Imagine a network of bank branches where customers feel at home and trust the staff to find products that truly fit their needs. Staff members greet customers warmly and by name. Salespeople are energized because they know that they are offering value to customers; that each day’s calendar is full of promising appointments; and that the more they benefit customers, the more they benefit themselves. Service colleagues fulfill customer transactions quickly and painlessly, identifying customer needs and sales opportunities at the same time. The leads result in sales and service prompts that are highly relevant for customers. A can-do atmosphere permeates the air.

Many retail banks feel that their branches are well on the way toward achieving such a level of excellence. And a few may be. But the reality is that although many institutions achieve branch excellence some of the time in some branches, only a handful achieve branch excellence most of the time in most branches.

This is of particular concern because branch performance is coming under greater scrutiny as customer behaviors change and profitability pressures steer banks toward multichannel distribution models. (See Distribution 2020: The Next Big Journey for Retail Banks , BCG Focus, March 2013.) Indeed, customers want to interact with their banks anytime, anywhere, just as they do with service providers in other industries. And much debate has centered on a key question: What is the role of the bank branch in this multichannel world?

In our view, branches will continue to play a central role in most retail banks’ overall offerings. As purely transactional services increasingly migrate to direct channels—mainly online and mobile—branches will focus primarily on providing high-value sales and advice as well as high-touch services.

The problem is that relatively few retail banks have capitalized on the opportunity to turn their branches into the brand-building, loyalty-enhancing pillars of profitability that they can truly be. For example, the following occur in many branch networks:

- Non-value-added tasks take up considerable time.

- Tasks that can be performed through direct channels are not actively redirected.

- The agendas of relationship managers (RMs) are not sufficiently filled, and idle time is not productively used.

- Daily and weekly operational rhythms are not sufficiently codified and focused on commercial activity.

- Sellers, tellers, and managers are not working together as a single team with a shared set of objectives.

- Operating practices vary widely, leading to significant performance differences among branches in the same network.

In order to achieve an organizational and cultural transformation that brings out the best in branch networks, banks need to initiate a dedicated branch-excellence program. We have seen such programs improve banks’ cost-to-income ratios by up to five percentage points. More specifically, commercial-excellence levers can increase production by 15 to 35 percent, and operational-effectiveness levers can reduce network employee full-time equivalents (FTEs) by 5 to 15 percent.

Banks need a specific methodology for achieving branch excellence. And although many banks are already resizing and reformatting their branch networks, they need to look beyond that and focus on increasing productivity within their target footprints. They also can learn from the best practices of banks that have achieved a high level of performance—as well as overall consistency and coherence—in branch networks.

The Path to Branch Excellence

When launched and executed well, a dedicated branch-excellence program will transform performance that is merely average up to a level that can be considered good. Similarly, the program will propel branch performance that is already good into the realm of the truly great. Significant results can be achieved within 6 to 18 months, regardless of the bank’s starting point or location.

The path to success, which requires a systematic approach and full engagement of both senior management and line management, lies in a three-phase program: fully diagnose branch network performance, develop a target branch model, and implement commercial and operational improvements.

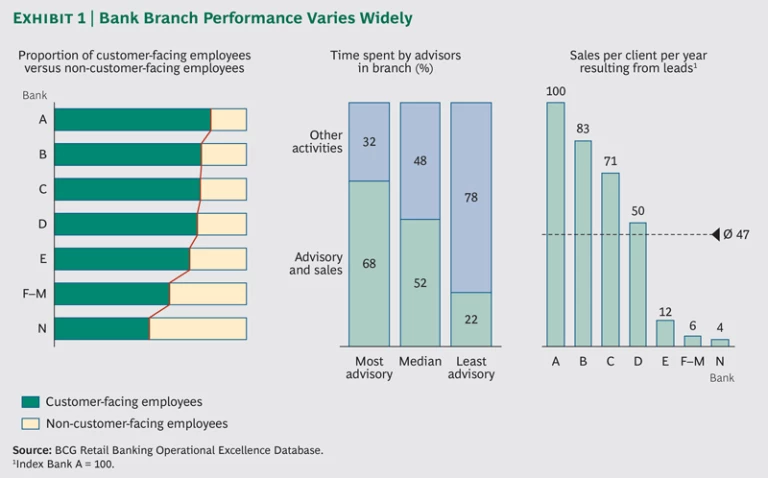

Fully diagnose branch network performance. Diagnosing branch performance begins with an external benchmarking of overall network productivity against top retail banks worldwide. In our work with clients, we have utilized BCG’s Retail Banking Operational Excellence Database, which compares performance among about half the top 40 retail banks globally across up to 160 metrics. Branch performance tends to vary widely. (See Exhibit 1.)

The goal is to provide a holistic overview of a branch network’s commercial and operational capabilities. Key issues include the following:

- How focused is the network on value-added tasks? How much of an advisor’s time is spent on sales and advice appointments? How many appointments do RMs have on an average day?

- What is the quality of sales interactions? How many legitimate leads are generated? How many sales result from these leads?

- How efficient are branch processes? How many transactions does each service FTE in branches and in operations handle each day? What is the average customer waiting time?

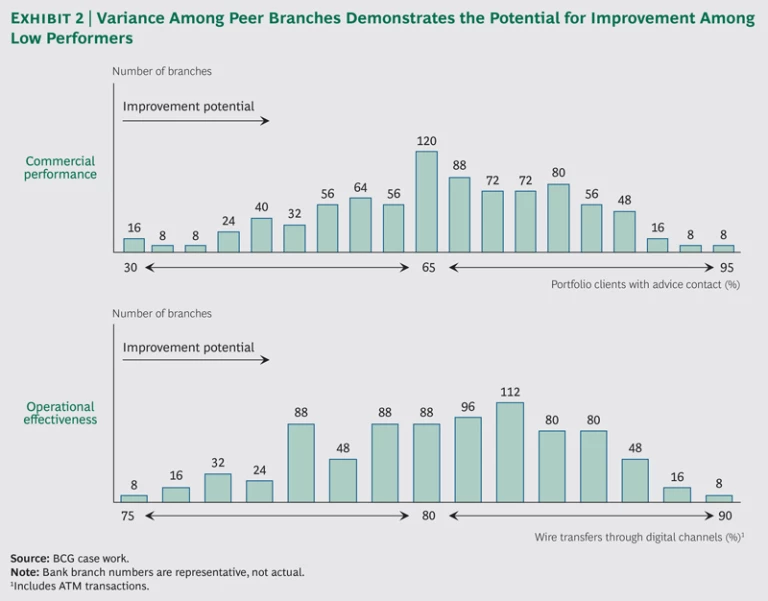

An additional internal benchmarking within a bank’s own network allows us to compare individual branch performance with clusters of comparable peer branches. The high variance in performance among peer branches demonstrates the potential for improvement for low performers. (See Exhibit 2.)

Part of the internal benchmarking involves visiting branches with a view toward understanding the root causes of underperformance. These visits, typically conducted in a sample of 10 to 20 representative branches and lasting about two days each, include interviews with branch management, RMs, and other branch staff. Sales meetings, coaching discussions, and daily and weekly branch meetings are closely observed. Branch processes and behaviors are assessed against a scorecard of best practices. Such visits allow the bank to collect factual information not available at the central level, such as how processes actually work in the field (as opposed to how they are designed).

Develop a target branch model. To make consistent progress on the journey toward true branch excellence, banks need to clearly identify what great performance really looks like, starting with their own specific strengths and addressing their weaknesses. They then need to draw a detailed roadmap for the journey and identify quick wins to build momentum and help fund the program.

Above all, banks need to focus on the specific levers that will genuinely make a difference in the branches. Which levers really contribute to network strategy and to the bottom line? Which are possible to implement in a reasonable time frame? Which are truly under the control of branch management? We have seen leading banks create a formal operational handbook that contains best practices and suggested solutions to problems that frequently crop up. Such banks also develop operational tools that branch management and staff can use to track performance. These tools are particularly effective at raising the performance of third- and fourth-quartile branches.

Choosing which levers should receive the most attention will depend on the bank’s market specifics, starting position, and strategic priorities. Implementation should be intelligent, offering leeway to branches that are already performing well but

providing clear input and guidance to underperforming branches.

Implement commercial and operational improvements. After diagnosing the performance level of the branch network and developing a target branch model, banks must embed the new improvement levers and operating model into the organization. Small-scale pilots should be used to refine the most complex improvement levers. Coherent incentives, key performance indicators, and transparent reporting are essential. A critical element is constructing dashboards to assist branch management in identifying and implementing improvement levers at the individual branch level, applying knowledge gained from the pilots. The dashboard has proved to be an invaluable tool for jump-starting the performance of individual branches.

A further important step is establishing detailed action plans that include sales and profitability goals. None of this, of course, can be accomplished without new training programs that allow local top performers to transfer essential knowledge to rank-and-file branch employees, or without full support at the group level.

What a Best-Practice Network Looks Like

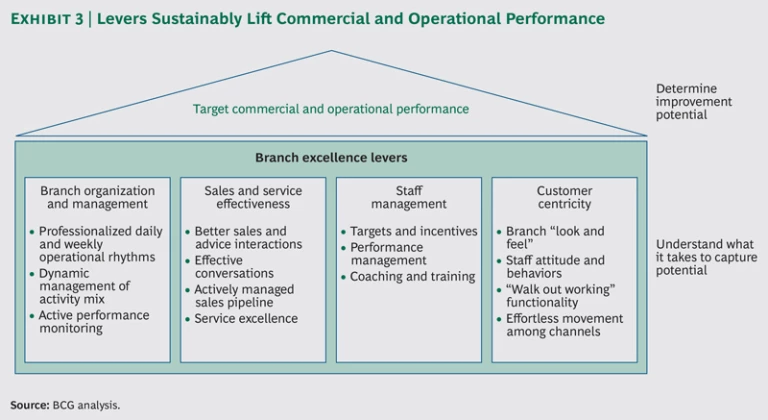

Banks with best-practice networks not only implement a series of critical commercial and operational levers from their branch-excellence programs, but they also work on them holistically to achieve maximum impact. The key categories of levers are branch organization and management; sales and service effectiveness; staff management; and customer centricity. (See Exhibit 3.)

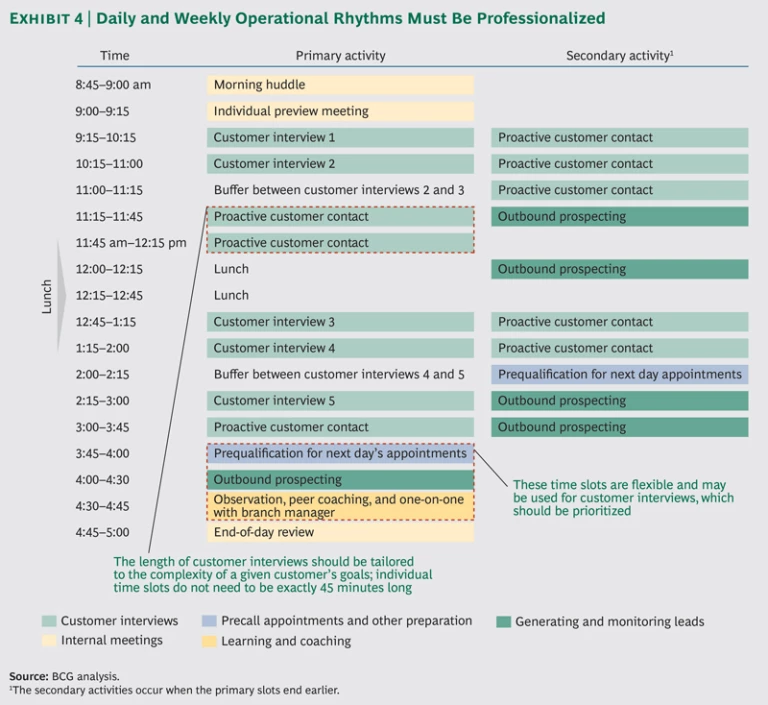

Branch Organization and Management. Best-practice banks professionalize the operational rhythms of their branches by instituting daily staff meetings 15 minutes before opening (the “morning huddle”), systematically reviewing commercial results during weekly meetings, and installing guidelines for spending noncommercial and idle time. (See Exhibit 4.) They also use sharp and focused management information at the regional, area, and branch levels to diagnose the activity mix and improve performance.

Sales and Service Effectiveness. We have seen banks significantly improve the quality of sales and advice interactions by using structured scripts for conversations, conducting holistic customer reviews, limiting interruptions (such as by phone and by colleagues in person) during commercial meetings, actively managing the sales pipeline, and differentiating service levels across customer segments of different value. We have also seen leading banks limit cash handling to select branches only, reduce opening hours at the counter, terminate delivery of debit and credit cards at branches, and stop accepting paper transfers. Such banks have achieved these goals by shifting more and more activities to direct channels, mainly online and mobile.

Staff Management. Targets and incentives must offer mutual benefit for staff members and customers. They should include metrics that go beyond typical financial key performance indicators. For example, it can be highly effective to base some incentives on inputs (such as the number of client appointments) versus outputs (the number of sales resulting from those appointments). In addition, a critical element of achieving excellent results—one that cannot be overemphasized—is the importance of training and coaching. We’ve seen banks where branch managers spend up to 20 percent of their time coaching their employees.

Customer Centricity. Perhaps most important, best-practice banks markedly improve the experience of customers in branches. Top institutions accomplish this by selling to need rather than to target, by codifying the “look and feel” of each branch, and by formalizing and driving optimal staff attitudes and behaviors toward customers. They effectively publicize product promotions and clearly post important information for customers in their branches.

Such banks also achieve end-to-end process effectiveness, demonstrated by shorter cycle times and “walk out working” functionality for major products. They enable seamless multichannel integration that allows customers to move effortlessly among branches, online and mobile channels, and the call center. The change-management skills they show in transforming the behaviors of their staff are transferred to customers through an overall experience that is more efficient and more effective in meeting the customers’ most important banking needs.

Seizing the Moment

Successful branch-excellence programs can bring major improvements to the top and bottom lines, enabling the bank to move into a leadership position in its target markets. For example, one major financial institution with a large retail footprint and a historically high cost-to-income ratio was under severe profitability pressure following the 2008-2009 global financial crisis. The bank ran a branch-excellence project as part of a large-scale transformation program, focusing mainly on reducing costs and FTEs in the network. The project, which is now repeated annually to reinforce best practices, has had the following impressive results (percentages are approximate):

- A 9 percent reduction of network FTEs

- An 8 percent increase in the number of advice contacts per FTE

- A 4 percent increase in the number of appointments per FTE

- A 10 percent increase in the conversion rate of leads

- A 4 to 5 percent improvement in the cost-to-income ratio

Moreover, as we have seen, the current performance level does not limit the potential benefits of a properly conceived and executed program. Even banks whose branches are already humming along at healthy rates of revenues and profitability can experience significant improvement. Nor does the region or type of market matter. We have seen banks in developed and emerging markets all over the world raise their games considerably.

Ultimately, banks should not simply explore how they might go about a rigorous branch excellence program. They should also think about what their competitors are doing with their own branches and then ask themselves a critical question: what are the potential consequences of standing pat and not acting at all?

Acknowledgments

The authors offer special thanks to the following BCG colleagues for their valuable contributions to the conception and development of this report: Sébastien Bard, Gennaro Casale, Fabien Chazal, Audélia Krief, Andy Maguire, Reinhard Messenböck, Michaël Niddam, Sukand Ramachandran, Axel Reinaud, Beatriz Reyero, Rob Sims, Sam Stewart, Steve Thogmartin, Saurabh Tripathi, and Christian Ziegelmayer.