The cost of food is rising rapidly, and hunger is on the increase. What will it take to build a better way to feed the world?

What might the global food system look like in 5, 10, or 15 years? Various futures are imaginable. Perhaps Africa will have achieved far more food sovereignty. Protectionism might cause food prices to rise dramatically. A few Global North countries might dominate agricultural trade, displacing smallholder farmers elsewhere. Or—just maybe—the world might come together, collaborating to slow climate change, boost global agricultural trade, and relieve hunger among the world’s most vulnerable populations.

It is, of course, impossible to know exactly what the future holds in store. No one can accurately forecast precisely how climate change will affect global food production. That’s because climate change and other factors—such as geopolitical conflict, high debt burden among low- and medium-income countries (LMICs), and major advances in agricultural technologies—that will affect the food system over time are deeply interconnected and subject to very high levels of uncertainty.

Unquestionably, the combined impact of COVID-19 and Russia’s invasion of Ukraine has stressed an already fragile global food system to the breaking point. Prior to the war, a grim combination of inequitable food distribution, increasing protectionism, enormous amounts of food waste and loss, and overdependence on a few crops had led to massive malnutrition and outright hunger. More recently, exports of Ukrainian and Russian wheat, fertilizer, and other key products have disappeared from markets worldwide. As we described in a recent article , the effects of this change have been dire: rapidly rising prices for the food needed now and for the inputs and fuel required to produce and move the food that the world will need tomorrow.

As efforts to relieve the immediate impact of the food crisis continue, stakeholders—including governments, multilaterals, NGOs, and the private sector—must also look to the future. Will concerted efforts to relieve the current food crisis and stabilize the food system succeed? Or will they fail to provide sufficient food and the means to grow it equitably and economically? Will the almost $700 billion in annual subsidies dedicated to supporting the food system make a difference in the next decade?

This article lays out four scenarios for the future. These scenarios are not forecasts. Rather, they represent our best efforts to envision the contours of a stretched-but-plausible world in which we might have to operate—or rather several versions of such a world—depending on how certain key factors and their underlying uncertainties play out. Our hope is that examining these scenarios will promote thoughtful consideration of what the global food system might look like in 5 to 15 years, provide the basis for stakeholders to prepare for a wide range of as-yet-undetermined contingencies, and encourage stakeholders to devise strategies and actions for building the most abundant, equitable, and resilient food system we can.

The Status Quo

Although Russia’s invasion of Ukraine is the immediate cause of the current food crisis, at least three other factors have been instrumental in exacerbating it. The COVID-19 pandemic disrupted global supply chains and food systems, dramatically increasing food prices and leaving up to 1.6 billion people—one-fourth of the world’s population—without access to adequate food. The pandemic also exacerbated the massive debt burden borne by LMICs, as they directed scarce funds toward defending their populations against the disease, making it more difficult for them to offset fast-rising food, fertilizer, and fuel costs. And finally, the effects of climate change are having a significant deleterious impact on farming yields.

Climate change has had devastating impacts on global agriculture already. Land degradation has reduced the productivity of 23% of the world’s agricultural land (especially in Africa and South Asia), and up to $577 billion in annual agricultural production is at risk from pollinator loss. As the world gets closer to the 1.5°C temperature increase threshold, the agricultural sector is absorbing an estimated 25% of the total damage and losses from climate-related disasters. In the emerging debate over payments from historically high-emitting countries to emerging markets for loss and damages caused by climate change, the food system has started to feature prominently.

Yet these impacts have only further exposed the inherent fragility of the global food system. Global agriculture produces enough food to feed the world, but as much as 30% of the food produced is lost or wasted, even as increases in crop yields are slowing. And a rise in protectionism and trade wars has limited the equitable distribution of available food and caused global food prices to rise.

Moreover, the global food system depends heavily on just a few crops and offers limited support for diverse, nutritious diets. This level of concentration increases the system’s exposure to the catastrophic effects of sudden adverse events. Meanwhile, at a global level, smallholder farmers—a large proportion of whom are women—produce most of the world’s food but receive an average of just 4% of the final price of food as payment for their work.

In short, our global food systems severely lack resilience and are highly vulnerable to external shocks, as the crisis brought on by COVID-19, climate change, and the war in Ukraine all too clearly demonstrates.

Factors and Uncertainties

In generating our scenarios, we focused on three overarching factors that are sure to impact global food systems over the next five years: the state of the world’s agriculture, climate change, and global economic and geopolitical dynamics. How each of these factors plays out—and how they affect the Global North and the Global South—is subject to high levels of uncertainty.

The state of the world’s agriculture will largely determine the kinds of food required and the capacity of global food systems to grow and distribute enough to feed the world. Four key variables will govern this factor: production and trade, the characteristics of various agricultural supply chains, new technology and innovation, and shifts in food demand and consumption.

The impact of climate change on global agriculture over the next five years is highly uncertain. It will be determined not just by the effects of natural and human activity on land, ocean, atmosphere, and weather events but also by the nature and extent of the policies, strategies, and technological innovations designed to address those effects—and by world’s willingness to act. These impacts are even more difficult to forecast as we look beyond the next 15 years.

Global economic and geopolitical dynamics include a range of uncertainties, including the level of country debt following the COVID-19 pandemic and future capital market flows, borrowing capacity, credit ratings, prices, inflation, and economic growth. Geopolitics—including the outcome of the war in Ukraine, the emergence of other conflicts, changing power dynamics among countries and regions, and the rise of nationalism—will also play a significant role. And the possibility and potential impacts of future pandemics can only be guessed at.

Four Scenarios

All of these uncertainties are evolving in parallel, creating a highly complex environment that renders attempts to sort out a probable future essentially impossible. Under such conditions, scenarios are an especially useful way to ponder different stretched-but-plausible future states that may face stakeholders in the global food system and to develop appropriate responses to them.

Each of the scenarios discussed below—which we call “Uneven Progress,” “The Rise of Africa,” “Every Country for Itself,” and “Coordinated Step Forward”—offers a distinct vision of the middle-term future, developed through careful consideration of how the various key factors noted above might play out. As valuable as the scenarios may be in efforts to imagine what the future might look like, their core value lies in their capacity to trigger thinking about the strategic implications of each one, as well as about plans and potential actions needed as the future unfolds, regardless of what form it ultimately takes.

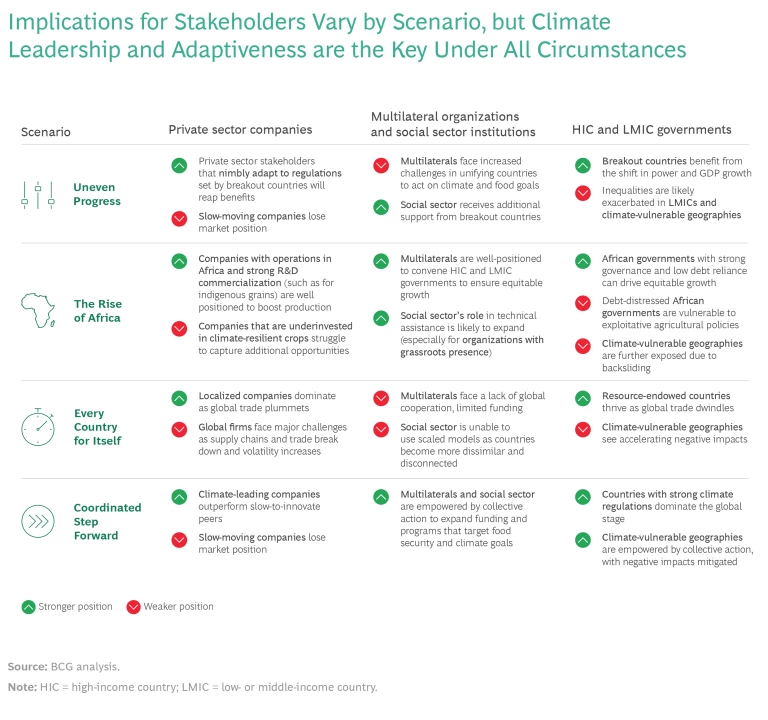

Although future events will not match any of the scenarios exactly, each scenario entails strategic repercussions for the three stakeholder groups—governments, multilateral and social sector organizations, and private sector companies—that have major stakes in the food systems of the future, and each suggests no-regrets moves that each stakeholder group should consider taking after weighing the strategic implications. (See the exhibit.)

Scenario 1: Uneven Progress

Global coordination stalls, but a few breakout nations among high-income countries (HICs) in the Global North lead a policy-driven development agenda and promote the uptake of existing climate-smart technologies. Meanwhile, inequity worsens as extreme weather decimates the Global South, food availability declines, and prices increase unevenly across the world.

In this scenario, global supply chains become concentrated and dominated by countries such as Canada and the Nordics that build on their low-carbon exports. Agricultural technology remains focused on industrial and contract farming, displacing smallholder farmers around the world. The Global South suffers in the face of ongoing high debt, as the world—and especially Europe—prepares for increased numbers of climate refugees.

This scenario has a number of strategic implications:

- Private sector companies that adapt nimbly to the breakout countries’ regulatory agenda will reap benefits, while their slower-moving rivals lose market position. If climate-focused countries begin to dominate the global agenda, companies that invest in decarbonizing their supply chains and developing climate-resilient agricultural inputs and healthier processed foods are likely to benefit the most. Nurturing strong relationships with key governments could help promote joint investments toward a more resilient food system.

- Multilateral organizations hoping to persuade countries around the world to act in unison on climate and food goals will meet resistance, but social sector organizations could gain considerable backing from breakout countries in support of their own climate and food security agendas. Doubling down on climate mitigation and food system resilience efforts could reduce some negative impacts. For example, multilaterals could push for national climate adaptation strategies and encourage bilateral creditors, including the private sector, to restructure debt for debt-distressed countries.

- Governments in breakout countries will benefit generally from favorable agricultural yields and from the shift of power in their favor, resulting in considerably higher-than-average GDP growth. But most LMICs—especially those in climate-vulnerable geographies—will face greater internal inequality. To weather the impacts of this scenario, LMIC governments should invest in duty-free protocols through regional trading blocs, including strengthening food and fertilizer import facilities and developing integrated decision support systems across data sets and government ministries to tackle climate uncertainties.

Scenario 2: The Rise of Africa

In this scenario, Africa accelerates its agriculture potential through unprecedented South-South cooperation, technology transfers, and private sector investments, especially from countries such as India and China. Overall, food availability and productivity increase, prices drop, and hunger declines, but the benefits are not distributed evenly across the continent. Moreover, intensified agriculture leads to backsliding on climate goals.

This scenario imagines a world in which reduced global trade results in more powerful regional trading blocs. Shorter food staple supply chains lead to intensified agriculture, notably in Africa, thanks in part to rapid adoption of technological advances in climate-smart agricultural inputs. At the same time, however, increased protein consumption on the continent and a lack of international consensus on climate policy cause greenhouse gas (GHG) emissions to increase there and elsewhere.

The strategic implications of this scenario are as follows:

- Private sector companies that have strong commercial investments in Africa (specifically in climate-smart technologies that can boost production of local crops and encourage regenerative farming techniques) will be well-positioned under these conditions to boost production and take advantage of untapped agricultural capacity. Given the potential for disruptions in global trade, companies that shore up their supply chains will also prosper.

- Multilateral organizations will probably be able to work successfully with HIC and LMIC governments to ensure equitable growth, and the role of social sector NGOs—especially those with a grassroots presence—in providing technical assistance is likely to expand. Both multilaterals and NGOs will play critical roles in coordinating public-private sector partnerships to boost climate-smart production, providing official development assistance and technical support to reduce debt in Africa, and supporting higher-value processing activities.

- Governments in Africa that can maintain strong governance and low levels of debt will be better positioned to drive equitable growth within their borders. But those with high levels of debt may be forced to rely on resource extraction, further exposing those in the most climate-vulnerable geographies to the impacts of climate change. In general, African governments that establish clear incentives for climate-smart agriculture and investments in local infrastructure such as storage facilities will emerge on top.

Scenario 3: Every Country for Itself

A self-sufficiency narrative takes root globally, leading to significant reductions in global agricultural trade. By necessity, alternative foods such as millet replace global commodities. However, limited climate action leads to a point of no return. Resource-rich countries benefit; others suffer.

In this scenario, a significant increase in protectionism has wide-reaching negative effects. Food costs rise and availability declines as global trade collapses by 20%. Supply chains are disrupted and profits in private sector agricultural decline. The failure to stem global warming leads to extreme weather events and further reductions in agricultural yields. Countries rush to protect their populations, but inequality and social unrest increases.

We see a number of strategic implications under these conditions:

- Private sector companies with global reach will face major challenges as trade and supply chains break down and volatility increases, while companies with strong localized presences will come to dominate their markets. Private sector companies that adopt more “glocal” approaches to sourcing, procuring, and accessing resources will be able to reap the benefits of local opportunities while limiting their reliance on global networks. This will strengthen their ability to offset the challenges arising from the breakdown of trade and global supply chains, and to meet consumer demand within their borders. Multinationals may find it beneficial to spin off local business units in some circumstances.

- Multilateral organizations will likely be severely hampered by the lack of global cooperation and by limited funding, and organizations in the social sector will struggle to scale their operating models across disconnected, uncooperative countries. To offset the decline in international cooperation, multilaterals may need to encourage donor governments to embrace a massive recommitment to aid and investment goals—including debt relief programs for smallholder farmers—and to initiate a dialogue for bilateral debt forgiveness and a fundamental restructuring of monetary instruments. For their part, NGOs that can counteract resistance to cooperation through deep, in-country presence may be better situated to identify and cultivate key local partnerships to overcome these challenges.

- Governments in countries that are well-endowed with resources will thrive as global trade dwindles, but the negative impacts of climate change will accelerate in countries most exposed to global warming. Governmental action will be critical in reducing the risk of food price volatility and the resulting potential for unrest. LMIC governments will be more resilient in this scenario if they invest in strengthening strategic grain reserves and alternative commodities through local value chains and in improving local infrastructure.

Scenario 4: Coordinated Step Forward

Spurred by a food system disaster exacerbated by Russia’s invasion of Ukraine, greater global coordination in climate policy and agriculture gains momentum. This promotes adoption of existing climate-friendly innovations. The private sector is pressured to follow along, especially benefitting companies that made early strategic bets on green ventures.

In this future, collective action yields to numerous benefits. Global trade rises, and supply chains grow more resilient and transparent, significantly reducing food waste and loss. Demand shifts toward more nutritious, environmentally conscious foods such as plant-based proteins. A global consensus emerges on slowing global warming, leading to investment in climate-friendly and humane agricultural practices, including better protection of arable land and decreased GHG emissions.

This scenario has the following strategic implications:

- Private sector companies that lead in helping mitigate global warming will outperform their slower-moving, slow-to-innovate peers in a world where cooperation is essential. As the private sector faces increasing regulatory and consumer pressures to act more transparently and sustainably, companies that have simplified and shortened their supply chains for staple crops, invested in alternative nutritious grains to create triple bottom line impact—social, environmental, and economic—and scaled up techniques for sustainable sourcing and food and packaging waste reduction will reap the benefits. These companies can balance the desire for near-term profits with consideration of the market potential and resulting long-term business gains in LMICs.

- Multilateral and social sector organizations will be able to significantly expand funding and programs that target food security and climate goals through collective action. They may also push for climate finance commitments focused on adapting to the impacts of global warming and increasing development aid to support climate adaptation and mitigation.

- Governments in countries with strong climate regulations will dominate the global stage, while those in countries more vulnerable to global warming will mitigate negative impacts through collective action. In this scenario, LMIC governments that have already begun creating demand for a range of diverse crops via subsidies, minimum price supports, and public procurement will be better positioned to achieve food sovereignty—as will HIC governments that have clearly defined the policies and actions necessary to facilitate the transition to a green economy, including more aggressive targets for emissions reductions and carbon neutrality.

No-Regret Moves

As important as it is for stakeholders in the public, private, and social sectors to prepare for the wide range of potential contingencies indicated by the four scenarios, it is even more critical for them to begin taking actions that are likely to pay off under any circumstances, with little or no foreseeable downside. These include various activities broadly designed to reduce the impact of future food crises, mitigate global warming, promote global trade, increase global equity, and improve supply chain resilience.

Private Sector. Companies in the private sector companies need to pursue a robust Global North and Global South engagement strategy. Food companies should invest in technologies and delivery models that prioritize climate-smart production of staples and nonstaples, such as disease- and drought-resistant seeds. By diversifying their sourcing strategies and value chains, and reducing food waste, they can help stabilize food prices and protect against future shocks. All companies will benefit from strategies to reduce emissions and invest in green technologies (including energy transition plans) and circularity. They should also work to reduce the productivity gap in the Global South by promoting technology transfers. A better balance between boosting near-term profits and capturing the Global South's market potential will likely mean long-term business gains.

Social Sector. Multilaterals and NGOs must double down on humanitarian assistance to the world’s most vulnerable populations and advocate for and support negotiations to pursue national climate adaptation strategies. To that end, they should urge donor countries to recommit to climate goals in agriculture, including providing increased development assistance to LMICs to support their efforts to mitigate the causes of climate change and adapt to its effects.

Multilaterals should also advocate for restructuring LMIC debt to increase capital flows, including debt relief programs for smallholder farmers, and they should establish alliances among governments, NGOs, and private sector companies to boost food production. Finally, they should promote a sustainable and just energy transition to the benefit of all, including efforts to develop and improve biofuels to avoid competition with food and to use nonfossil fuels for electrification.

Public Sector. HIC donor governments should increase their climate-related development assistance, with the goal of reaching equality targets based on the Gini index of global wealth distribution. For their part, LMIC governments—especially those in Africa and South Asia—need to rethink their food and climate policies and incentives, committing to actions such as industry tax exemptions, time-bound subsidies, minimum selling prices, and strategic grain reserves. Greater investment in integrated climate analytics will help countries monitor and support decision making during agricultural and food crises. And the development of duty-free protocols through regional trading blocs, combined with strengthened import facilities for food and fertilizer, would promote trade in agricultural inputs and products where they are most needed.

Equitability, Sustainability, Resiliency

Our fragile global food system was already stretched to the breaking point. But the dual blows of the COVID-19 pandemic and the war in Ukraine are now causing it to snap in several places. Its lack of resilience has generated severe shocks that have wreaked havoc globally on the accessibility and affordability of high-quality food. The goal of this exercise has been to imagine several possible futures stemming directly from the system’s current state, with the aim of triggering action on the part of all stakeholders to bring about a more resilient, affordable, nutritious, and equitable food system.

The probability that any of the scenarios we’ve imagined will come to pass precisely as described is quite small. But that doesn’t detract from their value to stakeholders looking for guidance in preparing for the global food system’s highly uncertain future, whatever it looks like.

All stakeholders should consider the contingent actions that we outline for each of the four scenarios. But far more important than these are the no-regret moves that we sincerely hope stakeholders will adopt to help create a fairer, more resilient food system—one that can provide healthy, nutritious, sustainable food for all and ensure secure livelihoods for the farmers and food workers who grow and distribute it.

The authors wish to thank Pilar Pedrinelli, Nicole Barman, Emily Fletcher, and David Lee for their contributions to this article.