be between $10 billion and $40 billion.

P&U companies’ experience during the global financial crisis suggests that they could face weak demand, lower investment, and cost pressures for a prolonged period. We expect many regulated companies in North America to miss their earnings targets for the foreseeable future, owing to lower-than-planned revenue growth, which, in turn, will increase the need to drive down costs. Depending on the path that the economic recovery takes and the annual rate increases that regulators allow, the accumulated earnings gap for the top 33 investor-owned utilities in North America for the period from 2020 to 2024 is likely to be between $10 billion and $49 billion. This amount represents between 0.7% and 3.5% of revenues—or between 6% and 30% of net income—and illustrates both the potential downside and the huge uncertainty that companies face in the current environment.

Value creation is also likely to suffer. After the global financial crisis, the sector’s TSR performance took five years to recover. Persistently low valuation multiples, weak cash flow contributions, and the impact of one-off events such as the Fukushima nuclear disaster held it back. P&U companies in North America and Europe will likely face a similarly lengthy period of low TSR in the post-COVID-19 era. As a result, companies that want to differentiate themselves in investors’ eyes must take steps to stand out from the crowd.

Preparing for a Post-COVID-19 era

The COVID-19 crisis is certain to accelerate multiple trends that were already shaping the P&U sector before the pandemic struck. Cost pressure will drive increased use of digital technologies and improved cash management, and weak profitability and investment levels in conventional power generation will support a continued shift toward renewables and adjacent business areas. At the same time, shareholders will continue to value the resilience, predictable cash flows, and stable dividends that regulated players offer. P&U players that tap these trends will be able to deliver greater value for their shareholders.

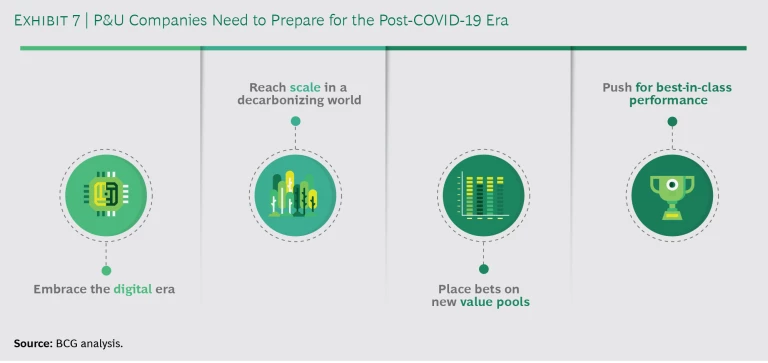

In a survey of investors across sectors, we found that 91% want companies to use the COVID-19 crisis as an opportunity to build capabilities for long-term advantage and growth—even at the expense of earnings . For the P&U sector, we believe that the following four imperatives will be especially important sources of value in the months and years ahead. (See Exhibit 7.)

Embrace the digital era. Digital technologies will be increasingly critical for P&U companies as a source of competitive advantage, allowing them to drive down costs and improve their customer offering. Indeed, digitization could be essential for companies to earn the “right to play” in the sector. Data-driven solutions and intelligent sensors will enable companies to carry out predictive maintenance, provide remote technical support and inspections, and protect themselves from cyber attacks. Digital and data will also help established P&U players’ retail businesses improve customer interactions and experiences, offer their customers additional services, and compete against nimble, inexpensive online-only challengers .

By combining their data with advanced analytics, companies will be able to unlock greater efficiencies and strategic insights. The use of AI will usher in new processes, such as guiding network company field workers remotely so that they can predict and prevent problems, as well as quickly and safely tackling outages. Digital will also be a crucial ingredient in establishing new ways of working—such as remote working and the use of agile, entrepreneurial principles for projects that require speed, flexibility, and proximity to the customer. In order to succeed, however, companies must build the right capabilities and attract appropriate digital talent.

Reach scale in a decarbonizing world. The decarbonization of the global economy will continue to drive huge change in the P&U sector and many other industries. In the long run, the share of renewables such as solar and wind in the generation mix is certain to increase. To flourish, P&U players will need to reexamine their current investment plans, prioritize renewables as a growth area, and build scale. By gaining scale in their businesses, they can reduce their operating and financing costs, develop important capabilities, and use these advantages to compete in a sector that offers shrinking profit margins. They should also consider driving consolidation in what are generally fragmented renewables markets.

ESG principles were becoming part of the mainstream for societies, companies, and investors even before the coronavirus crisis. But developments in the past few months have underlined their growing importance. Despite COVID-19, large investors, including Legal & General Investment Management and BlackRock, have reiterated their commitment to making sustainability a key part of their investment criteria. So far, ESG exchange-traded funds have performed significantly better during the crisis than they did before it began. For P&U companies, emphasizing decarbonization not only secures a long-term license to operate with environmentally minded stakeholders, but also provide business opportunities that will help others decarbonize their operations.

Some P&U companies already participate in projects to build utility-scale electrolyzers that will produce hydrogen for the steel industry. By following in their footsteps, players can expand into zero-carbon areas and benefit from government-backed green recovery programs that combine post-pandemic economic stimulus with a transformation toward lower carbon dependency. At the same time, P&U companies must be alert to risks arising from the energy transition. Although companies need to prepare for a decarbonizing world, uncertainty will continue for some time over what regulations will emerge, which technologies will prove most promising, and how quickly those technologies can become commercially viable. Companies must actively manage and continually review these risks.

Place bets on new value pools. As new power generation possibilities and technologies continue to transform the P&U sector, question marks remain over where P&U companies will find pockets of growth and value creation in future. As we have seen, conventional generation and retail face significant short-term challenges. Grid companies, despite providing stable cash flows, will feel the effects of evolving regulation and will probably have to endure prolonged periods of low returns. And although renewables will prosper in the long term, COVID-19 could have negative short-term implications for the segment.

Players should identify opportunities that they can use to build market leadership and that offer a clear unique selling proposition.

Against a backdrop of uncertainty and limited growth in many existing areas of their businesses, companies must work doubly hard to identify new value creation opportunities. A good approach is to concentrate on the needs of customers and explore energy solutions that add value and achieve customer satisfaction, while continuing to be alert to changing customer needs and preferences. Companies should not view creating energy solutions as a goal in itself, however. New solutions must reflect companies’ available capabilities. Players should identify opportunities that they can use to build market leadership and that offer a clear unique selling proposition. They should then double down on investments in the most promising areas, while also considering partnerships and opportunistic M&A to strengthen their position.

P&U companies should develop their solutions offering (whether it involves hydrogen, e-mobility, smart meters, energy storage, or household behind-the-meter systems that produce onsite power) around their existing business, balancing the imperative to tap new value pools against the requirement to use their existing core business to fund these activities. Many companies have struggled in the past. It is not enough to be clear about the what; companies also need to excel in the how, such as successfully integrating newly acquired companies or introducing innovative financing mechanisms. Unless they achieve excellence in execution, companies will fail to create the value they seek.

Push for best-in-class performance. Because of the similarity in business models across the P&U sector, companies must go further than their peers if they want to stand out from the pack. They must understand the critical value drivers in their business and professionalize all measures that help optimize these drivers. For example, many players will need to prioritize operational excellence programs that enable them to become sector leaders in profit margins by cutting costs in areas such as procurement. In an environment where all players feel pressure to keep their costs low, they must fundamentally question their cost position and consider applying a zero-based-budgeting approach . To secure the funding they need for growth and for paying out dividends, they should carefully manage their liquidity position, optimize payment collection, minimize bad debts, keep inventory levels low, and take steps to mitigate any potential financial distress they may face.

Companies should take these actions continuously rather than treating them as a one-off response to COVID-19. Savvy players will also actively engage with the local regulator so that they can participate in shaping the regulatory agenda on key issues, such as retirement of conventional power plants, greater use of renewables, and permitted regulatory returns.

COVID-19 has brought increased uncertainty to the P&U sector, creating fresh challenges for players within different segments. But while the pandemic undoubtedly constitutes a sizable dip in the road, we believe that savvy companies will continue to apply lessons they were learning before the crisis. Indeed, they will accelerate their transformation journey to become the value creators of the future.

The authors would like to thank Max Lutter-Günther, Dina Loeper, Corina Melchor, Jiemei Liu, Martin Link, and Dirk Schilder for their contributions to this report.