Gaming & esports is a vibrant and fast-growing sector, powered largely by the passion of 3 billion enthusiasts around the globe. With its substantial revenue potential, the high-quality jobs it creates, and its reputational benefits, Gaming & esports presents rich opportunities for industry and national governments alike.

Gaming & Esports: A Fast-Growing Industry Sector

Gaming and esports are distinct yet integrated ecosystems, combining to form a sector that presents rich opportunities for both industry and governments.

Encompassing a range of electronic amusements where players interact with an interface or input device to produce visual feedback , video games have emerged as a global cultural force. They compete for individuals’ leisure time with other entertainment activities like movies, books, and the arts. As evidence of their popularity, the video game Grand Theft Auto V, for example, set seven Guinness World Records since its release in 2013, including a world record for US$1 billion of sales within three days of launching.

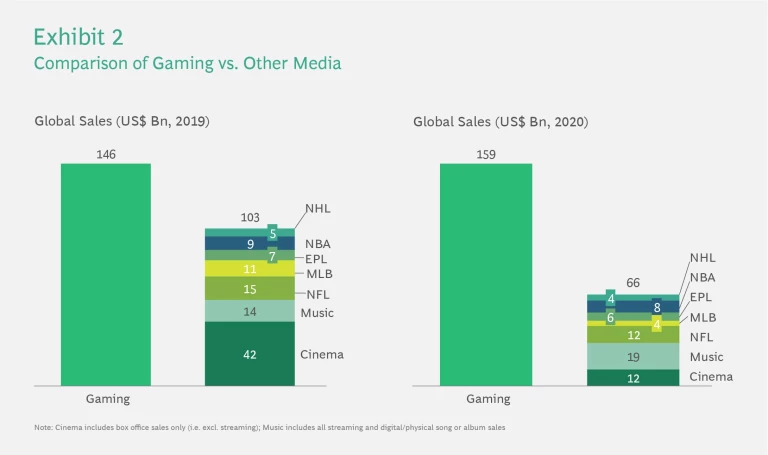

Annual global gaming revenue will exceed $200 billion by 2023, which is more than worldwide box office earnings, music streaming and album sales, and the top five wealthiest sports leagues combined.

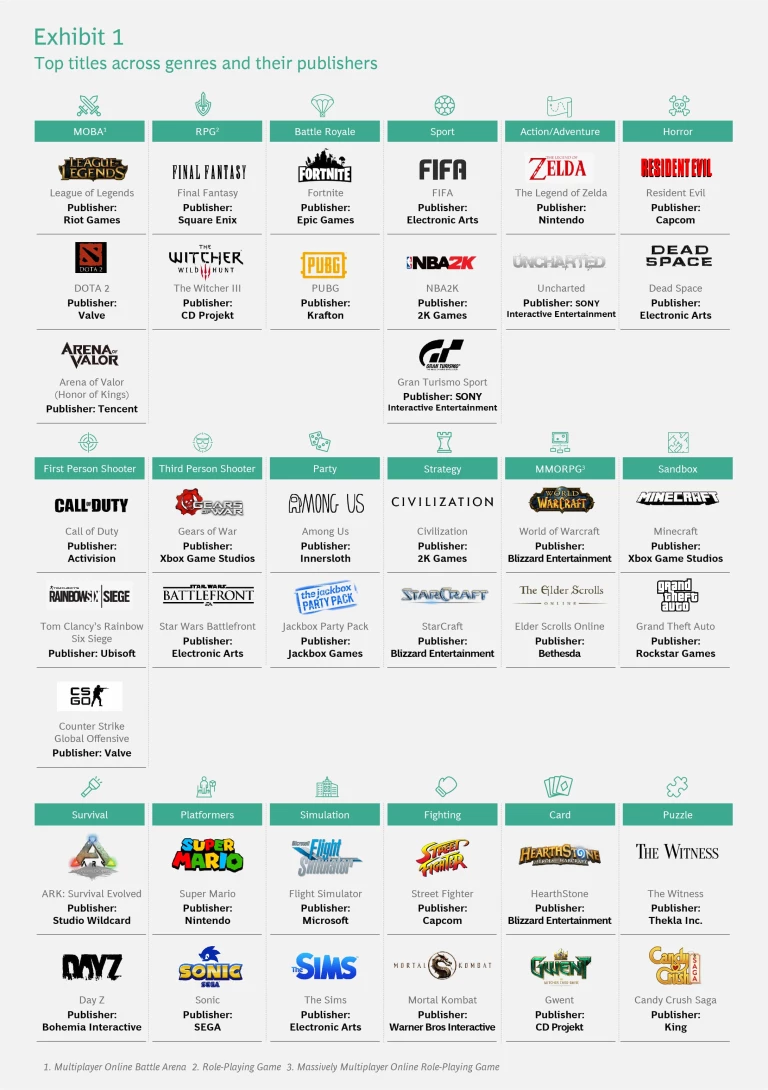

Games and the publishers behind them compete across a landscape of different genres (Exhibit 1) and platforms (mobile, PC, and console – discussed in next section). Even within a specific genre, the differences between titles is stark. From graphics and game mechanics, to the overall theme and subject matter, consumers have an immense selection to choose from. Some genres are sub-genres of others (e.g., Multiplayer Online Battle Arena, or MOBAs, came from Strategy games) and some titles are hybrids of genres (e.g., GTA is an action/adventure sandbox with some role-playing game elements). While no standard classification exists, the industry does a good job of self-managing the categorization of genres.

Esports is a subset of gaming and refers to competition involving video games – people playing against one another (individually and in teams) for prize money and global recognition. Many esports competitors have risen to the reputation and compensation levels of professional athletes. The 2019 Fortnite World Cup Final (a leading sports title) was held at Arthur Ashe stadium, home to the US Open. The event drew up to 2.3m viewers, and the winner earned $3m in prize money. By comparison, 2.7m viewers tuned in to watch the Men’s Singles final of the last US Open. Netflix has said that Fortnite is a bigger competitive threat than HBO

The Gaming & esports sector has grown faster than anyone could have imagined and is now a $175B-ayear business growing at a ~10% CAGR.

Newzoo forecasts that annual global gaming revenue will reach over $200 billion by 2023, almost 8% annual growth from $138 billion in 2018

This dramatic growth is spurred by a gigantic and expanding consumer base, willing to spend money on their passion. The number of gamers globally had been growing at 6% CAGR, with the pandemic and global lockdowns further accelerating that trend. By the end of 2021, 3bn people in the world will be considered “gamers”. Hungry for novel entertainment, these enthusiasts have devoured new releases. Gabe Newell, owner of Valve, a video game developer, publisher, and digital distribution company, notes that when an update is released for the company’s DOTA 2 (another leading esports title), worldwide internet traffic grows by 2-3%

BCG conducted a consumer survey covering 10,000 people in 10 countries globally (countries selected per region with leading average revenue per consumer). Respondents identifying as gamers are fairly evenly split by gender (57% of respondents were male, 43% female). Fourteen percent of respondents were below the age of 19, another 14% between the ages of 19 and 24, 35% between 25 and 35 years of age, and another 37% between 36 and 50. Seventy-seven percent of respondents indicated some form of employment. Of those, ~60% reported spending at least US$20 on additional in-game features over the last 12 months, with ~25% spending US$50 or more. This does not include the cost of purchasing a game, or any associated hardware purchases. Many games are free-to-play, and monetize through in-game microtransactions that users conduct to enhance their experience. Other popular games, however, currently retail at US$60-$70 for a new release

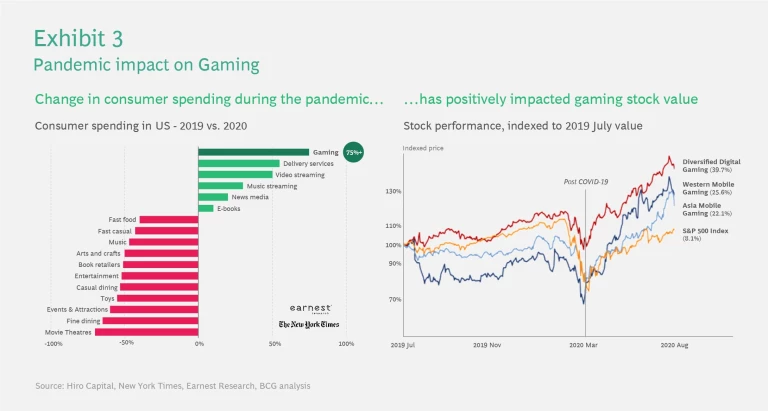

Already a strong performer, the gaming market has significantly outperformed the S&P 500 since the beginning of the COVID-19 pandemic (Exhibit 3). In the US, gamers have increased their spending on gaming by +75% over the course of the pandemic

The Gaming & Esports Ecosystem

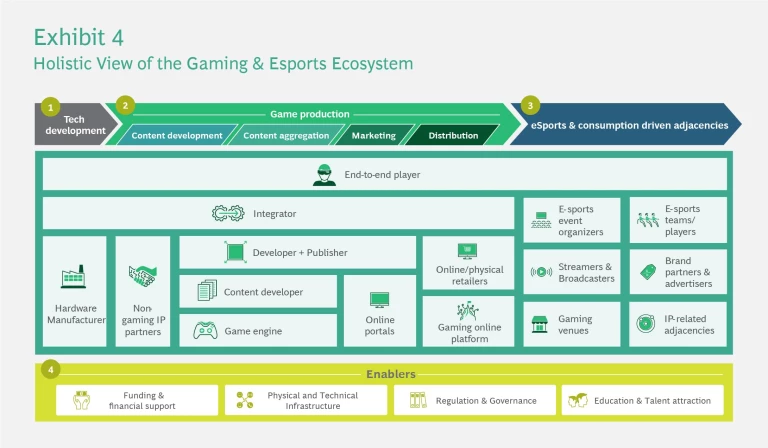

Gaming and esports share a common value chain up to and including game distribution, after which esports continues through events and other consumption-driven adjacencies (Exhibit 4). It is populated by a wide variety of companies, from end-to-end players like Sony and Microsoft to niche content developers, distributors, gaming venues, and so on.

Technology Development

Technology development focuses on the hardware, or platforms, that enable the games. Platforms on which people play fall into one of three main categories: console, PC, and mobile. Smartphone users account for much of the industry’s recent growth. Major console manufacturers include Sony, Nintendo, Microsoft. But there is some blurring across platforms. Earlier this year, for example, Nintendo announced an OLED Model of its popular Switch platform, featuring a larger, crisper display, catering to gamers-on-thego and emphasizing Switch’s positioning as a hybrid console / handheld device. Valve has also announced the forthcoming release of SteamBox – a handheld gaming PC with direct integration into its Steam distribution platform. These kinds of platform innovations will likely continue to support the handheld console market, despite the flexibility of mobile and PC options and emergence of “cloud gaming”.

Cloud gaming essentially removes the need for expensive hardware, with game processing performed in the cloud.

Cloud gaming is to gaming as video streaming is to traditional home video/DVD. Where consumers used to buy a physical DVD or purchase a digital download, they now just stream movies or tv directly from the web. Similarly, cloud gaming replaces discs or downloads, and consumers only need a controller at home, rather than a bulky Nintendo or PlayStation console.

Margins on consoles have been shrinking, and Nintendo, Microsoft, and Sony have increasingly relied on game purchases and in-game monetization to earn their profits. Cloud gaming could replace consoles with lower-cost devices that are more dynamic for consumers and easier to produce. However, cloud gaming demands top-tier connectivity with low lag times to provide an enjoyable experience. As a result, we see early deployments of the technology into markets with the most advanced infrastructure (e.g., Google Stadia’s release in US and Western Europe).

The next evolution in immersive gaming experiences will likely be delivered in a combination of virtual reality and augmented reality environments. Like Niantic’s 2016 Pokemon Go, and later Harry Potter: Wizards Unite, these technologies promise the seamless blending of real world and fantasy. This trend is shifting the technology development frontier to items like VR headsets and AR-enabled smartphones

Game Production

Game production comprises everything from scoping the game (e.g., budget, genre, storyline, gameplay concept) to the conceptualisation, design, development, monetization model and distribution. Game production accounts for most of the value in the sector, with content development capturing more than half of the value created.

Monetization models range from hypercasual games that generate revenue through ads and/or in-game microtransactions, to decade-old franchises that continue producing sequel after sequel, selling millions of copies to the global following they have garnered. Between 2007 and 2020, Ubisoft released 24 titles for their Assassin’s Creed franchise (including main series and spin-offs), selling over 150 million copies in that period.

Several trends are expected to shape the future of game production. The first is industry consolidation. We have seen significant M&A activity in recent years, as large publishers, media conglomerates, and other technology players acquire studios globally. The second is changing industry norms. It has traditionally been dominated by “crunch” – the expectation of long hours of unpaid overtime to meet key milestones in the development cycle – and a historically young male-dominated work culture

Esports and Consumption Driven Adjacencies

Esports is a subset of gaming and is simply defined as competitive gaming, played individually or in teams (Exhibit 5). Not all video games become esports titles, but all esports titles are video games. Although numerous video games have competitive formats, popularity is highly concentrated around the top 10 games, which account for 88% of esports hours watched

Organized tournaments range from amateur competitions to well-established professional leagues with multimillion dollar prize pools. While gaming, mostly done at home, generally has experienced a significant push through the pandemic, esports, which often feature live tournaments, has taken a small hit or successfully shifted activities towards online competitions.

Looking forward, we see professionalization and legitimization of the sport continuing to enhance overall perception, and attracting investment and sponsorship from within and outside the sector.

The roles of Publishers and Organizers in the ecosystem, and their corresponding share of profits, will also continue to evolve. Publishers like Epic Games, Riot Games, Electronic Arts, Valve, and Activision Blizzard, who own their games’ IP rights have traditionally been the most powerful players in the esports world. But as the industry grows, so too does the role of Organizers, and the development of rules, regulations, processes, and behind-the-scenes operations

Mobile esports continues to grow in selected markets but its global future is uncertain. Firstly, it is unclear how transferable the competitive gaming experience is from PC and console platforms – where esports lives today – to mobile. Current mobile esports titles are limited to a handful of genres, with only a few actually drawing much competitive attention. Whether esports will grow on mobile as they have on the other two platforms is an open question. Secondly, it is unclear how attractive watching people playing games on their phones will be to a wider audience. Audience participation and experience will surely need to be enhanced to keep people interested and engaged. And finally, it is unclear how publishers of leading mobile esports games will treat their IP going forward. They may opt to enhance their in-house monetization by taking a more active role in their IP’s esports operations (like Activision Blizzard and Riot Games have done), leaving the organizers with fewer mobile titles to feature. This would stifle the ability for other publishers‘ mobile games to piggy-back on an established mobile esports event, in turn slowing the segment‘s growth.

Several adjacent businesses have emerged with the rise in gaming and esports consumption, which leverage gaming and IP for other use cases. These include:

Streaming. There is a growing trend toward streaming gaming content as form of entertainment. Streaming spans a range of content and attracts several consumer segments: fans watching an esports competition; gamers looking for tips and tricks to improve their play; and community members following their favorite influencers’ / streamers’ content. Twitch is the clear incumbent platform, capturing ~75% of total content hours watched across all major platforms.

Advertisers and Sponsors. Historically, sponsors endemic to the gaming industry like Nvidia and Intel have also been major proponents of esports. But as its popularity has grown, other sponsors and advertisers are joining the fray, investing in both teams and events. These new players include Red Bull, Vodafone, numerous professional athletic clubs.

Gaming Venues. Venues are evolving from the traditional gaming centers like Wanyoo – a chain of more than 1,200 esports destinations in 50+ cities, boasting over 10 million members worldwide – to a more specialized esports-focused “third-place” experience. (Colloqiually, the first place is the home, second place is the office, and third place is a consumer‘s favorite coffee shop/bar/hang-out.) An example of this specialized experience is esports Arena, North America’s first dedicated esports facility. Developed in partnership with Walmart, and now with 50+ locations, it offers community-driven and crowd-funded events, as well as game launches, streaming, tournaments, and retail merchandise.

IP-Related Adjacencies. Popular games and esports have spurred an avalanche of derivative media content, merchandise, and themed experiential entertainment. For example, Netflix has created new content based on Dota (a leading esports title) and The Witcher (a leading single-player adventure game). Universal Studios Japan has a Super Nintendo World, with another under construction in Hollywood.

Enablers

Underpinning the gaming and esports ecosystem are four key enablers: funding, infrastructure, regulation, and education.

- Funding. Funds flowing into gaming firms over the last 18 months have already exceeded the total amount invested over the previous five years. Investment in video game companies was US$5.8b in 2018 and US$7.6b in 2019. In 2020, ~650 transactions (~220 M&A deals, ~400 VC/corporate/private investment, and ~30 IPOs) were completed totaling US$33b. The largest deal was Microsoft’s acquisition of Zenimax for US$7.5b. Other major deals have been announced in 2021, but observers expect to see a correction from the previous year’s boom. Investment is coming mainly from within the sector, but media conglomerates, telcos, tech players, and financial institutions have all entered the space, eager to capitalize on its potential.

- Infrastructure. Telco operators provide the core infrastructure needed to serve the growing Gaming & esports consumer base. The offering of greatest concern to the gaming and fan communities is enhanced connectivity (low ping). Sri Lanka Telecom and Telecom Egypt, for example, both offer gaming data bundles. Telcos regularly supply connectivity gadgets to major esports events, which also allows them to associate with the gaming community.

Telco operators can expand their Gaming & esports activities by focusing on other parts of the value chain. In technology, they can follow the lead of Saudi Telecom Company (STC) and others, and forge partnerships with cloud gaming service providers to distribute their platforms. Zain has joined forces with Nvidia GeForce, UAE’s Etisalat with Gamestream, and British Telecom with Google. - Regulation. The implications and objectives of sector regulation and governance differ based on the maturity of the ecosystem being governed. In developed markets with an established Gaming & esports scene, regulation seeks to ensure a globally competitive environment for developers and publishers. Lobbyists petition lawmakers on behalf of industry participants to support that objective. For example, in the United States, the Entertainment Software Association brings together the major publishers and industry players to reflect common interests, such as combatting copyright infringement.

In developing markets, where a nascent industry is finding its footing, regulation focuses on establishing the right framework suited to local context, and nurturing the regional ecosystem. In Spain, for example, AEVI brings all the industry stakeholders (including esports) together under one organization that consolidates, prioritizes, and champions their collective agenda with the government. Key issues include securing public funding for game development, and treatment of esports competitors as athletes. - Education and Talent Attraction. Traditional academic institutions (e.g., USC, UT Austin, SMU) are now offering Bachelors and Masters level degree programs in game development, digital innovation, esports management and administration, and entrepreneurship, often in partnership with local industry players. And numerous specialized academies like DigiPen or Laguna College of Art + Design have integrated gaming curriculum into their offering, boasting ~90% of graduates employed in the sector within 2 years.

All four of these enablers are currently driven by private sector players. But they can also be bolstered by direct government action, as discussed in the following section.

How Governments Are Enabling Ecosystem Growth

Governments care about the Gaming & esports sector for several reasons:

- Economic Impact. They wish to benefit from the industry’s rapid growth and increasing potential contribution to GDP. Especially right now, they see that making big bets can reap commensurate returns. Governments also view Gaming & esports as an important key to unlocking adjacent sectors like software development, AR/VR, hospitality, and tourism.

- Job Creation. They are eager to create job opportunities in a thriving and dynamic sector. Increasingly, Gaming & esports is a major employer within many countries’ entertainment industries. Furthermore, these are good jobs, employing well educated and technologically savvy people, fostering innovation, and generating substantial economic value.

- Soft Power/Reputation. Acquiring a reputation in Gaming & esports is great for a country’s image. It announces the country’s relevance, at the forefront of designing and driving 21st century sport, culture, and entertainment. With Japanese anime and South Korean K-Pop, we have seen gaming as the vehicle for expanding global cultural influence. Countries at the center of the Gaming & esports ecosystem can also become global destinations for large-scale events.

- Enhancing Quality of Life. The Gaming & esports sector expands residents’ entertainment options, and allows them to share in a global phenomenon. And to the extent that a country’s telecom, technology, and hospitality infrastructure can improve the gaming experience, this also enhances participants’ quality of life.

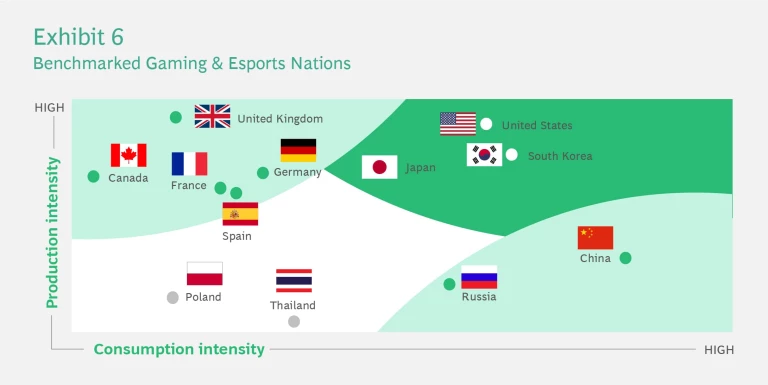

BCG benchmarked leading gaming nations based on the intensity of their Gaming & esports consumption and production to identify best practices globally (Exhibit 6). Consumption intensity was measured by the total market size, consumer engagement (casual and competitive players), and amount of adjacent gaming content consumed (e.g., streamed video content). Production intensity was measured by the total Gaming & esports revenues, number of entities engaged in Gaming & esports activities, and maturity of enabling infrastructure (including education, funding, etc.). Nations were then grouped into three archetypes: (1) Producers: countries that produce more Gaming & esports content than consume; (2) Consumers: countries that consume more Gaming & esports content than they produce, and (3) Leaders: countries that lead globally in Gaming & esports content production and consumption. Below we share key lessons learned and examine selected countries in more depth.

Funding and Financial Support Lessons

Four distinct types of support emerged as key enablers. The first is direct financial support for new companies in the Gaming & esports sector, including seed funding and bank loan facilitation for startups. The second is availability of business incubators and accelerators to help develop and grow new startups and turbocharge existing players. The third is provision of ongoing subsidies to firms in the sector, such as R&D tax credits and labor cost assistance. And the fourth is an international sector investment strategy with clear ROI and domestic impact targets.

Infrastructure Lessons

Two types of infrastructure proved particularly important: telecommunications and physical venues. Strong bandwidth and 5G capabilities are essential to support modern Gaming & esports trends. Some countries’ telecoms have localized their game servers to reduce latency. Leading countries also fostered ways to bring gaming out of people’s homes and into more shared and public spaces. This includes local gaming centers for grassroots communities to flourish, as well as arenas or stadiums for large-scale esports events.

Regulation Lessons

Leading gaming nations all featured strong information and communication technology (ICT) regulation. This includes: intellectual property and copyright protection, with penalties against piracy; favorable company setup laws and regulations; favorable labor law and permits; a straightforward and transparent licensing process; and streamlined and lenient age rating criteria. Overall, these governments acknowledged and legitimized the Gaming & esports sector and esports players. They had established visions and strategies to accelerate industry growth, and worked with private institutions like trade associations to steer the national agenda.

Education and Talent Attraction Lessons

Building the right local skillsets and actively attracting talent are critical to building national strength in the sector. Leading countries offered gaming course and degree offerings (e.g., engineering, arts and graphic design, management) with a focus on practical application. More broadly, they cultivated a highly skilled workforce with a range of technological and artistic capabilities. They fostered partnerships with leading global gaming universities and institutes for student exchanges and academic research, and offered gaming internships and training programs. Leading nations also promoted and destigmatized Gaming & esports careers. We found that liberal values and a focus on diversity and inclusion attract talent and allow this creative industry to flourish. Finally, top countries in the sector have developed and nurtured a grassroots ecosystem. They have built esports training facilities with world-class coaches and robust instruction programs. These in turn help to attract global events and allow teams to train with the best.developed and nurtured a grassroots ecosystem. They have built esports training facilities with world-class coaches and robust instruction programs. These in turn help to attract global events and allow teams to train with the best.

Deep Dive: UK, South Korea and Saudi Arabia

In this section we examine UK and South Korea in more detail, as specific examples of what leading nations are doing with respect to the four enablers. We then look at how these are being implemented by KSA, a more recent entrant into the sector.

UK – Historical Production Powerhouse

UK enjoys a high production intensity compared to its consumption intensity – it produces a lot relative to the size of its gamer population. Much of this is rooted in its rich history of developing games for personal computers. Since the 90s, UK has created some of the gaming world’s most iconic franchises like Grand Theft Auto and Tomb Raider.

- Funding and Financial Support

The country’s Video Game Tax Relief (VGTR) program uses a ‘Cultural Test’ to offer 25-80% tax relief on games produced in the UK (with a minimum of 25% of core budget required to be expensed in UK or EU). This test awards points for games being set in UK, featuring British lead character, or developed in the UK. Since the program’s inception in 2014, GBP 444m has been paid out across 1,460 claims, of which 50% have involved international industry players (e.g., Sony, Sega). Additionally, the UK Games Fund is a pool of grants awarded to game startups in the UK (conditional on minimum of 50% of total project budget to come from external sources). Since its introduction in 2015, GBP 5.2m have been paid out – and 170 funding applications were received in 2020 indicating a healthy, and well-received initiative for the gaming sector. - Regulation and Governance

In 2020, the Association of UK Interactive Entertainment (UKIE), the main gaming industry trade body, developed an 8-point plan to boost UK esports. Many of these points involve close government engagement and support, including communication campaigns, regulatory stability, and alignment with the Department of Digital, Culture, Media & Sport. - Education and Talent Attraction

A shortage of local talent to fill key technical game development roles led the British government to add several specific roles to the “Shortage Occupation List”, including web designers, game developers, UX designers, and VFX designers. This designation allows local companies to more easily attract and recruit foreign talent. For example, it exempts them from the 28-day local job market listing period, prioritizes the issuance of work visas, and permits lower minimum salary sponsorship obligations.

South Korea - Global Esports Capital

South Korea is the 11th largest video game development hub in the world. Called the Hollywood of professional gaming, it features a densely packed, cost-efficient network of competitors, managers, and sponsors.

- Funding and Financial Support

The Korean esports Association (KeSPA) subsidizes amateur esports clubs out of its US $60M+ annual budget. And strong amateur clubs receive additional sponsorships from the ecosystem and their communities. Teams may be sponsored by global brands like Logitech, regional players like Chinese streaming service DouYu, but also by local businesses, including software companies, creative agencies, and even educational and healthcare institutions. This support ensures that developing players get salaries early and can devote more time to their training. Professional for-profit clubs, however, are exempt from government fundi - Infrastructure

Fundamental to South Korea’s gaming and esports dominance is its state-of-the-art connectivity infrastructure. The country also offers over 20,000 gaming centers called PC bangs (“PC rooms”) where participants play massive multiplayer games for a modest hourly fee. They are popular as social meeting spots, and for their expensive, high-end computers specifically designed for video gaming. A project is currently under consideration to establish minimum requirements for PC bangs to streamline quality. A new esports arena opened in Busan in 2020, supported by US $2.7M in government funding. - Regulation and Governance

Government agencies including KeSPA and the Korea Creative Content Agency (KOCCA) were early movers in establishing a clear vision for gaming industry, with defined mid- and long-term plans, and a strong focus on esports (Exhibit 7). The country is home to the International esports Federation, and the industry receives strong support from the Ministry of Culture, Sports and Tourism. The societal prevalence of gaming, and 24-hour operations of many PC bangs have led to an unfortunate rise in addiction to the activity. South Korea has responded with gaming rehabilitation centers and a strong anti-addiction lobby, driving regulatory changes like a ban on late-night gaming for young children. - Education and Talent Attraction

South Korea systematically nurtures and develops gaming talent, and supports esports players throughout their careers. Specialized courses and training facilities encourage esports players from an early age. A “club-system” similar to that of European football supports amateur clubs and offers talented players the possibility and path to become pros. The government also helps post-career players, after they retire at age 25, with pensions and job placements.

Kingdom of Saudi Arabia – Ambitious newcomer

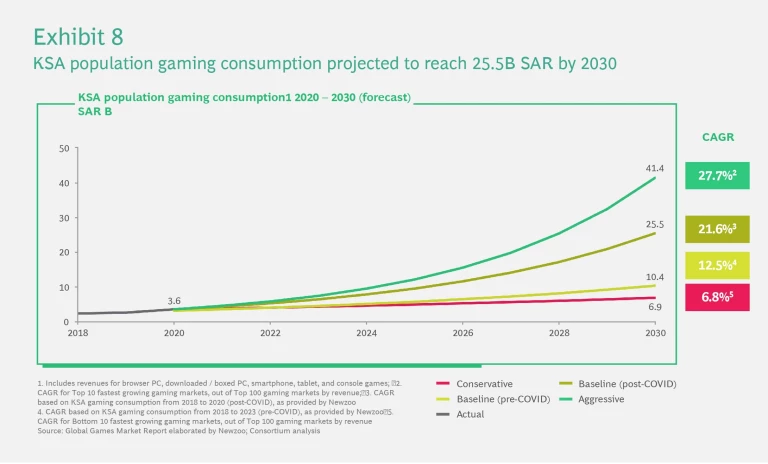

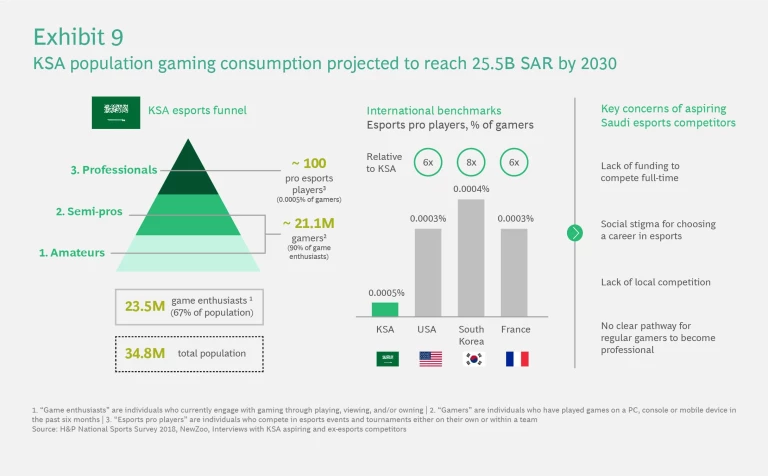

KSA presents an interesting example of a country seeking to translate a passion for gaming, reflected in its high level of consumption intensity, into a corresponding production intensity. From a population of 34.8M people, 23.5M or 67% identify as game enthusiasts

Increasing by an average of 22% CAGR, gaming consumption in Saudi Arabia is projected to reach USD 6.8 Billion by 2030.

The Kingdom is already home to several notable MENA game developers. Veteran Semaphore Productions has been around since 2010, and released several titles, one of which appeared at E3’s PC Gaming Show in 2016. UMX Studios, established in 2014, has produced several titles with distinctly local flavor like CSD – Climbing Sand Dunes, a sand dune climbing simulator. It is now beginning to venture into the console space. Manga Productions opened in 2017. Originally an anime house, it has expanded into the world of video games with several releases, each increasing in visual complexity and gameplay appeal. The country also boasts multiple esports champions and finalists over the last decade, including:

- Abdulaziz Al Shehri – FIFA World Champion 2015

- Abdullatif “Latif” Alhmili – Fighting Games finalist 2016

- Khalid Aloufi – FIFA Ultimate Team Regional Champion 2017

- Mosaed AlDossary – FIFA Ultimate Team Champion 2018, FIFA eWorld Champion 2018, FIFA Ultimate Team Champion 2019

- Najd Fahd – FIFA eFootball World Championship 2020

Funding and Financial Support + Education and Talent Attraction

Manga Productions is a MiSK company – MiSK being a government sponsored non-profit focused on cultivating KSA’s youth as stewards of the region’s economy. This demonstrates the significance gaming and game development plays in the government’s vision for the future.

The Ministry of Communications and Information Technology (MCIT) and DigiPen (world-leading game design academy) recently collaborated to launch the Game Changers program. It is designed to provide “unique career pathways for entrepreneurs in the Saudi game industry”, increasing the number of independent game company startups. Participants begin with a 6-week overview of the game development process and entrepreneurial basics, followed by 16 weeks of intensive training in one of three specialized topic areas: game design; game art and animation; or game programming. They then enter an 8-month game development and incubation phase, with the goal of emerging with a marketable product and viable business model. Selected participants are eligible for a SAR 70,000 grant to take their game’s development further.

Despite this progress, however, talent attraction – especially to the esports sector – faces several structural and societal barriers. Saudi Arabia has approximately 100 pro esports players – representing 0.0005% of regular gamers. In contrast, USA and France have 6x the proportion of pros vs. gamers, and South Korea 8x. Aspiring Saudi competitors note a lack of funding to compete full-time, scarcity of local competition, no clear pathway for gamers to become professional, and social stigma associated with choosing a career in esports

Infrastructure

Communications and Information Technology is a key enabler of the Kingdom’s Vision 2030. In this context MCIT has been investing heavily to develop KSA’s telecommunications and IT infrastructure (especially high-speed broadband), support and grow the relevant business sectors, and create a favorable regulatory environment. All five of the ICT sector’s major 2023 strategy targets imply direct support for Gaming & esports

Regulation and Governance

The Saudi esports Federation (formerly Saudi Arabian Federation for Electronic and Intellectual Sports) was established in 2017 with a mandate to:

- Grow esports in KSA, the region and globally, by promoting, supporting, and facilitating the industry

- Develop local talent to win regional and international tournaments

- Engage all key partners in the Gaming & esports ecosystem

- Lead lobbying to bring esports to the Olympics

Since that time, the federation has hosted numerous league events and tournaments. Perhaps the most notable is its Gamers Without Borders tournament – a multi-title charity tournament attracting competitors from around the world, to raise donations for selected organizations. The second iteration of this event just concluded earlier this year. In 2018, SEF led the creation of the Arab esports Federation alongside 11 other national members, with headquarters in KSA.

Conclusion

Gaming & esports is a fast-growing and continuously evolving sector and offers content producers a platform to connect with consumers in a way that other media cannot replicate. This paper has demonstrated the ability for investors to achieve commercial returns, and for governments to create economic impact. But investors and governments can only create the framework for game developers and esports athletes to grow.

Ultimately, ecosystems emerge from the passion of the consumers - the stories they want to tell and the glories they want to achieve. Gaming & esports speak directly to a shift in the media paradigm, consumers as creators. More than entertainment, they offer an infinite canvas for creation. As government and private sector investment continues to grow, that canvas will keep expanding.