The Forest Imperative

The world’s forests—which today cover 30% of the earth’s land surface—are an incredibly valuable resource, storing massive amounts of carbon, helping to purify water and air, ensuring natural biodiversity, and providing livelihoods for millions of people. But despite the vital importance of forests, they are under worldwide assault, with the equivalent of 30 soccer fields disappearing every minute.

In response to the growing crisis, BCG conducted a comprehensive analysis to answer three questions: What is the financial value of global forests? What are the biggest threats to that value? How and to what extent can we preserve (or even increase) the value of forests?

Our analysis addresses the value of forests across four attributes: their climate regulatory function; their environmental benefits, such as air purification and water filtration; their commercial output; and their social value. We realize that quantification of these dimensions is difficult, and certainly always imperfect. For example, the value of forest biodiversity cannot fully be captured. Nevertheless, we believe that a valuation is essential in order to create transparency with respect to the value of forests in comparison with other assets and thereby introduce clarity to a discussion that is often dominated by emotion.

Among our findings:

- The estimated total value of the world’s forests is as much as $150 trillion—nearly double the value of global stock markets. The ability of forests to regulate the climate through carbon storage is by far the largest component of that total value, accounting for as much as 90%.

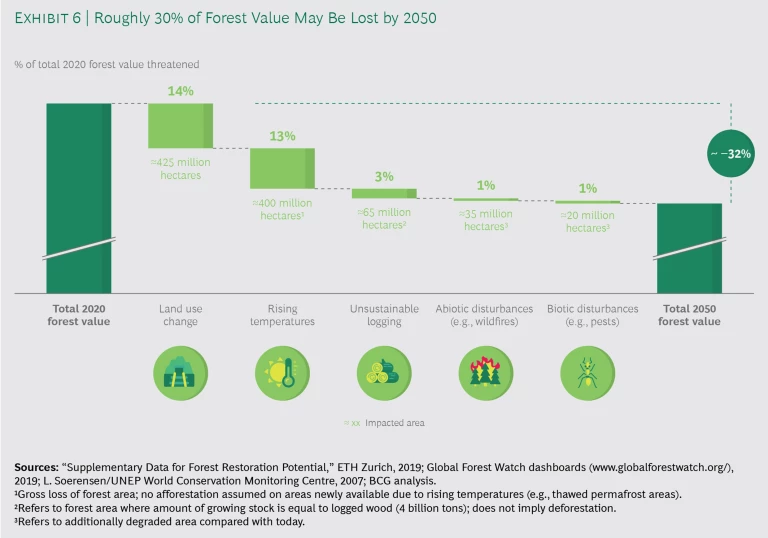

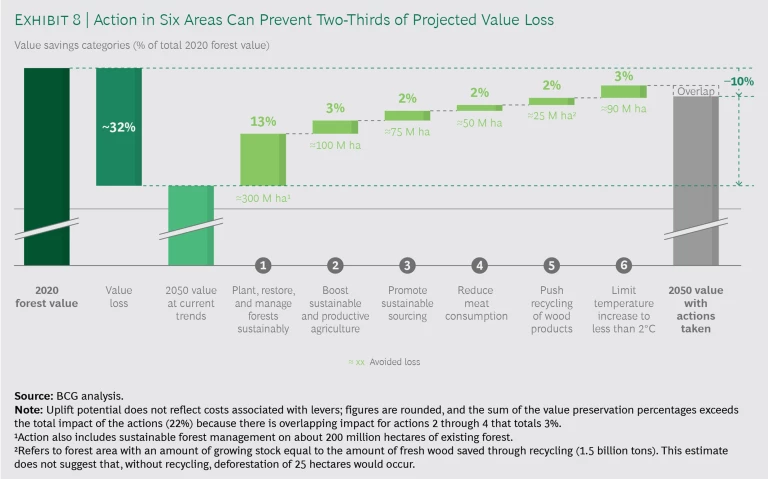

- The most serious threats are not always the ones garnering the most public attention. Recent media coverage, for example, has intensely focused on the devastation brought by wildfires. However, our analysis finds that land use changes and rising global temperatures, major drivers of deforestation, will actually be the main causes of forest value losses. Of the five primary threats to forest value that we identified, these two account for about 70% of projected losses between now and 2050. Ultimately, if the five major threats to forests today are not addressed, global forest value will drop by roughly 30% by 2050.

- All stakeholders, including governments, NGOs, the private sector, and consumers, have a role to play. Governments are particularly important and must create a robust regulatory framework that drives real change. We have identified six critical actions that can protect forests and limit deforestation—and therefore preserve forest value: (1) restore and plant forests for the purpose of protection as well as wood production, sustainably manage these and more of the existing forests, and increase their productivity; (2) boost sustainable and productive agriculture; (3) reduce meat consumption; (4) push for deforestation-free production of palm oil, soy, beef, and timber; (5) increase wood recycling; and (6) limit global temperature increase to less than 2°C. Ambitious but realistic action, including follow-through on current global pledges for forest protection, can preserve 20% of value and thus reduce value loss to about 10% by 2050.

To preserve the full value of today’s forests we would need even more aggressive steps, such as new forest plantings that cover an area larger than Australia and, critically, sustainable management of 100% of new and existing forests, up from the 40% currently.

As our analysis underscores, the value of forests and the threats facing them are inextricably linked to climate change. Existing forests store CO2 in the form of carbon on a massive scale—and young, growing forests absorb significant amounts of CO2. However, on a global scale, because of deforestation (the permanent loss of forested area) and decay, forests are now releasing more CO2 than they are absorbing—meaning forests are net carbon emitters. Depending on the actions we take today, forests will either be a powerful tool for combating climate change or a major contributor to rising CO2 levels.

If adopted, the measures we outline in this report would drive significant progress in protecting forest value—something that must be achieved if society is to ensure a sustainable planet for future generations. With a collective push for action, we can preserve a supremely valuable, but increasingly endangered, global asset.

The Value of Forests

Few of the numerous publications on forests offer a comprehensive yet easily understandable overview of forest value. To help fill this gap, we studied the current state of forests around the world and developed a methodology for valuing them.

An Overview of Forests

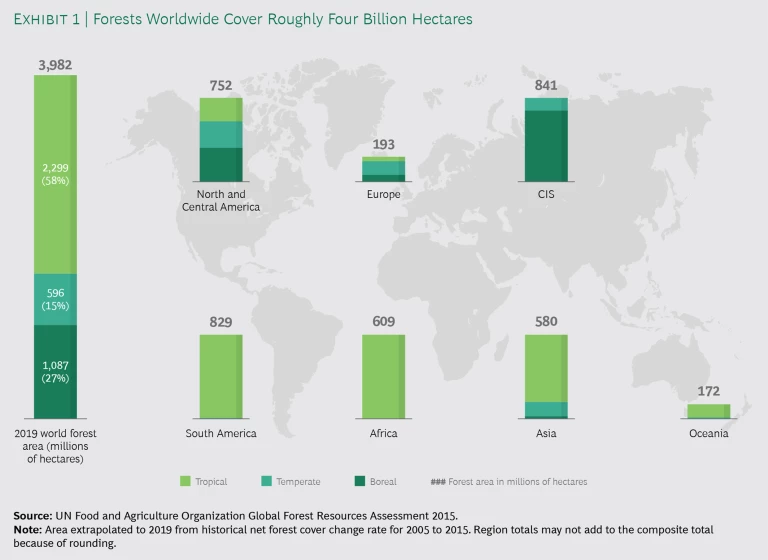

Forests today cover nearly 4 billion hectares around the world. They are found in almost every region, but their sizes and compositions differ greatly among continents and countries (See Exhibit 1.) Five countries jointly account for more than half of the global forest area: Russia (20%), Brazil (12%), Canada (9%), US (8%), and China (5%).

From a biological perspective, forests are categorized according to their biome: tropical, temperate, or boreal. The differences between forest biomes are determined largely by precipitation patterns related to temperature. Tropical forests are generally located close to the equator and are concentrated in South America (including the Amazon), Africa (primarily the Congo Basin), and Asia (largely in Southeast Asia), where they cover roughly 2.3 billion hectares. Boreal forests, about 1.1 billion hectares in total, are found in the coldest regions, mostly North America, Northern Europe, and Russia. Temperate forests are located between tropical and boreal forests, covering roughly 600 million hectares in regions such as North America, Europe, and China.

Tropical forests can capture and store more carbon in their biomass than other forest types owing to their fast-growing and very dense trunks, canopies, and roots. In addition, thanks to the mild climate in which they grow and the fact that much of their acreage remains undisturbed, they are the most biodiverse, providing a home for many more species than do the other two biomes. Temperate forests, meanwhile, are the smallest biome (accounting for 15% of total forest area) but account for an outsized share (29%) of global forest product output. That’s because they’re generally more easily accessible than the other types of forests, are relatively dense compared with boreal forests in particular, and are often managed using processes that make them highly productive. (See Exhibit 2.)

It is also instructive to assess forests in terms of the type and degree of use by humans. Commercially used forests, such as plantations and natural forests that are used for production, are major drivers of carbon capture and storage through the young, growing trees they hold and the wood products that they yield. Other forest types include those that have limited or no commercial activities today, such as inaccessible primary forests and mixed-use forests. Primary forests are forests with high levels of biodiversity but no visible indications of human activities. Mixed-use forests have portions that are undisturbed and portions that are used commercially.

Quantifying the Value of Forests

Drawing upon previous research, we developed a methodology for valuing forests. This exercise can drive a concrete discussion about the asset value at risk, the impact of certain actions to preserve that value, and, by extension, the amount we should be willing to spend to implement those actions.

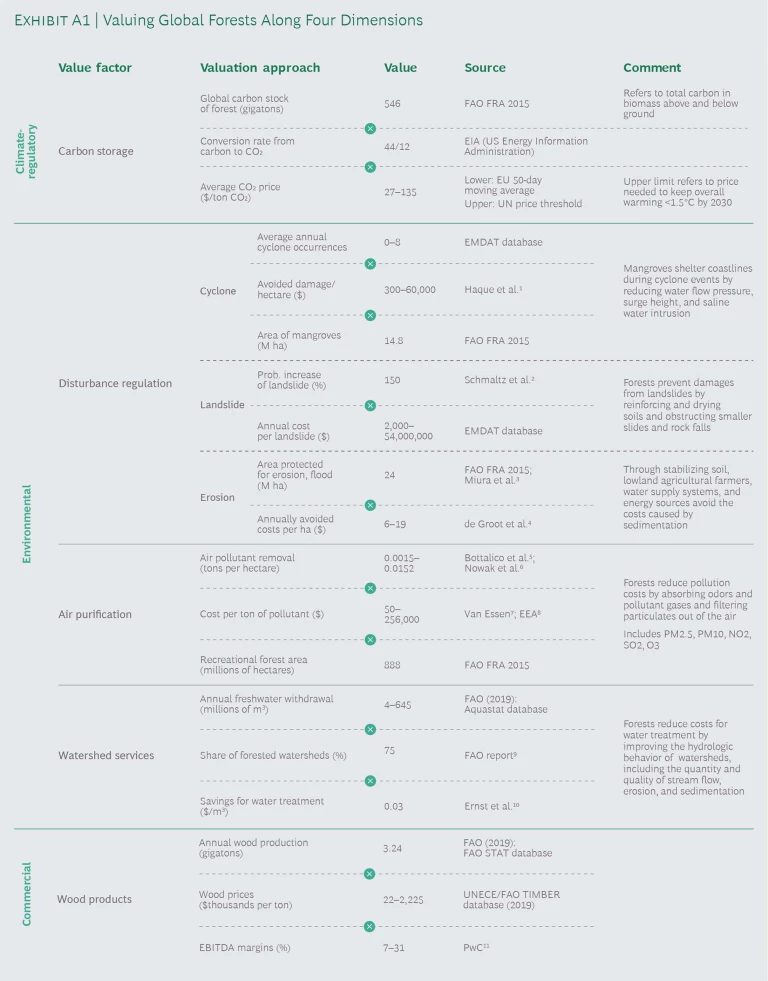

Our goal was to capture the full value of global forests, not simply the value that can be extracted through commercial activities such as harvesting timber. Consequently, our analysis assesses value in four dimensions—climate-regulatory, commercial, environmental, and social. We are not looking at the value in just one year; rather, we are calculating the cumulative value in all four dimensions in perpetuity, much as one would in valuing a stock. This approach makes sense given that forests are a self-sustaining asset that will continue to provide benefits into the future.

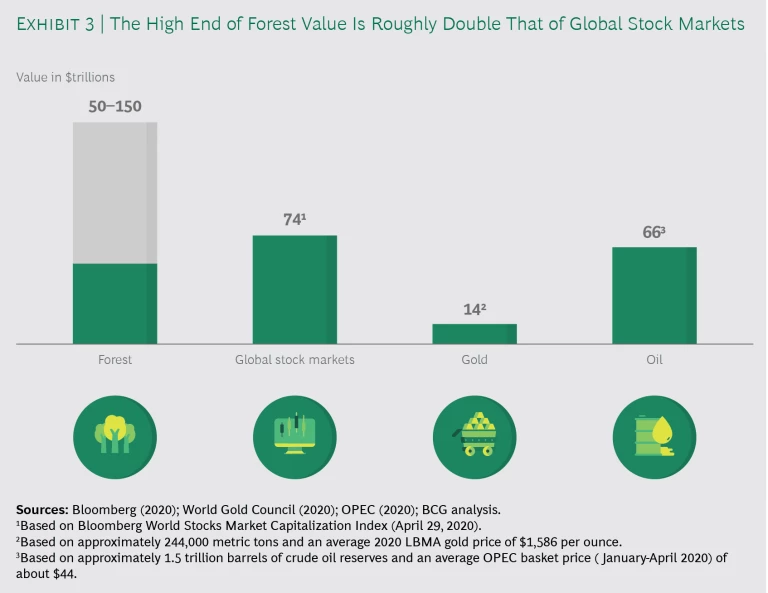

Our analysis reveals that the total value of forests is $50 trillion to $150 trillion—with the upper limit being roughly double the value of global stock markets and more than ten times the value of the world’s gold, including reserves. (See Exhibit 3.) It is worth noting that this is a conservative estimate; we consistently used figures based on academic consensus or, where none existed, the most conservative values in our calculation. (For details on the data and sources used in our calculation, see the appendix.)

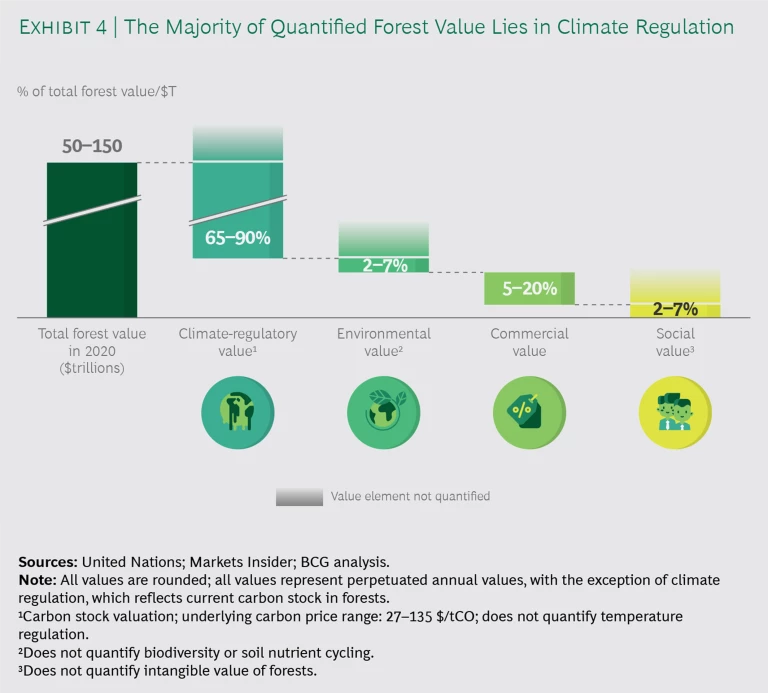

The largest share of forests’ total value—between 65% and 90%—lies in their climate-regulatory function. Commercial value accounts for the next largest share, and environmental and social value account for the remaining portion in equal amounts. (See Exhibit 4.)

Climate-Regulatory. Trees regulate the climate in two ways. First, they absorb CO2 from the air, store the resulting carbon in their biomass, and release oxygen into the air. Second, they play a significant role in regulating temperature and precipitation.

We quantified the first component by determining the amount of carbon currently stored in tree biomass. On the basis of that figure, we calculated the CO2 emissions that existing forests have prevented from being released into the atmosphere. Those prevented emissions, roughly 1,000 Gt of CO2 in total, are priced at $27 to $135 per tCO2 to arrive at the climate-regulatory value from carbon capture and storage. The lower figure represents the current 50-day moving average of the carbon price in the EU, while the higher figure is the price necessary to keep global warming below 1.5°C by 2030 according to the Intergovernmental Panel on Climate Change (IPCC).

We excluded from our calculation timber that has been removed from forests but still exists in the form of products such as building materials. Certainly, the carbon in such wood products also represents a form of carbon storage, and its impact is especially considerable when looking at the “substitution effect,” the avoided CO2 emissions from materials substituted with wood, such as cement. The European Forest Institute estimates that every ton of wood used in place of non-wood products represents 1.2 tons of avoided carbon emissions.

Although a clear methodology exists for determining the carbon capture and storage value of trees, the value created by their role in lowering temperatures and regulating precipitation is trickier to quantify. Transpiration and evaporation of water stored in forests help regulate heat flows and aid in the formation of precipitation. A loss in forested area can influence this cycle and lead to a significant reduction in local rainfall.

The capability of forests to regulate climate through carbon capture and storage is the most important factor in our value assessment, accounting for 65% to 90% of the total value of forests.

Tropical forests, heavily concentrated in South America and Africa, account for a stunning three-quarters of that value, thanks to several factors. First, they are the largest forest biome by area (58% of total forest area). Second, they hold a large share of primary forests, which have the highest carbon density. Third, they have higher tree biomass than other biomes. That translates into carbon storage per hectare of roughly 90 tons, more than double that of boreal forests.

Environmental. Forests help manage natural systems. Trees, for example, absorb harmful particles and help provide clean water by filtering it. They also help prevent or regulate natural disturbances, providing protection from soil erosion, rock falls, and high tides, for example. In coastal areas, forests such as mangroves shelter local populations from tsunamis. Forests also provide critical support of species-related and genetic diversity.

We based our environmental valuation on avoided costs, such as what it would cost to filter water through a mechanical process, the healthcare costs that would result from higher air pollution levels, and the increased disturbance-related costs that would be incurred without forests.

Calculating the value associated with biodiversity support is more challenging. Biodiversity exists on multiple levels. It is reflected in the different types of ecosystems, including forests, around the world, in the variability and abundance of species within those ecosystems, and in the diversity of genes within those species. The details of how biodiversity works within and across ecosystems are not fully understood. But we do know that forests both rely on biodiversity (to remain healthy) and provide biodiversity (by offering habitat that supports species and genetic variety). In addition, biodiversity has a direct impact on a forest’s ability to provide benefits such as disturbance regulation. Given the fundamental importance and interrelatedness of forests and biodiversity, we expect the value of biodiversity to be a multiple of our total forest value estimate. We excluded this factor from our environmental value calculation because of the difficulty in isolating its value from other benefits forests provide and the related complexity of an accurate quantification.

The environmental value of forests in our calculation is about 2% to 7% of the total. The value from air purification is the most significant, followed by that of watershed services. The latter is especially important in Asia, which accounts for more than 60% of the volume of fresh water that is withdrawn globally. The disturbance regulation value is a small part of the total, but it can be critical in such regions as Asia and Oceania, where forests reduce damage from landslides and cyclones.

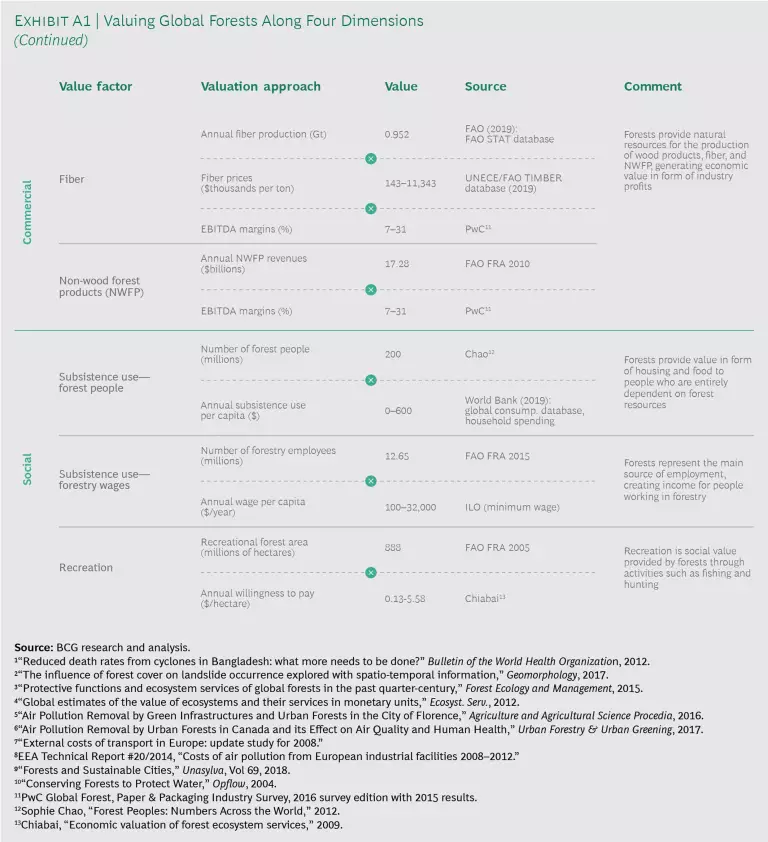

Commercial. The commercial value of forests stems from profits generated by their use in the production of certain products. These profits, distributed among players along the production chain, including forest management, harvesting, manufacturing, and retail, come largely from wood products and fiber products such as pulp and paper. Each of these product categories accounts for roughly half of our total estimated commercial value of 5% to 20% of total forest value. Non-wood forest products such as food and animal-based products (mushrooms, fruits, and honey for example), medical raw materials, and exudates (including latex and gums) are important raw materials for certain processes and products. However, they account for a very small share (1%) of forests’ commercial value.

Interestingly, Europe and Asia jointly account for almost half of forest economic value but only 20% of global forest area. That’s because they each hold a relatively high share of the world’s productive forests and have very efficient commercial forestry operations. Further, both hold a large share of temperate forest, which provides the best conditions for productive use in terms of accessibility and rate of tree growth. Forest plantations are the most productive type of forest in terms of commercial output, accounting for only 3% of total forest area but 12% of total forest commercial value.

If anything, the commercial value of forests is likely to increase. To meet the demands of a growing population while decarbonizing the global economy, humanity must increasingly rely on nature-based solutions—what is called the “circular bioeconomy.” Forest-based products are at the heart of multiple industries in the circular bioeconomy, including bioenergy, biofuels, textiles, building materials, chemicals, and packaging. And with the World Business Council for Sustainable Development projecting that the circular bioeconomy will grow to $7.7 trillion by 2030, forest-based products will be in increasing demand. In order to avoid a loss of forest value in other dimensions, such demand must be met through sustainably harvested timber.

Social. The social value of forests has several components. First, nearly 200 million people rely on forests for subsistence—they reside in and live off forest resources.

Forests certainly have significant intangible social value as well, for example the psychological and emotional benefits that the mere presence of forests provide to humanity. This value, however, is difficult to quantify accurately, and we do not include it in our valuation.

Social value constitutes 2% to 7% of total forest value, and the vast majority of that value comes from subsistence use of forests and forestry employment. Recreational value is a very small percentage.

By far the largest share of global social value comes from tropical forests in Asia and Africa, where the forest products industry is a major employer and large numbers of people also live in and rely on the forest for their livelihood. Only a small share of forestry employees and forest-dependent people are from South American countries.

Threats to Forests

Forests are disappearing at a rapid pace—we lose an area equivalent to 40,000 soccer fields every day. These heavy losses are driven by a number of threats that destroy the value of forests through deforestation, degradation, or both. (See Exhibit 5.) We studied each threat and, extrapolating from current trends, calculated the potential impact each is likely to have on forest value between now and 2050.

Our analysis yielded sobering results. On the current trajectory, one-third of forest value will be lost by 2050. The major culprits: land-use change and rising temperatures. (See Exhibit 6.) Although wildfires are responsible for 23% of annual forest loss, most of this is temporary loss. Understandably, wildfires often dominate the news, but they are likely to account for less than 1% of forest value destruction over the next thirty years. In general, tropical forests, which account for a large portion of overall value, face the greatest potential loss, with land-use change and rising temperatures the biggest threats. Temperate and boreal forests are also at risk, primarily from logging and abiotic and biotic disturbances.

The COVID-19 crisis has exacerbated forest loss. The crisis led to less aggressive law enforcement and relaxed regulations in some locations. Deforestation in the Amazon, for example, increased by 107% in the first quarter of 2020, reaching an all-time high.

Land-Use Changes

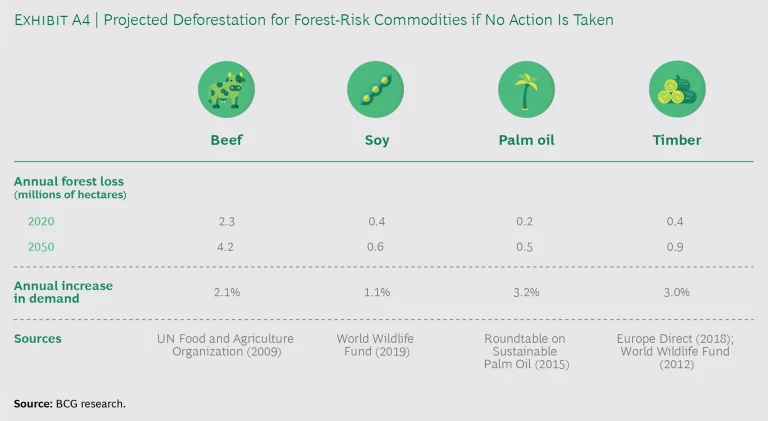

Our analysis shows that land-use changes, through the deforestation of 425 million hectares, will account for 14% of forest value loss. There are three key elements to this threat. First, and most significantly, forests are being removed so that land can be used for large-scale production of commodities, primarily through agriculture but also through mining. Second, use of the “shifting agriculture” model in small-scale subsistence farming involves clearing land for farming for a limited period. Third, urbanization in many parts of the world is leading to the destruction of significant amounts of forest to pave the way for new cities or the expansion of existing ones. In all three cases, responsible parties gain more direct benefits (in terms of money or food) from converting land than from leaving the area forested.

Large-scale agriculture is a particularly significant factor. Indeed, the top three commodities driving deforestation are palm oil, soy, and beef. Meat consumption alone, including beef, poultry, and pork, is currently responsible for more than 2 million hectares of deforestation annually. This includes the clearing of forest for use as pastureland and for soy cultivation (some 80% of soy production is used in animal feed). As the global population expands and incomes rise in the years ahead, the rate of deforestation associated with meat consumption is likely to grow significantly, if no action is taken.

At the same time, shifting agriculture, the conversion of small- or medium-scale forests and shrub land to temporary farmland, also contributes to deforestation. Under shifting agriculture, the land is farmed for a period and then left fallow, often followed by a resumption of farming or the regrowth of forest. Although this practice allows for reforestation (the planting of trees in an area that was previously forested), that can take a long time, roughly 15 years or so. In addition, in countries with fast-growing populations, such as the Democratic Republic of Congo, the pressure for agricultural output increases and fallow periods get shorter, ultimately leading to depletion of the soil and poor prospects for reforestation. The shifting agriculture model is the dominant system in tropical developing countries where the quality of soil is low and farmers have limited access to fertilizers and sustainable farming practices.

Rising Temperatures

An increase in global temperatures, and the resulting decrease in precipitation, will have a major impact on forests, accounting for about 13% of the projected decline in total value through deforestation of roughly 400 million hectares. The trend is expected to lead to widespread deforestation in the tropics as forests in those areas die and essentially become deserts. Rising temperatures will certainly have some countervailing effects. Some areas, such as those in which permafrost thaws, may become more forested. And higher CO2 concentrations in the atmosphere (a leading cause of temperature rise) may increase forest growth rates (the “fertilizer effect”). Still, the net impact on forest value will be negative.

Rising temperatures will also have indirect effects on forest value. They may reduce water and air purification and other environmental benefits of forests without necessarily leading to complete deforestation. Higher temperatures will further exacerbate other disturbances: faster growth of pest populations puts more strain on forests, and rising sea levels lead to forest death through salinization of soil. Given the difficulty in isolating and valuing the net impact of such indirect effects, we excluded them from our analysis.

Unsustainable Logging

The rising demand for forest products is expected to trigger more unsustainable logging, activity that we project will remove an amount of wood equivalent to 65 million hectares of forest. Such activity will account for 3% of the total decline in forest value.

Unsustainable logging involves the excessive harvesting of trees and leads to significant degradation (reduction in a forest’s ability to provide services such as air and water purification) and even deforestation. It is often driven by volatile timber prices (which incentivize high-volume logging when prices are high), unclear ownership rights (which contributes to illegal logging), a lack of long-term management plans from public- or private-sector forest owners, or subsistence use of wood by economically disadvantaged populations.

Abiotic Disturbances

Abiotic, or nonbiological, events such as extreme storms or wildfires are projected to account for roughly 1% of forest value loss through the degradation of an additional 35 million hectares. Although wildfires have devastating effects on local populations, they are generally natural events in forest ecosystems, returning nutrients to the soil from decaying plants and allowing growth of native species. And contrary to the impression left by much of the media coverage, historical data from 1998-2015 reveals that the area burned each year actually decreased over that 17-year period.

Going forward, however, a majority of studies predict an overall increase in burned area and/or fire intensity due to a warmer and drier climate. And as recent events in Australia have proven, such a development would pose a significant threat to biodiversity. Still, given the uncertainty and complexity of climate models, and the fact that rising temperatures could increase precipitation and therefore reduce wildfires in tropical areas, the ultimate trajectory of global wildfires is difficult to predict.

Biotic Disturbances

Although threats from pests, diseases, and invasive species are on the rise around the world, they are expected to account for only roughly 1% of the value deterioration between now and 2050, through the degradation of an additional 20 million hectares. The relative importance of this threat is highly dependent on the region, of course. For instance, in the past two decades, reduced tree diversity and rising temperatures have fueled the expansion of pine and spruce beetle outbreaks across North America, Europe, and Siberia, causing millions of dollars of damage to the timber industry in these regions. Although climate change will have a major impact on the extent and intensity of biotic disturbances well beyond 2050, it is difficult to forecast those effects today.

Actions to Save Global Forests

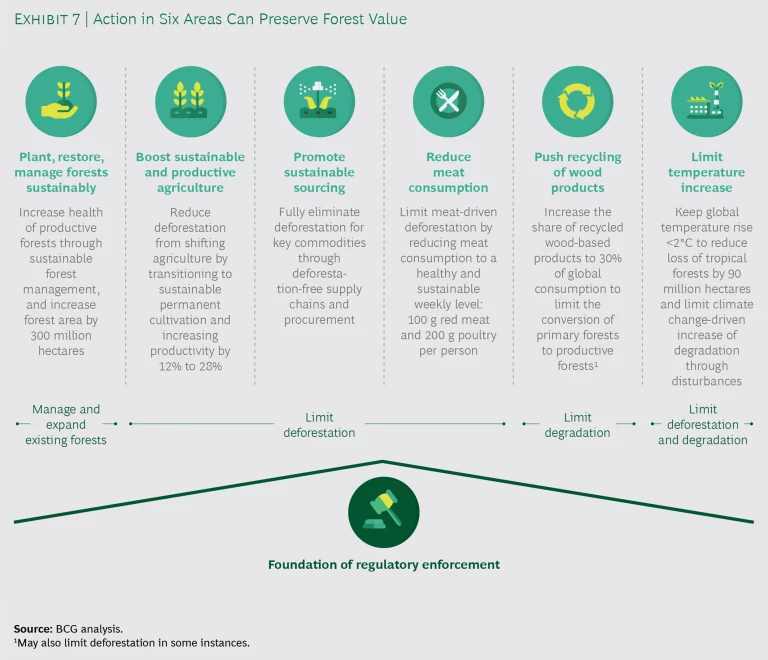

The current range of threats to forests around the world requires aggressive and immediate action by all stakeholders. Concrete actions can be taken today to address these threats. We zeroed in on actions in six areas that can have significant impact. These actions take aim at the threats outlined above, either directly (by restoring forest area, for example) or indirectly, by reducing the drivers of deforestation. (See Exhibit 7.)

As detailed below, we have based our projections on ambitious but feasible assumptions. Those assumptions largely reflect existing commitments and goals as outlined by players in the global community. Under this scenario, forest value loss can be reduced from roughly 30% to 10%. That equates to the preservation of $30 trillion in value—an amount roughly six times the combined value of Apple, Microsoft, Amazon, Alphabet, and Facebook. (See Exhibit 8.) Given that the overall value does not include components such as biodiversity, it is likely the value preserved through these measures could be even higher.

We focused our recommendations on four key stakeholder groups: governments, both those in countries with significant forest areas and those in countries with less forested acreage but a commitment to preservation of global forests; NGOs, including both international and local organizations; the private sector; and consumers from all socioeconomic backgrounds. Action by governments and the private sector—including investors—is particularly vital. (See “The Role of Investors.”)

The Role of Investors

The Role of Investors

Large investors are increasingly making capital allocation decisions to both mitigate environmental and societal risk in their portfolios and advance critical societal goals. They are motivated by mounting evidence that companies with strong environmental, social, and governance performance can also outperform financially. When it comes to the protection of the world’s forests, they are making an impact in two main ways.

First, some leading investors are encouraging companies to commit to sustainable, deforestation-free supply chains and are steering their investments toward those public companies that do. In the fall of 2019, investors with a total of $16.2 trillion of assets under management signed an open letter urging companies to prevent deforestation. Such action could have significant impact. According to CPG, a nonprofit that runs the global environmental disclosure system, more than $940 billion of public company revenue is dependent on forest-risk commodities.

Second, investors are putting some funds directly to work in sustainable forestry funds. These funds generate revenue based on sustainable timber proceeds or other forest products, sale of carbon offsets, or leasing or sales of land for conservation.

Investors can be catalysts for even more progress in the years ahead. Sustainable forestry funds, for example, are a relatively small asset category despite their attractiveness. Policymakers should build a regulatory environment that incentivizes (or requires) investors to take sustainability into account and promotes further development of the market. This can include the development of a robust market for forest-backed securities and open-ended sustainable forestry funds that provide more liquidity than their closed counterparts. Governments and NGOs can also ensure improved access to information on sustainable forestry investment opportunities for investors, reducing the need for a resource-intensive, detailed due diligence and the level of perceived risk in a currently complex investment landscape. At the same time, large investors need to continue to push the public companies in their portfolio to take aggressive action on deforestation. Such action can make institutional investors a potent force for forest preservation.

Even if we take ambitious action in all of the areas described here, our model shows a value loss of 10%. Preserving, or even bolstering, the total value of forests today would require more aggressive action: we would need to not only start managing all existing productive and mixed-use forests (an area of more than 2.7 billion hectares) sustainably but also afforest and reestablish forests on about 900 million hectares—all the land, including private holdings, available for such activities today.

Restore and Plant Forests and Manage Existing Forests Sustainably

The largest impact of our six areas for action comes from driving sustainable management of forests through large-scale restoration and afforestation (the planting of trees in an area that was not previously forested) and the establishment of the right incentives and regulations to promote sustainable practices in existing forests. In total, these efforts can reverse about one-third of value loss, preserving 13% of current forest value.

This estimate has two components. Three-quarters of the projected impact comes from aggressive efforts to plant or restore about 300 million hectares of forest. The 300 million hectares figure is based on current commitments made by governments, associations, and companies, including the Bonn Challenge, an initiative launched by the German government and the International Union for the Conservation of Nature.

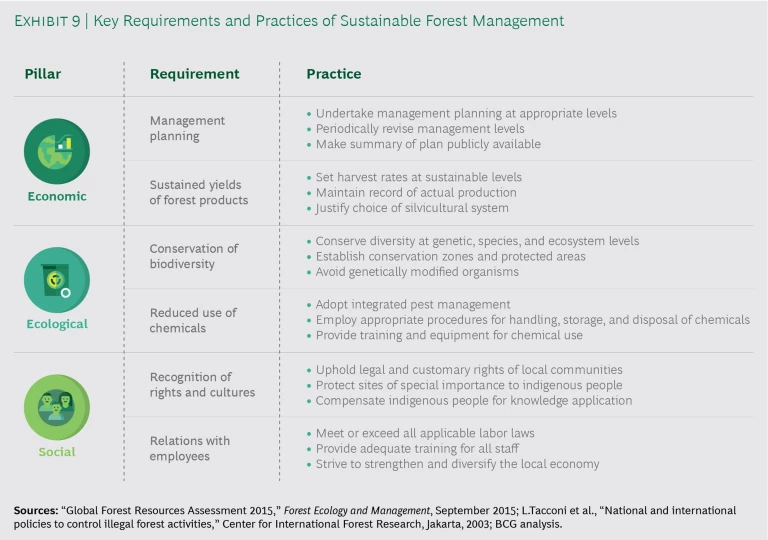

The other quarter of the expected impact comes from sustainable management of existing commercially used forests. Right now about 40% of all forested area is managed sustainably. Our calculation assumes that by 2050 all countries that have committed to the Bonn Challenge will employ sustainable practices in 100% of their existing commercially used forests. That increase equates to roughly 200 million hectares. Sustainable forest management practices in commercially used forests aim to ensure forests hold a large amount of wood and are diverse, both in terms of abundance and variability of species and genes and the age of trees. Such diversity in forests increases their resilience to disturbances and their ability to provide benefits such as carbon capture and storage. Further, such productive forests help to sustainably meet the increasing demand for wood as a substitute for other high-emission materials (See Exhibit 9.)

Governments. Policymakers must move on two fronts, pushing large-scale restoration and afforestation initiatives and establishing a comprehensive system, including support of the market for wood-based products, that incentivizes, or indeed requires, the private sector to manage the forests they own sustainably.

To drive large-scale restoration and afforestation initiatives, governments need to leverage both public- and private-sector resources. They should integrate such initiatives into budget planning at national and subnational levels through tools such as “ecological fiscal transfers,” which allocate tax revenues to forest owners based on the maintenance and expansion of forest areas. At the same time, they should find ways to fund restoration and afforestation initiatives through blended finance, an approach that uses public resources (in the form of insurance, for example) to attract private investment. The Land Degradation Neutrality Fund, for instance, is an investment vehicle that raises public, private, and philanthropic capital for land restoration projects implemented by the private sector. The fund lowers private investment risk through public money from “de-risking partners,” such as the government of Luxembourg, who cover more risky measures and give priority in the payment of returns to private investors.

All publicly funded restoration and afforestation efforts must be combined with incentives and rigorous outcome-based monitoring to ensure that these forest areas are managed sustainably and thus preserved in the long term. Consider Turkey’s ambitious initiative in 2019 that involved the planting of more than 300,000 saplings in a single location in one hour. Nearly 90% of those trees died within a few months, most likely owing to poor timing of the planting and the selection of a location with insufficient precipitation.

Governments must create a system that supports the development of sustainable and productive commercial forestry operations.

Large-scale restoration and afforestation projects, however, will not be enough. Governments must also create a system that supports the development of sustainable and increasingly productive commercial forestry operations. A robust commercial forestry sector can drive increased investment in restoration and afforestation, spur innovation and efficiency in managing healthy and productive forests, and establish incentives to protect them at a local level.

This should start with steps to advance the development of the wood-based products market. Governments can do this through multiple actions, including the promotion of long-term uses of wood, such as in construction, and requiring a certain share of wood-based materials in public procurement. In addition, governments in regions where access to commercial forests is limited may need to invest in infrastructure such as road construction and maintenance. Ultimately, action to support steady demand for wood products will help to stabilize timber prices and reduce the tendency of commercial operators to overharvest.

Such a benefit, however, will depend on the degree to which wood-based products come from sustainably managed forests. After all, unsustainable logging will drive degradation or ultimately even deforestation, regardless of how the end product is used.

That’s why governments need to marry their support of the wood-based products market with policies that drive an expansion of sustainable forestry. They should establish policy and regulatory frameworks that include clear standards for sustainable forestry and trade regulations that favor sustainably harvested wood. They must also clarify and secure land ownership rights—without which commercial operators will not make the investments required to operate sustainably. Governments must ensure that their regulatory approach is consistent; unpredictable changes make it difficult for commercial operators to plan for the long term. And they should avoid excessive bureaucracy and such interventions as subsidies for wood-based bioenergy, which distort market prices.

At the same time, governments can look for new, innovative ways to support sustainable forestry. They can, for example, establish schemes such as ecosystem service payments, which provide remuneration to forest owners who use sustainable practices for the public benefits their forests provide. These payments can in some cases be funded by revenues generated by taxes on CO2 emissions. In Germany, one state is exploring a program under which the government would redirect tax revenues to private forest owners based on the value of the ecological benefits that those forests provide.

NGOs. Nongovernmental organizations should continue to research and share their expertise with other stakeholders to maximize the impact of restoration and afforestation initiatives. For example, they can work with the private sector to identify and develop technology-based solutions for sustainable forest management or identify and help scale new funding mechanisms. In countries where there is no public body equipped to drive restoration and afforestation projects, nongovernmental organizations should also help design and monitor such efforts. They can, for example, facilitate landscape planning initiatives, projects where NGOs and public and private actors come up with a comprehensive land use plan based on social, commercial, and environmental goals. Further, NGOs should encourage and facilitate donations for afforestation projects through initiatives such as the Trillion Tree Campaign, a program that links donors with forest conservation ventures around the world.

Private Sector. As governments create the right incentive structure, companies and investors should embrace sustainable forest management and productivity-boosting measures in their commercial forestry operations. Such practices will enhance revenues and lower risks by reducing forests’ susceptibility to disturbances, lowering costs for protecting and planting through natural regeneration, and promoting continuous and improved timber yields. Plantations in particular must be managed in a way that creates more diversity in tree types and that adjusts the composition of tree species (what is known as “assisted migration”) toward the varieties that are most likely to thrive as temperatures rise and, potentially, those that also maximize CO2 capture.

Forestry companies can increase the productivity of their sustainably managed forests by adopting solutions such as genetic improvement, plant breeding, and precision forestry. However, the development and application of technology-based solutions in forestry (laser scanning to track forest inventory, for example) lags behind that in comparable sectors such as agriculture. Startups and established forestry players should push to develop tools and gain an early mover advantage.

In addition, commercial forestry players can acquire and cultivate trees on land that was previously used for other purposes, including marginally productive farmland or land that was previously covered by permafrost but is now suitable for planting thanks to rising temperatures. The latter category is likely to involve as much as 150 million hectares by 2050.

Companies can also lead or support afforestation initiatives as a way to accelerate their progress in becoming carbon neutral, an effort that may be driven by legal requirements, the demands of investors or consumers, or voluntary commitments. This is particularly true for industries such as airlines and petrochemicals, where the environmental pressure is highest and where decarbonizing operations with currently available technology is still challenging.

Boost Sustainable and Productive Agriculture

A movement toward permanent, sustainable agricultural cultivation, and away from shifting cultivation, and the adoption of more productive farming practices reduce the need for farmers to clear forested land for agriculture. We believe aggressive moves in both areas can reduce deforestation by up to 100 million hectares by 2050, preserving roughly 3% of today’s forest value.

Transforming agricultural practices, however, is not a matter of simply giving farmers information on more productive, permanent cultivation techniques. Shifting agriculture today is deeply rooted in the traditions and heritage of many developing countries. There are very tangible obstacles to encouraging permanent cultivation, including poor soil quality, a lack of infrastructure and market access, inadequate credit availability, and lack of clarity around property rights.

Governments. In order to enable a movement away from shifting agriculture, governments in countries where the practice is prevalent must create conditions under which farmers, especially smallholders, can take such action without risking their subsistence.

The public sector should promote long-term investments in agriculture by clarifying property rights. Further, they should provide independent training and technical assistance to help farmers be more successful over the long term by limiting their dependence on agriculture-related companies.

Governments should also provide direct financial support for farmers. They can, for example, provide funding assistance for investments in agricultural input, such as fertilizers, and establish a financial safety net for farmers against crop failures. At the same time, governments should require that farmers who receive financial support adopt sustainable farming practices that will limit environmental degradation. This includes agroforestry, a popular approach in the tropics that involves integrating trees and shrubs into farmland as a way to preserve biodiversity. Further, governments should ensure that the regional market infrastructure is adequate to handle increased agricultural output from both productivity improvements and the shift toward permanent agriculture.

Governments should also address the potential negative ripple effect of increased agricultural productivity. As productivity improves, returns on a hectare of land increase—making the opportunity costs to farmers for preserving forested acreage even more steep. Therefore, governments should include farmers in their discussion of afforestation and restoration initiatives and possible financial compensation mechanisms for those preserving forests on their land.

And governments should track their overall progress in promoting permanent agriculture, employing satellite-based and other data to develop sophisticated monitoring systems.

NGOs. Nongovernmental organizations can run design courses and workshops on permanent cultivation, as well as community-based projects focused on watershed and soil management, tree-based farming, diversified cropping, animal integration, and seed saving. Such programs will also reduce food loss by minimizing the need for farmers to harvest crops prematurely in order to address a cash flow crunch.

In addition, NGOs can shape the dialogue around deforestation in a way that encourages collaboration by farmers, governments, and conservationists. Often, public communication by NGOs, intended to raise awareness on the causes of deforestation, seems to reflect the perspective of developed countries and does not account for some of the complexities in developing countries, including the expanding need for arable land. Such messaging often triggers a blame game rather than the constructive development of common solutions.

Private Sector. Companies and investors should support farmers in order to accelerate the move away from the shifting agriculture model to permanent cultivation systems. Food companies, for example, can expand their network of smallholder farmers. Such efforts can have dual benefits, helping to improve the productivity and sustainability of those farm operations while making the supply chain more resilient .

In addition to supporting the move toward permanent agriculture, technology-based companies can improve agricultural productivity by developing tools that expand the time periods when crops can be grown. These tools include precision watering, analytics-optimized LED lighting, and hydroponics (growing plants in a nutrient-rich solution rather than soil). They can also invest in technologies, such as saltwater-cooled greenhouses, that have the potential to turn unproductive areas such as deserts into arable land.

Promote Sustainable Sourcing

Right now, more than 3 million hectares of forest are lost every year for the production of just four commodities: soy, palm oil, beef, and timber (a significant share of which is used for fuelwood). We estimate that 75 million hectares of deforestation driven by these “forest-risk” commodities can be avoided by 2050, preserving roughly 2% of current forest value. That projection assumes that the production of these commodities becomes deforestation-free by 2050. This estimate may prove to be conservative, given that many organizations, including companies, NGOs, and governments, are advocating for these commodities to be deforestation-free by 2030. While there is a role for all stakeholders, the poor transparency within forest-risk supply chains makes it difficult for consumers to have an impact. The responsibility for sustainable sourcing lies most prominently with governments and the private sector.

Governments. Governments must create a regulatory environment that enables, promotes, and forces change in the private sector. Extensive analysis of 500 companies that play major roles in the forest-risk commodities supply chain shows that only a fraction have been able to make their supply chains deforestation-free over the past decade. Voluntary commitments alone have proven insufficient: Despite growth in the number of deforestation commitments of 63% from 2014 through 2018, average annual forest loss has increased by 44% over the same period. That’s why legally binding regulation is critically necessary to level the playing field among all players in the supply chain for forest-risk commodities and penalize and incentivize change on the ground.

There are two levels of regulations that support sustainable sourcing—those aimed at domestic production and those related to imports. A significant share of beef, for example, is consumed in the country where it is produced—making domestic regulations critical. At the same time, roughly 25% to 30% of products produced in deforested areas are sold to international markets, underscoring the importance of import regulations.

There are clear signs of momentum on both domestic production and import-related deforestation policy. The EU Forest Law Enforcement, Governance and Trade (FLEGT) Action Plan, for example, is designed to encourage sustainable practices and sourcing among both suppliers and buyers of forest-risk commodities. In 2018, France introduced a National Strategy Against Imported Deforestation to end the importation of nondurable forest or agricultural products that contribute to deforestation by 2030. In 2019, the UK government established an independent taskforce, the Global Resource Initiative (GRI), to develop recommendations to reduce deforestation and degradation related to agricultural and forestry products. Having concluded its assessment, the GRI has recommended a legally binding target to make UK supply chains deforestation-free as soon as possible—but no later than 2030. As part of that target, businesses and financial institutions will be required to conduct due diligence to ensure they are not supporting practices or companies that contribute to deforestation.

Governments must also ensure that both domestic and trade regulations are designed to minimize unintended consequences—spillover effects that can arise in a number of ways. First, developed countries that put strict regulations on domestic producers, without similar rules on imports, can end up having little net impact on deforestation because they essentially transfer unsustainable practices from their shores to countries that do not have strict rules on deforestation (often those in the developing world). Furthermore, the new location may have less efficient production and require more land to generate the same output—worsening the deforestation problem. Second, pressure to eliminate deforestation impact in one product can shift the problem to other product types. For example, increased demand for deforestation-free soy may result in soy production expanding to land that was previously used for cattle grazing—with cattle farmers then expanding into forested areas. Such displacement effects are possible in many product areas. The World Wildlife Fund (WWF) calculated that if all the palm oil currently consumed in Germany was replaced with other vegetable oils, it would require five times as much cropland.

In the case of timber, governments can lead by example—for instance by establishing policies to ensure that wood sourced for public construction projects has zero deforestation impact. While some governments, including those in Norway and the state of California, have already made general deforestation-free commitments, those efforts must be paired with a robust implementation plan and effective monitoring.

NGOs. Nongovernmental organizations such as the Forest Stewardship Council (FSC) play a vital role in establishing standards related to sustainable sourcing and operator certification. (See “The Impact of Certification.”)

The Impact of Certification

The Impact of Certification

Certification can be a powerful lever for promoting sustainable supply chains. For example, certifications from the Forest Stewardship Council (FSC), a leading worldwide organization with more than a thousand members (including NGOs such as the WWF), cover approximately 200 million hectares of forest in 82 countries. The organization provides standards for the socially, ecologically, and economically responsible production of wood and transparency on wood producers’ compliance with these standards for corporate and private buyers of wood products. FSC standards are designed to closely mirror the EU Timber Regulation in order to streamline the risk assessments and risk mitigation activities done by timber-trading companies and the due diligence conducted by EU regulators.

The Swedish multinational food packaging company Tetra Pak, for example, has used FSC certifications as a strategic key performance indicator. Because of this, by mid-2019, the company had delivered more than 500 billion FSC-labeled packages, having sourced 100% of paperboard from FSC-certified or FSC-controlled sources since 2018—all part of its drive to ensure deforestation-free production and reduce its carbon footprint.

NGOs must continuously adapt these certifications on the basis of market developments and monitor compliance closely in order to ensure that the standards are effectively reducing deforestation. They should also assess and test the regulations and commitments of public and private actors and raise consumer awareness of the importance of buying deforestation-free products. NGOs should also find ways to support those operators who are committed to zero deforestation—otherwise, significant restrictions in operations will discourage companies from certifying their operations and adhering to standards.

Private Sector. Many companies and investors have made voluntary zero-deforestation commitments. In 2014, for example, 57 multinational companies endorsed the New York Declaration on Forests, aiming to eliminate deforestation from their supply chains. And a 2006 moratorium on soy production on deforested land in the Amazon, signed by 85 producers, distributors, buyers, and NGOs, has slashed soy-related deforestation there from 30% to approximately 1.5%.

To meet these commitments, however, companies must fully integrate sustainable sourcing into their operations.

First, companies that buy forest-related products need to demand commitments from suppliers to adopt sustainable sourcing practices—and aggressively monitor those commitments. This includes establishing a grievance mechanism for suppliers that fail to live up to standards, and a transparent process for supplier selection. In addition, there needs to be increased transparency on progress, which is significantly lacking today.

Second, they need to ensure that their risk management assessments factor in the degree to which their operations contribute to deforestation. According to a CDP study of 306 companies that purchase high-forest-impact commodities (beef, soy, palm oil, and timber) 29% of those companies did not include forest-related issues in their risk assessment. This gap exists despite the fact that almost all companies that do factor those issues into assessments identified significant forest-related risks.

Investors, meanwhile, need to become more vocal and demand sustainable production and sourcing from companies in which they have holdings. And they should join efforts such as Climate Action 100+, an investor initiative to engage companies with the highest emissions in the fight against climate change.

Consumers. Wherever possible, individuals should purchase beef, soy, and palm oil that is certified to be deforestation-free and timber certified to be from sustainably managed forests. However, given the complex nature of forest-risk commodity supply chains and a lack of transparency on unintended consequences, they face significant challenges in using their purchasing power to drive change. For one thing, certifications for palm oil, soy, and beef are visible when they are bought as commodities—but less so when they are used as ingredients in other food products. In addition, it can be difficult for consumers to know if, by avoiding certain products, they are inadvertently driving mere displacement of deforestation or supporting product substitutions that only drive more deforestation. For example, boycotting entire commodities, notably palm oil, can actually worsen deforestation because oil substitutes require significantly more land.

Ultimately, consumers can have the greatest impact by using their voices to advocate for regulatory and private sector change, increasing their impact beyond what’s possible with their individual consumption choices.

Reduce Meat Consumption

Although sustainable sourcing is important, it is also imperative to limit the consumption of one forest-risk commodity in particular: meat.

Globally, meat production has increased nearly fourfold in the past 50 years, contributing to deforestation through soy production for animal feed and, in the case of beef, the expansion of pastureland.

Governments. In order to change consumption patterns, governments must pull a number of levers. They can shift tax policy to incentivize a plant-based diet and discourage meat consumption. Such changes, however, must be managed carefully and take into consideration social issues such as the impact on cattle farmers resulting from a change in demand and prices. They can also adjust nationally recommended diets to change behavior. Currently, these diet recommendations make almost no reference to environmental impacts such as deforestation.

NGOs. Nongovernmental organizations can help raise public awareness about the negative impact of meat consumption and support similar consumer campaigns by governments and corporations. In particular they can inform consumers about the link between meat consumption and deforestation, as well as the health benefits of relying less on meat as a protein source. A study by Dutch researchers found that educating consumers about the climate change benefits of reduced meat consumption led those consumers to shift toward a plant-based diet.

Private Sector. Companies can play a large role in helping consumers select more environmentally friendly foods. Food companies should commercialize and promote plant-based products to incentivize a shift from meat-based consumption. Investors should look for opportunities to put their money behind companies developing and sustainably producing meat substitute products, a number of which have been huge consumer hits. Additionally, retail companies should offer consumers practical advice on adapting a more environmentally friendly diet.

Consumers. Consumers can directly decrease beef- and soy-related deforestation by reducing their meat consumption. The average person in the world consumes more than 800 grams of meat per week. Especially in developed nations, meat consumption per capita is far above the recommended level for healthy nutrition, proving that a reduction in meat would be advantageous from both environmental and health perspectives.

Push Recycling of Wood-Based Products

As wood demand increases in the future, wood recycling will drive greater efficiency in how previously harvested wood is used, potentially extending its lifecycle and therefore the length of time it can store carbon. At the same time, increased recycling would reduce the need to harvest fresh wood.

Today, recycled wood material (excluding wood used for energy production) on average accounts for an estimated 10% of the wood consumed globally every year. If that portion is pushed to 30%, it would reduce the amount of timber that needs to be produced from forests by 1.5 billion tons by 2050, preserving roughly 2% in current forest value.

Recycling involves converting waste wood, which comes from sources such as construction and demolition sites and wood processing factories, into something of equal or greater value (upcycling) or something of less value (downcycling or cascading). The hierarchy of cascading goes from solid wood or veneer products down to chemical raw materials and finally energy use. Currently, the main uses of recycled waste wood are as material for energy use or panel boards.

Governments. Public sector leaders should implement regulations and policies that bolster both the supply of and the demand for waste wood and establish the prerequisites for broad-based wood recycling.

First, they must ensure an efficient and effective infrastructure to collect, classify (according to attributes such as level of hazardous materials, treatment, and quality level), separate, prepare, and recycle waste.

Second, they need to ensure that the right regulations and incentives are in place for groups that buy and supply wood for recycling. The incentive structure should be aligned with policies in bioenergy, circular bioeconomy, waste management, forestry, and public procurement. Take incentive structures in bioenergy as an example. In regions where primary wood sources are in cheap supply or where the majority of fresh wood can go into subsidized production of bioenergy, there may be little economic incentive for the establishment of an infrastructure for wood recycling. The EU renewable energy directive, for instance, subsidizes the use of wood as biomass for energy.

NGOs. NGOs can help to provide transparency for consumers and awareness on the importance of using waste wood for a wide range of applications and of refraining from burning fresh wood as bioenergy. This can include promoting the widespread use of labels for recycled wood. Compared with certification for sustainable fresh wood, labels for recycled wood are not well established, limiting consumers’ ability to deliberately purchase recycled wood products. For instance, the recycled label of the biggest forest management certifiers, FSC and PEFC, is still little known or used compared with regular sustainable wood certificates. In addition, NGOs should inform consumers on how wood should be disposed so that it is available for recycling.

Private Sector. Companies in a wide range of industries, including cosmetics and skin care, can integrate recycled wood-based products into their operations, in many cases replacing fossil-based plastics. Such players should develop and refine business cases for commercializing recovered wood and fiber (leveraging the expected increased government incentives for such actions). This includes breaking with firmly established practices and getting more creative about how different wood types are used. The panel industry has set a positive example by significantly increasing the amount of waste wood used in its boards through new technologies. But if other scalable and sustainable uses are found for beech, forest owners would shift some of their material to those options.

Companies should also integrate circular design principles into their processes, policies, and employee training. These principles facilitate the recycling process throughout a product life cycle, by selecting, for example, materials that are well suited to automatic separation. In addition, they should take the lead in addressing gaps in the current infrastructure, including through the adoption of technologies for tracing wood or mechanisms for connecting waste wood recyclers with suppliers.

Consumers. People should look for opportunities to buy used wood products or products that are made with recycled wood. Further, they should carefully follow local rules about waste separation, so that more post-consumer wood is directed to recycling.

Limit Global Temperature Increase to Less Than 2°C

Efforts to limit climate change will have a significant impact on forest value. According to our model, limiting the global temperature increase to less than 2°C, in line with the Paris Climate Accord (versus the current trajectory toward a 4°C or 5°C increase by the end of the century) would prevent the loss of roughly 3% of forest value.

Given the magnitude of the challenge , this action area is in many ways distinct from the other five. Research by many organizations, including BCG, has underscored The Economic Case for Combating Climate Change . Any successful campaign to limit the devastating consequences of climate change must include a reduction in deforestation and degradation—a reflection of the deep and complex connection between trees and climate. (See “The Interdependence of Trees and Climate Change.”)

The Interdependence of Trees and Climate Change

The Interdependence of Trees and Climate Change

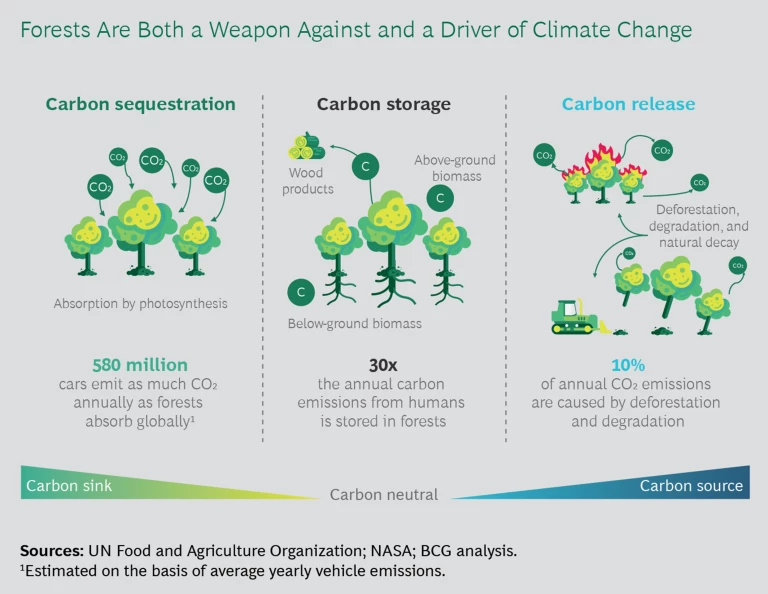

Forests are both a casualty of climate change and one of the most potent weapons in the fight against it. At the same time, our current destruction of the world’s forests is an accelerant of global temperature rise.

Through photosynthesis, forests have accumulated immense amounts of carbon, the majority of it held in their biomass and soil. If trees die and their biomass decays, some carbon remains in the soil, while the rest is released back into the air. As a result of this cycle, forests have three roles in determining CO2 levels in the atmosphere (See the exhibit “Forests Are Both a Weapon Against and a Driver of Climate Change”):

- If the biomass of a forest is growing, the forest becomes a net carbon sink (absorbing more carbon than it emits).

- When forest area or biomass remains stable, the forest is carbon neutral (absorbing as much CO2 as it releases).

- When more biomass is lost than regrown (as in a degraded forest), the forest is a net CO2 emitter (releasing more CO2 than it absorbs).

Wood products with an extended life cycle are often seen as additional carbon sinks, outside of forests, because they retain carbon and can reduce emissions via the substitution effect. For example, if 50% of new buildings were constructed with timber by 2050, emissions from the production of steel and cement would decrease at least by half.24

Human activity has altered the balance among the three roles forests play in regulating CO2 emissions. Today, for forests in aggregate, annual emissions from biomass loss due to deforestation and degradation vastly exceed the amount of carbon absorbed. In other words, forests have become a net emitter of CO2.

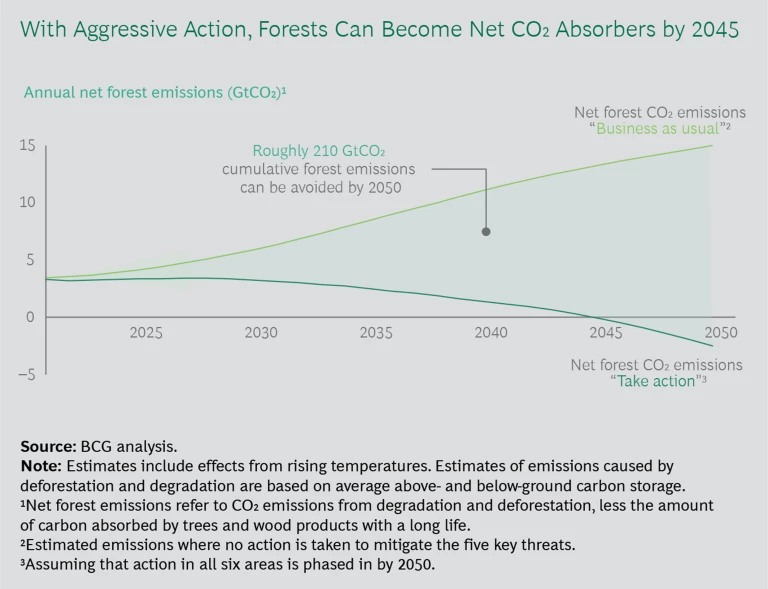

Our modeling shows that forest emissions could swing between two extremes between now and 2050, depending on the measures we take.25 (See the exhibit “With Aggressive Action, Forests Can Become Net CO2 Absorbers by 2045.”)

- If we do not take action in the six areas outlined in this report, forest emissions are projected to rise to 15 GtCO2 per year. This is more than the annual emissions from China today.

- If we take aggressive action in the six areas and succeed in limiting global temperature increase to less than 2°C, forests can become net absorbers of CO2 after 2045 and capture up to 2 GtCO2 per year. This amount is more than the annual CO2 emissions from Russia today.

Which path we ultimately travel will help determine the health and sustainability of the planet for generations to come.

24. “Buildings can become a global CO2 sink if made out of wood instead of cement and steel,” ScienceDaily, January 2020.

25. Both scenarios include emissions from forest loss through rising temperatures—an aspect that many projections of forest-related emissions do not factor in.

The Right Foundation

Actions by all stakeholders will have less impact if a foundation of aggressive enforcement of forest-related regulations is not firmly established.

Enforcement is particularly important in stopping illegal logging, which today accounts for up to one-third of global timber production, according to Interpol. Governments should push to enforce laws against illegal logging, both on their own and in collaboration with the private sector and other countries. New technologies, such as early warning systems to detect illegal logging, can be powerful tools in that fight. (See “Stopping Illegal Logging in Its Tracks.”)

Stopping Illegal Logging in Its Tracks

Stopping Illegal Logging in Its Tracks

The key to combating illegal logging is to stop the practice before the damage is done. Unfortunately, most systems for spotting deforestation today use satellite-based monitoring to detect ongoing deforestation—which means the warnings from such systems can come too late.

WWF has taken aim at this problem. Together with BCG, it developed Early Warning System (EWS) to predict and prevent illegal deforestation. EWS predicts which areas are likely to suffer deforestation within the next six months. The predictions are based on factors such as proximity to forest degradation and existing roads, the level of industrial activity and shifting agriculture, the population density, and the extent to which sustainable forestry is practiced. An underlying machine learning model combines topological data with socioeconomic information and data retrieved from state-of-the-art radar satellite technology to create alerts for those areas at risk for deforestation.

The system allows governments, communities, and the private sector to spot early signals of imminent illegal logging and take action to prevent it. EWS is currently being piloted in Central Kalimantan on Borneo and aims to go live for all of Borneo in 2020, with the ultimate objective of reducing the illegal conversion of forests in Borneo by 10% to 35%. Owing to the initial successes in Central Kalimantan, WWF plans to scale the program to other deforestation fronts around the world, starting in the Guianas and the Congo region.

WWF is implementing the EWS with governments and local communities. The system is being developed in collaboration with BCG and a tech consortium that is led by Deloitte and includes Amazon Web Services, Jheronimus Academy of Data Science, and Utrecht University.

A Call to Action

The world’s forests represent an asset of staggering value. With the bulk of that value manifested in trees’ ability to capture and store carbon, the battle to stave off the most devastating effects of climate change will hinge on mankind’s ability to protect this vital resource.

But the asset is being destroyed. And the key threats to forests—land-use change and rising temperatures—are manmade. Consequently, it is up to all of us to halt the devastating decline in global forest value and to take decisive action now. Governments, NGOs, the private sector, and consumers all have an important role to play. Their actions will determine whether forests continue to be degraded and lost or protected and restored. Ultimately, allowing the destruction to continue will make forests an accelerant of climate change—preserving them will combat it.

Our analysis should serve as a rallying cry to all stakeholders. Further delay means the loss of more forested land. We must act as if the future of the planet depends on it—it does.

Acknowledgments

The authors thank Adrien Portafaix, Florent Rodzko, Belinda Saunders, the Forest Stewardship Council, and Naturschutzbund Deutschland for their assistance in developing this report. They also acknowledge Amy Barrett for writing assistance and Katherine Andrews, Kim Friedman, Abby Garland, Adam Giordano, Frank Müller-Pierstorff, Shannon Nardi, and Ron Welter for their contributions to editing, design, and production.

APPENDIX: ASSUMPTIONS AND METHODOLOGY

APPENDIX: ASSUMPTIONS AND METHODOLOGY

The relative biome distribution in each country, also based on FAO data, is assumed to remain constant over time.1 Subtropical forests are included in the “tropical forests” biome category. We categorize forests from a human use perspective in two ways: commercially used forests (plantations and commercially used natural forests) and noncommercially used forests (primary and mixed-use forests). The total amount of mixed-use forests is calculated as the difference between total forest area and the sum of commercial and primary forest area.

Currency conversions for forest valuation, threats, and action impact are based on the annual average exchange rate in 2018. 2

Note 1: "Global Forest Resources Assessment 2000," Food and Agriculture Organization (FAO) of the United Nations.

Note 2: Applied rates: US$1 = EUR 0.85, INR 68.85, CHF 0.99, PHP 52.87.

Methodology for Valuing Forests

We compute the value of the four dimensions of forest value on the basis of individual components. (See Exhibit A1.) The values of the various components are computed in perpetuity—a recurring annual value without a determined end, discounted to its value today—with one exception. Carbon storage value is not calculated as a recurring value; it is based on the amount of carbon held in forests currently. Most other assessments of forest value have analyzed the annual value of forests—not their full present value into the future. Our approach reflects the fact that forests are a self-sustaining asset that will provide benefits indefinitely if they maintain their current total area and health.

The resulting total computed value provides the basis for assessment of threats and action areas.

A note on exclusions from quantification. When assessing the value from carbon storage, we exclude carbon stored in soil, considering only carbon stored in above- and below-ground biomass of trees. Soil can capture significant amounts of carbon, and it currently holds roughly 40% of the total carbon stock of forests. However, the ability of soil to store carbon is not specific to forests; thus, to capture the portion of carbon in the soil that is related specifically to forests would require comparison of soil levels in forests with carbon levels in nonforested areas. However, that calculation depends on the type of land chosen as the reference point. Soil in agricultural lands, for instance, can be a powerful carbon sink when managed correctly. Given the wide variability in reference points, we do not include forest soil in our climate regulatory value.

Further, we do not quantify the benefit forests provide in three areas: regulation of temperature and precipitation, enhancement of biodiversity, and intangible benefits.

The final area is particularly challenging. It includes the educational, spiritual, and cultural value of forests—what some people describe as a benefit from simply knowing forests exist. In academic literature these intangible benefits are often categorized as the “passive use” value of forests, approximated according to how much people say they are willing to pay for the existence of forests without immediate use. For two reasons, passive-use value is not included in our calculation. First, people may include the value they see in forests for climate regulation, air purification, and the like—factors we capture through other measures—into that passive-use value. Second, such measurements are highly subjective and therefore imprecise.

Note 3: Maureen L. Cropper, “How Should Benefits and Costs Be Discounted in an Intergenerational Context?” discussion paper, Resources for the Future, 2012; "The Green Book: Central Government Guidance on Appraisal and Evaluation," UK government publication, 2018.

Quantification of the Impact of Forest Threats

We calculate the potential impact of each threat on the basis of a detailed literature review and extrapolation of current trends. (See Exhibit A2). The baseline for our threats analysis is today’s forest value. As a result, areas that are already degraded are reflected in our current forest value calculation and are not incorporated into the projected threat calculation. Also, our calculations of the impact of threats assume that no action is taken in any of the areas (afforestation, for example) that can preserve forest value.

When evaluating the key threats, we do not consider the “CO2 fertilization effect,” the phenomenon of higher CO2 concentrations in the atmosphere increasing the growth rates of trees. Studies show that this effect is insignificant in magnitude and unlikely to balance the negative effects of climate change.4

Note 4: “Tree Ring Evidence for Limited Direct CO2 Fertilization of Forests over the 20th Century,” Global Biogeochemical Cycles, September 2010.

Quantification of the Impact of Actions

On the basis of historical and projected data, we assess the potential of six areas of action to preserve current forest value. (See Exhibit A3.) Our analysis assumes effective enforcement of regulations.

Three areas for action tackle the deforestation driven by forest-risk commodities (beef, soy, palm oil, and timber), and they do so from three different angles: boosting sustainable and productive agriculture, promoting sustainable sourcing, and reducing meat consumption. To quantify the impact of these three levers, we project the loss of forest due to unsustainable sourcing of each of the four forest-risk commodities. Our projections are based on historical and/or projected data. (See Exhibit A4.)

In the report sidebar “The Interdependence of Trees and Climate Change” we project CO2 emissions between now and 2050 under two scenarios: one in which no action is taken in our six areas and global temperature increases as much as 5°C and one in which action is taken in all six areas and the global temperature increase is limited to less than 2°C. To model these two scenarios, we converted the tree biomass carbon lost due to deforestation and degradation into CO2 by multiplying by the ratio of the molecular weight of carbon dioxide to that of carbon (44/12). We made a number of assumptions to calculate the CO2 emissions from forests due to deforestation and degradation and the capture and storage of CO2 from existing and new forest areas and from wood products.

The calculation of forest CO2 emissions is based on the total carbon stock used in the calculation of our climate regulatory value. We assume that 100% of forest carbon stock is released as CO2 for those areas that are deforested and that about 40% of the carbon stock is released into the atmosphere in areas where forests are degraded.

The carbon sequestration and storage calculation in our model has three primary elements:

- To estimate how much CO2 existing forest area absorbs, we derive the average sequestration rate (0.68 tons of CO2 per hectare annually) of existing global forests by dividing the total amount of carbon absorbed annually by total projected forest area.5

- To estimate this figure for newly forested area, we use average FAO estimates of annual carbon sequestration potential of afforested area.6

- To estimate how much carbon is stored in wood products, and how much CO2 that represents, we used historical FAO data to project harvest wood product production and assumed that carbon storage expands as new products enter the pool and contracts as existing products decay.7 The impact of wood products on global CO2 emissions is derived by estimating the change in the amount of carbon stored in wood products from one year to the next. The longer a product’s lifetime, the slower the carbon is released back to atmosphere. With regard to our six areas for action, we expect that higher recycling rates, as well as a larger share of sustainably managed commercially used forests, will extend the lifespan of wood products through improved reusability and durability and thus enlarge the carbon sink (total amount of carbon stored). All figures are reported in GtCO2 (1 GtCO2 = 1,000,000,000 tons CO2).

5. “Global Forest Resources Assessment 2015,” Food and Agriculture Organization (FAO) of the United Nations; “New Estimates of CO2 Forest Emissions and Removals: 1990–2015,” Forest Ecology and Management, September 2015.

6. “State of the World's Forests 2001,” Food and Agriculture Organization (FAO) of the United Nations.

7. Consistent with IPCC’s 2013 Revised Supplementary Methods and Good Practice Guidance.