Kick-starting the market is not enough—governments need to plan, orchestrate, and incentivize the buildout of EV charging stations, setting the stage for private investment.

The future of mobility will be electric, with electric vehicles squarely in the center of climate-friendly transportation options. But as the EV ecosystem evolves , the industry finds itself in a classic chicken-or-egg dilemma: Which comes first, the electric vehicle or the charging station?

EVs require charging—but charging stations in most countries are still relatively few and far between. When consumers consider buying their first EV, therefore, many have “range anxiety”—wondering if they will be stranded on the highway as gas-powered cars sail by. In fact, a June 2021 survey led by Nissan revealed that “56% of European internal combustion engine (ICE) drivers who are not considering buying an EV believe there are not enough charging points.” Simultaneously, potential investors in EV charging points (CPs) or other EV infrastructure are hesitating until more electric vehicles are sold, creating a financing gap.

While many EV drivers use privately funded chargers at home or work, we still expect 20% to 50% of charging to take place on the road and at destination chargers, depending on the region. And according to a recent survey of European EV drivers by NewMotion, 33% of respondents cannot install a CP at home. Without public charging infrastructure, therefore, EV adoption will remain slow. And with the private sector left to its own devices, this dilemma could bring EV markets to a standstill.

As a result, many governments have already stepped into the gap to kick-start the market. Yet they tend to do so without a clear plan or goals, resulting in early stage open-market chaos. Private players may compete wildly in the more profitable urban areas, adopting competing standards and installing incompatible technologies and redundant charging stations, while rural areas and many highways, with a hazier business case, are left bare—risking hundreds of miles of charge-free road for anxious EV owners.

Government orchestration to resolve these issues is thus essential, especially in immature markets. Most governments have yet to design a central, coordinating mechanism and are struggling to achieve a workable infrastructure ; instead, their efforts to stimulate the market have primarily focused on passing CO2-related regulations or creating incentives to increase demand for EVs and reduce sales of ICE vehicles. They must now turn their attention to ensuring the appropriate, and timely, availability of charging infrastructure.

To do this, governments should coordinate with players throughout the EV ecosystem to create a master plan for the buildout—including the location, timing, type, and number of CPs. They should communicate the plan’s goals to all stakeholders as clearly as possible. And they should incentivize the buildout of CPs until the private sector is ready to step in, especially along highways or in more sparsely populated areas—locations that are less profitable, but essential. Only then can the dilemma be resolved, setting the stage for private investment and creating a self-sustaining market structure—one that will be economically viable without subsidies and other government support.

The Charging Conundrum

Electric vehicles reduce the emissions that contribute to climate change and pollution, and they have already begun to cut global reliance on oil and gas: according to the International Council on Clean Transportation, the lifecycle carbon emissions of standard EVs are 66% to 69% lower than those of ICE vehicles in Europe and 37% to 45% lower than those in China (where EVs run on electricity that is less green due to a higher reliance on fossil fuels). In addition, EVs are up to 40% cheaper to run than ICE vehicles and their once prohibitive prices are dropping as the technology matures and the cost of batteries declines.

Nonetheless, range anxiety is slowing EV adoption. Many consumers are hesitant to buy EVs until they know that they will be able to recharge when and where they want. A 2019 global survey of licensed drivers by AlixPartners indicated that 46% of respondents would buy an EV only if charging stations were as common as gas stations.

These low utilization rates early in the market’s development make for a difficult business case, creating a gap in the ability to fund new infrastructure. The difficulty is compounded by the need for a variety of charging options and locations. Most CPs will be slower units installed where owners spend extended periods away from their cars; for example, in homes, offices, shopping malls, and commercial buildings. However, the CPs placed along highways, in short-term parking spaces, and in rural areas—where drivers may stop only to charge their cars en route—must be faster. (See “Charging Options.”) The business case for these public CPs is particularly hard to make, especially in the early market stages when CPs are not economically feasible: an ultra-fast charger on a highway requires an investment of $100,000 and more, but utilization is still very low.

Charging Options

Charging stations along roads or highways, as well as in some short-term parking spots such as outside of retail stores, would have to offer shorter charging time. Rapid chargers, with 22 kW to 149 kW of power output, can take one to three hours to charge a car to 80%. Ultra-fast or high-power chargers, with 150 kW or more of output, take just 15 to 60 minutes.

The optimal mix of these slow, rapid, and ultra-fast chargers will depend on local conditions, such as housing characteristics, commuting patterns, the availability of public space, and vehicle mix.

Government Kick-Starts and Early Stage Open-Market Chaos

In many countries, governments have responded to this conundrum by kick-starting the market through public funding for charging infrastructure. But they have typically done so without planning the market’s growth, allowing the open market to decide where and what CPs to build.

The results of these early efforts have often been chaotic. In the early stages of Berlin’s program (2010 to 2015), for example, the government launched a variety of subsidies to grow charging infrastructure but failed to establish adequate guidelines or requirements, resulting in underutilized EV charging stations that were not commercially viable.

The EU also failed to establish central coordination, planning, and standardization in the early stages of the market—inadvertently generating CP redundancy and a lack of interoperability. In fact, instead of a seamless experience, 63% of EV drivers in the EU needed multiple charging membership cards as of 2020, with an average of 2.5 cards per driver, according to NewMotion.

In the US, competing standards have led to many CPs being unable to service more than one type of vehicle. As a result, drivers have arrived at CPs they found on a map, only to discover that they can’t use them—a frustrating situation that reduces trust in the EV charging experience. In addition, a lack of open access to charging data has meant that numerous EV services end up advertising incomplete or outdated station information to drivers.

Government Orchestration

Given the lack of successful infrastructure development to date and the issues often resulting from the early stage free-market approach, it is time for governments to do more, orchestrating a response that boosts EV adoption and incentivizes and subsidizes the buildout of optimal public CP infrastructure. In addition, they will need to determine:

- How they will attract private-sector involvement and interest

- How to set pricing and tariffs

- Whether to establish mandates on standards, interoperability, and roaming platforms

- How to use and govern the data generated by CP usage and payments

Governments should begin by defining the high-level market structure they believe most likely to be sustainable in the long run, the role of the different players, and the level of competition to be allowed, bearing in mind country-specific targets and conditions. In addition, they should determine which part of the value chain they want to control and how they envision market development.

To make the EV charging business self-sustainable, the general trend is toward establishing a market-based model that can be economically viable in the mid- to long term without significant subsidies or other government support.

Create a National Master Plan

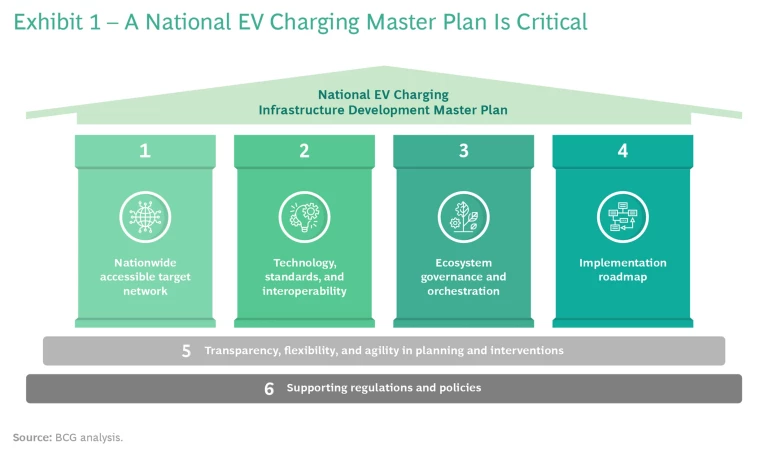

To succeed in this complex undertaking, our experience in the most advanced markets tells us that governments should create a national master plan for EV charging infrastructure and accessibility, one that will ensure that the EV ecosystem is supported, that public-private partnerships have the right frameworks, and that the private sector is confident this is an attractive sector worth participating in. This plan must include six key components. (See Exhibit 1.)

Nationwide Accessible Target Network. As a first step in laying out their master plan, governments should agree on high-level infrastructure goals, establishing targets such as network size, optimal locations, affordability, accessibility, and even construction timing. Weighing existing experiences from CP buildouts globally and comparing them to previously established goals can guide decisions and help avoid mistakes from the past. For example, what should the split of private and public charging be? What is the minimum highway coverage to avoid range anxiety? What is the optimal ratio of EVs to public chargers?

A strong national master plan for EV charging infrastructure and accessibility is necessary to ensure that the private sector sees it as an attractive sector worth participating in.

We recommend plotting out all CP locations in advance, bearing in mind the mix, spread, and use of different types of locations in which people might charge their cars. For example, the government may decide to place a fast charger every 50 miles on highways across a region and a charger in every zone of a certain size, e.g., every 50 square miles. It is also critical that governments ensure inclusive and convenient charging access for low- and mid-income users who cannot easily upgrade their homes for EV charging.

Analyzing the current CP coverage and coverage gaps can help determine the most appropriate infrastructure for the geography, traffic, user needs, locations, and conditions of each region in question . The German government has done good work in this area, creating a centralized toolkit for identifying and coordinating charging requirements down to the individual street level. The toolkit also shares information about newly built CPs with the public and helps market participants become more informed as they bid for CP contracts.

Note that slower public and workplace chargers will cover most of the need for CPs, at a much lower CAPEX than fast chargers. Thanks to high traffic, and thus value creation for the businesses involved, private-sector investments would have a good economic return in these locations.

Fast and ultra-fast chargers, in contrast, require more careful planning and monitoring, since they are needed in pivotal locations to secure universal coverage, reduce range anxiety, and increase confidence in EV adoption. Gas stations and highway rest areas ideally should offer these faster chargers.

As a part of this entire process, governments should also determine the investments required for electricity grid upgrades and create a comprehensive transition schedule, coordinating it with existing mobility targets such as ICE bans and specific EV-ICE sales-share targets.

Technology, Standards, and Interoperability. The master plan should specify the interoperability of CPs, which should not be captive—rather, they should be able to serve any customer using any service provider. This will help maximize charger utilization, improve the customer experience, and optimize CP investments. Interoperability implies technical usability, a back-end connection for customer authorizations and B2B settlements, and the ability of customers to make payments.

Interoperability, with charge points able to serve any customer using any service provider, will help maximize charger utilization, improve the customer experience, and optimize CP investments.

There are different technical approaches to interoperability, which should be established through back-end connections, not just plug compatibility. Many markets initially used peer-to-peer connections and mandatory payment options to allow any user to access the CP (e.g., via credit card). However, a “roaming” approach can offer a simpler, centralized, back-end response that gives customers access to the entire CP network. (See “Roaming.”)

Roaming

In contrast, roaming solutions provide a back-end connection through a cloud-like system that allows any player to join the entire system, offering services on any charger (within the agreed commercial terms). Regions that design their interoperability around roaming can:

- Reduce their connection costs

- Use centralized data to optimize the charging network

- Foster competition by removing barriers to entry;

- Create simpler, standardized B2B interactions and transaction settlements

- Create a better customer experience

The Netherlands has been using roaming solutions to ensure CP interoperability through a central body since 2011. Any CP membership will allow the user to charge anywhere in the Netherlands, with total transparency on availability and prices.

Governments should also establish technical, grid-connection, and safety standards, including standard communications protocols—both between CPs and vehicles and among leading ecosystem players—to support smooth CP access and interoperability.

Lastly, it is important for governments to take a broad, supportive perspective on complementary technology solutions, such as battery swapping (swapping a discharged battery with a charged one rather than waiting to charge) or off-grid solutions (for locations in which there is no access to the power grid) to account for different situations and environments.

Ecosystem Governance and Orchestration. A governing body should be established to help early stakeholders—government entities such as municipalities and the departments of energy, transportation, technology, and the environment—and other ecosystem players coordinate and agree on the way forward.

This governing body should define the EV charging ecosystem, which will eventually include many different players such as OEMs, utility companies, charging specialists (which provide access cards, apps, payments, and the user front-end), investors, entrepreneurs, and NGOs. Many of these players will need a business case to move forward, including subsidies, incentives, and other assurances of government support. Others will be involved at the foundational level; for instance, governments should involve electricity grid operators to facilitate the connection of EV charging infrastructure, such as by choosing locations where the grid is less constrained.

A well-governed ecosystem can help the market avoid the competing standards, redundancy, and lack of interoperability found in many rollouts to date. The governing body should therefore act as a central coordination and orchestration unit for the EV charging ecosystem. In fact, we see a centrally coordinated market as a key success factor, with e-mobility targets, consistent action plans, and central economic support. Norway, the Netherlands, and China have already established such systems.

We see a centrally coordinated market as a key success factor, with e-mobility targets, consistent action plans, and central economic support.

In the Netherlands, for example, six electricity grid operators created the Elaad foundation in 2009 to install EV charging infrastructure in collaboration with municipalities. Elaad is now the knowledge and innovation center of the smart-charging infrastructure field in the Netherlands, where grid operators monitor the infrastructure and coordinate connections between public charging stations and the grid. In contrast, markets that have not reached their potential, including the UK and US, have primarily struggled to design a central coordination and governance body.

Implementation Roadmap. Governments should communicate everything they hope to achieve—from the target network to the interoperability approach and the ecosystem governance—to gain buy-in from members of the charging ecosystem and create a roadmap to attaining these achievements. This implementation roadmap should include clear milestones and the roles and responsibilities of key public and private stakeholders.

A good place to start is by creating public-private partnerships, such as offering public land concessions to private players to install public CPs or establishing multistakeholder platforms to facilitate dialogue and collaboration. Governments should also work with the private sector to determine the best incentives and subsidies—for example, tax reductions and exemptions, grants, or low-interest loans—and to define allocation methods and timeframes. Any incentive must include some measure of accountability to ensure these public funds’ efficient use and their contribution to the sustainability of the EV charging sector. For instance, Enova SF, a Norwegian public entity responsible for EV charging subsidies, has linked its subsidies to periodic progress reports to ensure that the original tender requirements are being met.

Transparency, Flexibility, and Agility in Planning and Interventions. Underlying the entire plan, governments need the flexibility to adjust and adapt to learnings from the evolving EV market if they are to avoid the pitfalls met by earlier efforts. They should therefore develop the plan both dynamically and transparently, including the continuous publication and update of the EV charging network, progress, spending, and incentives. A government will also need a transparent mechanism for intervention in case of market failure—including when, how, and for what duration—to give a clear signal to the market of how serious it is about ensuring success.

Supporting Regulations and Policies. Finally, starting from the early days of the process, the master plan should be underpinned by a comprehensive regulatory framework for EVs and EV charging infrastructure addressing every topic from ecosystem definitions to a public- and private-charging playbook. It should facilitate building, operating, and using EV charging stations while ensuring that some parts of the market will be open to competition, sparking innovation. We look to Germany’s federal Master Plan for Charging Infrastructure as a good example. Although it was a few years in the making, it created a legal framework enabling accelerated infrastructure development.

There are many potential policy tools that governments can utilize within this framework. At a minimum, these should include a regulatory and legal basis for efficient market operations; incentives for EV purchase and usage and the development of charging infrastructure; a supervisory mechanism; and financial subsidies and funding models.

In addition, governments should ensure there are no regulatory barriers that hinder the rollout, such as building codes or grid operator permits. For example, Germany recently passed a law that allows any apartment owner to install an EV charging station without the neighbors’ approval, as getting such approval—as previously required—was often difficult.

A Comprehensive Approach

Whatever the details of the master plan, all governments should aim to roll out a nationwide, publicly available CP network that takes into consideration and supports the needs of the entire country. They should go beyond declarations about targets, instead defining, planning, and monitoring the most appropriate EV charging ecosystem and the role of the public sector , allocating the right incentives and subsidies, and supporting the implementation start to finish.

This comprehensive approach will send a strong signal to the market and to current and potential EV owners and will be critical to creating regulatory certainty, addressing financing gaps in the early stages, developing clear and transparent governance, and coordinating the actions of ecosystem players and stakeholders.

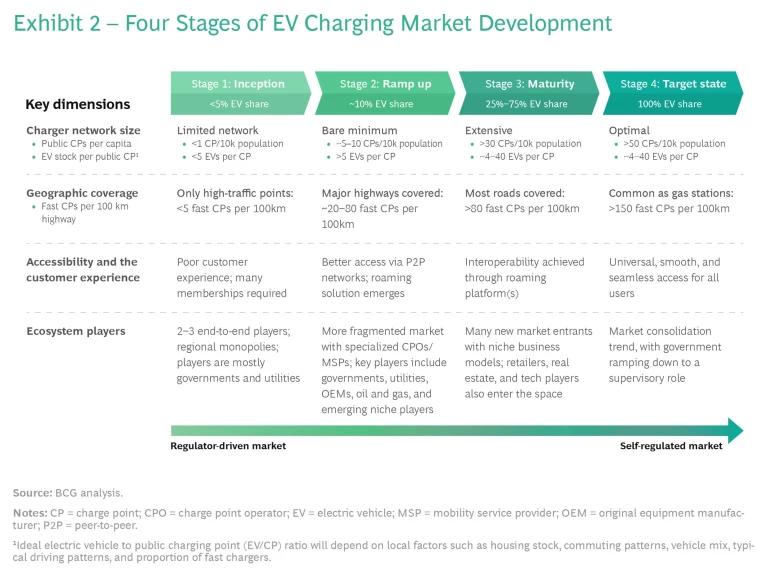

Four Stages of Market Development

A master plan will help governments shepherd their market quickly and effectively through the four main stages of development that we have seen across regions, which we have labeled the inception, ramp-up, maturity, and target states. Our analysis finds that the EV charging market is still in the initial stages in many countries, and even the most mature markets (China, Norway, the Netherlands, and California) have not yet reached the complete target state. (See Exhibit 2.)

We offer four key dimensions for measuring progress through the four stages:

- Size of the charger network, from a limited network in the inception phase (fewer than 1 CP for every 10,000 people) to an optimal network in the target state (more than 50 CPs per 10,000 people)

- Geographic coverage, from few CPs available on roads and highways in the inception phase to CPs as common as gas stations in the target state

- CP accessibility and the customer experience, from a poor customer experience (for example, many membership cards required) to universal, smooth, and seamless access for all users

- The landscape of players in the ecosystem, beginning with two or three end-to-end businesses and regional monopolies in the inception phase, shifting to a fragmented and competitive market in the ramp-up and maturity stages and then to a consolidating market in the target state with the government winding down to a purely regulatory role

Governments should plan to evolve their role from acting as the protagonist in the inception stage to a supervisory role in the mature market.

As the EV charging market matures, the growing value chain and larger number of electric vehicles on the road will make it more attractive to the private sector. Governments should therefore create a plan to evolve their role from acting as the protagonist in the inception stage to serving as an enabler in the ramp-up and maturity stages and, finally, to a supervisory role in the end state. This evolution will mean defining and redefining their actions, priorities, and use of resources at each of the four stages, as well as market-control mechanisms such as pricing, interoperability, and regulations, while accounting for country specifics and priorities.

Key Success Factors

Although there has been relatively little global progress to date, we believe that the EV charging dilemma can be resolved and the market ultimately succeed with the right approach, and there are many lessons available from early efforts to guide the way. Some successful government actions to date have included the following.

- Ensuring the timely availability of public EV charging infrastructure by eliminating barriers such as permitting requirements, or difficulty in accessing land from municipalities

- Providing seamless access to all CPs and a smooth charging experience for EV users by preventing different operators from setting up their own access cards or procedures

- Deploying resources efficiently by, for example, using adequate criteria when determining charger locations, thus avoiding low CP utilization rates

- Ensuring fair, transparent, and comparable pricing for EV charging—not an easy task, given our finding of significant pricing differences within a single country for similar charging levels

- Supporting an attractive, fair, and inclusive private charging market, one that will foster competition while ensuring that the most vulnerable customers—those who cannot afford home chargers or who reside in isolated regions—are not left behind

Many regions have taken ten years and more to get where they are today—whether they have a nationwide, compatible CP network or are still in the inception phase—but no country can wait another ten years to implement the right framework and master plan. Green deals and climate change initiatives are accelerating the EV timeline , and governments need to be sure that when these vehicles hit the road, their charging network is ready: widespread, broadly accessible, consumer-friendly, affordable, and seamless. The ad hoc approach taken by many regions to date will not achieve this target.

While local and regional differences mean there is no single path to an ideal CP infrastructure, many lessons can be learned from EV charging experiences around the world. Above all, each region will need a strong, individualized master plan and government support, as well as an accelerated ramp-up and a roadmap to success—all within the next five years.