It’s been a few years since your company launched its zero-based budgeting (ZBB) effort. Thanks to a solid design and full buy-in, it was a success, with only a few bumps in the road. Through roughly 100 savings initiatives, you carved out inefficiencies and redirected funds to the company’s business priorities. Once the implementation was done, everyone wondered: what’s next? Interest in the program has now waned, as new members of the leadership team turn their attention to other pressing challenges—and costs are once again on the rise.

Stories like this are becoming increasingly familiar. Over the course of the past decade, companies across many industries have adopted ZBB, reimagining their cost base to unlock funds and reinvest in growth. For one reason or another, what was supposed to be a permanent transformation, a new way of thinking and working, didn’t always take hold. These companies wonder how they can get back on track. How do they get past one-off initiatives and treat ZBB as the new way of operating?

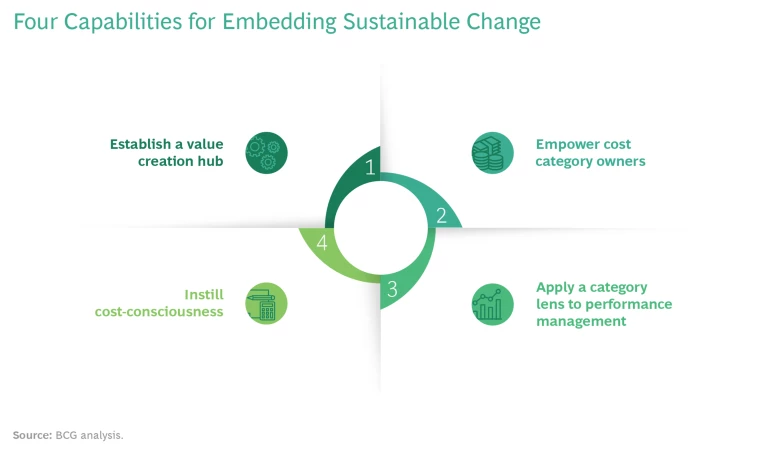

Through our client work, we have identified four ingredients that can help companies ensure that ZBB evolves from a cost-reduction effort to a culture of cost consciousness that fuels continuous improvement over time.

From One-time Effort to Business as Usual

In the past ten years, ZBB has come a long way, from a niche cost-cutting approach to a widely adopted cost management technique with a proven ability to reduce the cost base. But few companies have tried to figure out how to sustain a zero-based transformation once the one-off measures have been completed and the implementation has run its course. Still, some have managed to integrate zero-based thinking into the fabric of their daily operations. What is the secret of their success?

We have observed that companies that derive ongoing value from their zero-based transformations, regardless of industry, organizational structure, or corporate culture, all share four practices or enabling capabilities—a mix of governance, structure, process, and behavioral changes. (See the exhibit.)

Establish a Value Creation Hub

Every enduring success story entails a ZBB “nerve center,” what we call a value creation hub, to guide the transformation. This entity, which can vary in size and structure, functions as the core ZBB governance body. It owns the company’s value creation agenda—cost performance and reinvestment—and oversees both strategic decisions and operational activities. For example, it recommends whether and how to expand ZBB scope, when and where to identify and scale new efficiency opportunities, and how costs are budgeted and monitored. The hub also owns and maintains all ZBB-related assets, including its cost taxonomy, category playbooks, spending policies, KPIs, and reporting.

Among its most critical functions, the hub administers the company’s reinvestment framework, which governs how savings are reinvested back into the business to fuel incremental growth. This framework has two key components: a set of principles on how to reinvest savings in accordance with the business strategy , and a clearly defined process that distinguishes savings from reinvestment, so that neither is compromised.

A clear reinvestment framework is often a critical prerequisite to achieving full organizational buy-in. Its principles should incentivize people to actively pursue inefficiencies in order to reallocate the freed-up funds to new and innovative uses. Money is reinvested against strategic priorities (for example, new-product development or acquisitions), based on incremental financial commitments and in accordance with ZBB efficiency guidelines.

Few companies have tried to figure out how to sustain a zero-based transformation once the one-off measures have been completed and the implementation has run its course.

Operationally, the hub team designs and manages how ZBB is integrated with existing business activities by identifying opportunities, managing monthly performance, and providing input into the annual budgeting cycle. Let’s highlight how these three activities work at a large global health care company.

In one instance, the company’s Asia-Pacific business unit was falling short of its target in the technology category. In response, the business unit proposed shifting data center operating systems to open-source software, which don’t require licenses. The hub supported the region by validating the business case and connecting the region to the relevant experts in IT, finance, and procurement to ensure that the initiative was rigorously scoped and assessed—and that it would be scalable.

During implementation, the hub ensured that monthly financial and operational reports were updated to track progress and impact of the pilot initiative. It incorporated those reports into regular regional and global cost category performance reviews.

What started out as a mitigating action eventually led to a global rollout, saving the business millions in annual IT licensing costs. Once the pilot, and others like it, proved successful at a local level, the hub took action to scale them and lock the benefits into the annual budgeting cycle. It gave cost category owners (CCOs) and their teams a pipeline of new opportunities with quantified, ongoing improvements, associated operational KPIs, and lessons learned. These inputs now help the CCOs and global financial planning and analysis teams engage in constructive, fact-based discussions, enabling them to make annual targets and budget owners’ plans as rock-solid as possible.

Empower Cost Category Owners

CCOs are tasked with managing each cost category enterprise-wide. They play an important role during the project phase, when they are responsible for rigorously challenging existing costs, aligning the organization on new ways of working, and then overseeing implementation of the initiatives. Critically, successful ZBB companies recognize that the job of the CCO is not over when the initial savings have been realized. CCOs and their teams continue to provide strategic direction for their cost category, sharing best practices and promoting continuous improvement by regularly identifying and launching a stream of new initiatives.

CCOs play a crucial role in providing ongoing support to budget owners. They challenge and stress-test expenditures to ensure that they are supported by the right cost drivers. In doing so, CCOs become trusted advisors to budget holders, helping them meet or exceed their targets, bridge unexpected gaps, mitigate anomalies and risks, and support rapid responses to internal or market changes (such as COVID-19’s impact on travel, media buying, or the supply chain). They also help budget owners strike the right balance between efficiency and effectiveness in supporting the overall business strategy.

For example, a global consumer goods company’s marketing function relies on gross ratings points (a measure of the impact of a TV ad) to identify the sweet spot in efficiency and effectiveness. But the optimal threshold is dynamic and must be revisited when changes occur—for example, whenever there are new market entrants or changes in consumer behavior, media consumption, or product mix. Here, the CCO for marketing would actively benchmark performance and work with the company’s marketing executives to ensure that marketing money is generating the optimal return on investment.

CCOs also play an important role in planning and budgeting. At a global automotive company, for example, CCOs provide input into category-specific targets based on business cases; these are shared with budget owners to help them develop sustainable yet “stretchy” proposed budgets that can help the business achieve its profit ambition. Then, during the actual budgeting process, the CCOs constructively challenge budget owners wherever their proposals deviate from target spend or KPIs.

The most advanced ZBB organizations use cost category ownership as an explicit rite of passage in leadership development. They handpick CCOs for their high potential and give them the opportunity to shape the ways of working in their cost category while gaining insight into other areas of the company.

Still, some companies have managed to integrate zero-based thinking into the fabric of their daily operations.

Thus, beyond generating and sustaining savings, the category owner role contributes to succession planning by allowing companies to groom the next generation of leaders. Companies explicitly use category ownership as a mechanism to unearth new executive talent and to provide the people in these roles with a platform to demonstrate and develop their capabilities. In many cases, a successful stint as CCO opens up new internal career paths and/or the opportunity to join the executive team a few years down the line.

Apply a Category Lens to Performance Management

Cost transparency is a cornerstone of ZBB, and not only because it supports objective and more informed decision making. It also allows leaders to balance tradeoffs and track the impact of their budget decisions. Moreover, it helps companies identify efficiency opportunities and address issues early on, before they grow out of control. To maintain forensic spend transparency, successful companies ingrain cost category thinking into their planning, budgeting, and performance reporting processes and systems. So in addition to having a cost center view, they also apply a category lens to every type of spend.

This category lens is activated in four ways.

Targets are aligned to business strategy and are tangible, yet stretchy. ZBB leaders use a number of mechanisms to continually raise the bar in the annual planning process. In addition to scaling new opportunities throughout the year, many businesses also conduct annual challenger workshops where category experts identify and quantify new ideas or evaluate ideas that have been deferred. Drawing on these insights, the CCO team then provides strategic guidance and helps the business set appropriate category-specific targets. During budgeting, the cost category team constructively challenges budget owners to ensure that savings are fully incorporated into budgets and are supported by the right cost drivers.

Category-specific reporting is made simple, accessible, and timely. Successful ZBB adopters understand that to get people at all levels to embrace the new way of working, it’s vital to keep the process as streamlined as possible without compromising the granularity of information that ZBB provides. Typically, this involves creating user-friendly, web-based self-service dashboards and automating report production. These category-specific reports are then embedded into monthly performance reviews.

Reporting focuses on spending effectiveness, not just efficiency. In order to serve as the single version of truth for the entire business, reporting must focus on balancing efficiency and effectiveness. Financial results are presented in context, with supporting operational KPIs that show spend patterns, effectiveness thresholds (ROI metrics), and functional drivers. A contextualized report provides transparency about the cause of any variances, whether favorable or adverse. In this way, it gives decision makers confidence that savings are sustainable if they are coming from the right places—and provides the opportunity for rapid response if they are not.

For example, a global retailer’s monthly media buying report would show the total cost from the P&L, operational KPIs (such as length of ad versus target, total number of spots, and impact on reach), and commercial KPIs (such as actual versus forecasted sales). A decline in total cost might seem positive, but not if it came at the expense of spurring sales. Running shorter or fewer ads could risk undermining the message, which would also hurt sales and eventually thwart growth.

CCO teams support the business to review performance and achieve plans. As the business starts to review performance through a category lens, CCO teams are responsible for providing category-specific support and insight. CCO teams monitor financial and operational metrics, investigate variances, and suggest mitigating actions where required. They also share leading practices and instigate new efficiency initiatives for their categories, thus enabling the business to execute against plan.

Instill Cost Consciousness Throughout the Organization

Instilling a cost-conscious mindset and behaviors in employees is the hardest, and perhaps the most important, building block of culture change. The proper incentives and messaging must be put in place and reinforced, and they must be adapted as people gain familiarity and experience with the program and processes and confront new challenges.

All successful zero-based transformations start with a compelling case for change that captures the hearts and imagination of employees. The narrative should be simple, bold, urgent, and irrevocable. It should clearly explain the need for cost consciousness and how it enables the company strategy. The case for change must then be translated into tangible actions that apply to employees’ day-to-day work. Through training, playbooks, job aids, and process changes, they can then see what’s in it for them.

Companies that derive ongoing value from their zero-based transformations all share a mix of governance, structure, process, and behavioral changes.

Executive incentives and organizational performance targets need to explicitly promote cost consciousness to ensure that the right behaviors are recognized and rewarded. This also ensures that business unit performance targets are aligned with the overall strategy and that any cross-functional tradeoffs are reflected across the affected units through shared KPIs.

Organization leaders play a critical role in advancing the cultural shift. They consistently articulate the narrative and act as role models to live and breathe the change. They take symbolic actions and communicate candidly with employees about their individual change journeys—for example, holding virtual meetings and adopting a hybrid working routine, and consistently seeking a strategic rationale (and economic justification) for events and sponsorships. Adherence to the new ways of working as well as continuous improvement can only be sustained if the right behaviors are infused into the organizational DNA.

Successful ZBB organizations go a step further to define, encourage, and incentivize cost consciousness in every aspect of their HR processes. They incorporate the desired mindset and behavior across all stages of the employee life cycle, from job descriptions and recruitment to training, performance management, and promotion criteria. Having held a CCO position for 24 months could be a key criterion for promotion to a global leadership position.

In addition, companies deploy accessible, high-impact communications and change management techniques to advance culture change. Organizations issue succinct, regular communications to maintain momentum. They celebrate successes and showcase best-in-class behaviors by sharing stories and rewarding exemplars. They also explicitly tie ZBB success to business strategy, showing the tangible ways that ZBB is helping the company realize its goals. Finally, successful companies understand that it’s essential to facilitate change at every level, from senior executives to frontline employees. That means identifying pivotal interventions that drive lasting change, such as training marketing personnel to consider efficiency and effectiveness KPIs when planning, helping procurement measure the true impact of KPIs on the P&L, and supporting HR in devising performance frameworks that reward the right behaviors. Only by addressing individual mindsets and behaviors at these levels can a company embed cost consciousness at the core of its culture.

In this fast-moving digital era, companies with forensic spend transparency and the ability to rapidly optimize and reallocate resources are best positioned to seize opportunity, disrupt, and forge ahead confidently with their business strategy. Here, ZBB plays a critical role. By taking the four measures described above, companies can ensure that their zero-based transformations take root, move beyond one-off initiatives to sustain the change, and instill a culture of cost consciousness throughout their organization.