Digital trade, like all trade, enriches nations. We estimate that the extent of this enrichment will amount to $4.2 trillion, or more than 5 percent of GDP, for the G-20 countries in 2016.

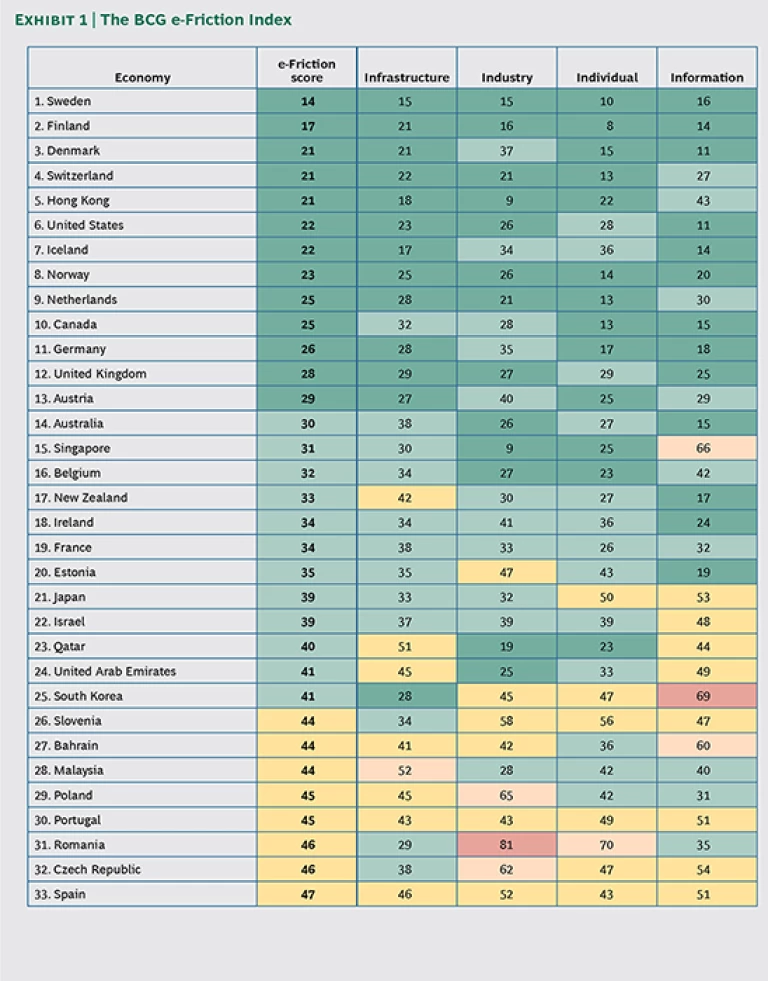

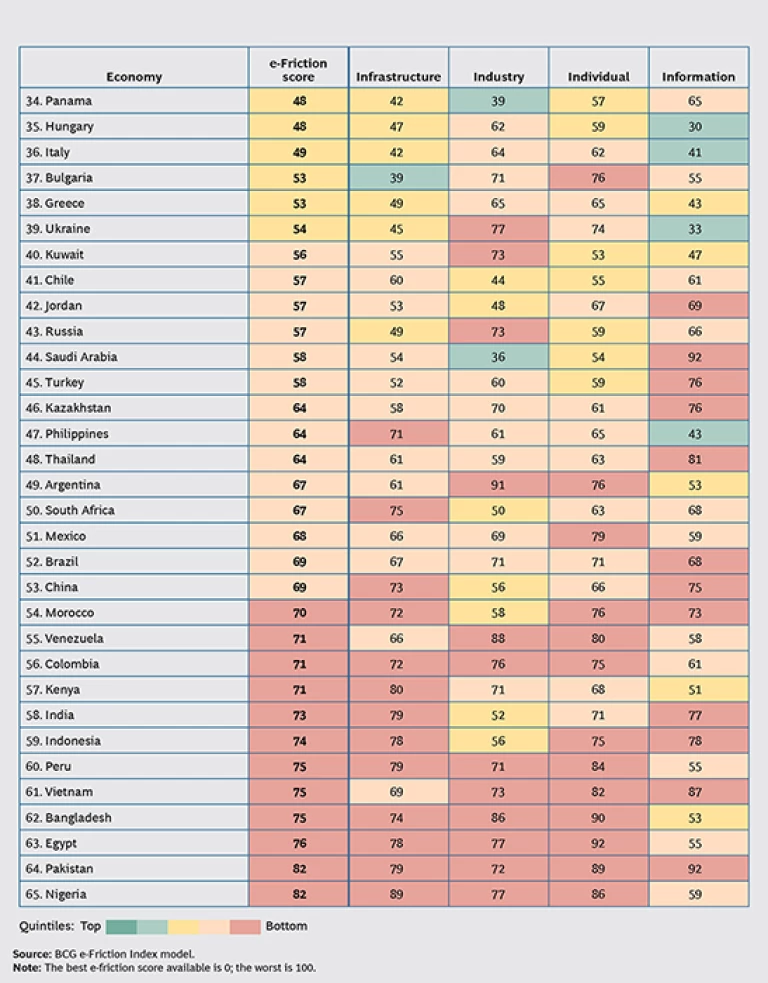

The BCG e-Friction Index

Where is digital trade best positioned to flourish? Where is it inhibited the most? See how 65 economies stack up.

But not all nations engage equally in the exchange of goods, services, ideas, and information—either online or in the physical world—and the economic and social benefits of digital trade are far from evenly distributed. In the most advanced and productive Internet economies, consumers and businesses face few restrictions or constraints on digital activity—what we refer to as “e-friction.” A single set of technical rules and protocols enables anyone who can get online to trade goods, services, ideas, and information with anyone else—anywhere. Few tariffs, taxes, or technology controls (other than limits to access) slow things down. We put the difference between countries with large digital economies and those with low online economic activity at about 2.5 percent of GDP—a material figure for any nation.

| Digital trade will amount to $4.2 trillion, or more than 5 percent of GDP, for the G-20 countries in 2016. |

To make it easier for those with an interest in the health and growth of their online economies to “grease the wheels” by reducing the friction that holds back the development of the Internet economy, this report looks at the major causes of e-friction and at how countries can learn from those that faced similar challenges but have managed to address the most significant impediments. (See “About This Report.”)

About This Report

In our January 2014 report, The Connected World: Greasing the Wheels of the Internet Economy, which was commissioned by the Internet Corporation for Assigned Names and Numbers (ICANN) as was this update, we identified 55 indicators of “e-friction” that inhibit online activity by consumers, businesses, and governments. The BCG e-Friction Index used those indicators to rank 65 economies that are home to more than 80 percent of the world’s population and more than 90 percent of the world’s economic activity. This report updates the index and expands on that analysis, showing economies how they can move up the e-friction ladder.

The Impact of e-Friction

The Boston Consulting Group’s e-Friction Index ranks economies according to four types of friction: infrastructure, industry, individual, and information. (See Exhibit 1.) Infrastructure-related friction, which limits basic access to online activity, is the most significant and accounts for one-half of an economy's total e-friction score. The other three components are equally weighted. Industry-related sources of friction, such as shortages of capital and skilled labor, hold back successful online-business operations and the development of digital businesses. Individual friction—payment systems and data security are two examples—affects the degree to which citizens and consumers engage in online activities. Information-related friction includes the volume of content available in a local language, a country’s commitment to Internet openness, and the obstacles to accessing certain types of content.

Reducing e-friction can have a big impact on national competitiveness as well as on social and economic development. Digital technologies are transforming essential social services, such as education and health care, as well as the ways in which people interact with their governments. The potential for massive improvements in universal utilitarian services, such as transportation and banking, is clear. But billions of people still cannot connect to the Internet. More than 4.5 billion people live in high e-friction economies (those in the fourth and fifth quintiles of our index), including some 3.2 billion people who are not connected to the Internet. (Since most of the economies not covered by the index are likely to have a high degree of e-friction, expanding the index to cover the world would increase these numbers to more than 5.5 billion and 4.2 billion, respectively.) There are about 2 billion people under 19 years of age in the 65 economies. Some 85 percent of them live in economies with the highest levels of e-friction. These young people will be entering—or wanting to enter—the workforce over the next decade or two. Will they have the skills to contribute to and benefit from the Internet economy?

Low e-friction correlates closely with high Internet penetration and strong digital economies. Top-ranking e-friction economies have Internet penetration rates of more than 80 percent, while many low-ranking economies have penetration rates of 50 percent or less. That said, the off-line population in the economies in the top two e-friction quintiles still numbers about 150 million, many of whom are elderly, have a low income, or are unskilled. The U.S. has the developed world’s largest off-line population, accounting for about 40 percent of this figure, or some 60 million people.

Factors Affecting e-Friction

Although the 55 individual e-friction indicators pinpoint the factors that inhibit digital economic activity, five broad causes stand out as major contributors to high e-friction scores and correspondingly to low rankings. Some of these causes can be influenced by policy initiatives in such areas as infrastructure, incentives, taxes, and tariffs; others require more creative approaches.

The first major cause of friction is overall wealth, as measured by GDP. National wealth affects consumers’ ability to make purchases, such as smartphones or other Internet-enabled devices, and the willingness of businesses to invest, such as network operators’ inclination to finance capital-intensive telecom infrastructure. Economies’ e-friction scores tend to improve with increasing wealth: high-income economies (those with a per capita GDP greater than $15,000) mostly have e-friction scores under 50 and fall into the top three quintiles. Middle-income economies (those with a per capita GDP from $4,000 to $15,000) and low-income economies (those with a per capita GDP that is less than $1,000) fall mostly into the fourth and fifth e-friction quintiles.

Wealth is a cause, not a determinant, however. For countries with any given level of GDP, e-friction can vary significantly. Qatar has the highest per capita GDP in the world ($146,000) according to the International Monetary Fund, yet it ranks twenty-third on the BCG e-Friction Index with a score of 40. Finland, twenty-fifth with a per capita GDP of $40,000, ranks number two in e-friction with a score of 17.

The second and third big causes of e-friction—population density and the share of the population living in urban areas—also have a substantial impact on the economics of network infrastructure deployment. Where people live, topography, and the distance from fiber connection points are all huge factors, too. In many larger countries, conditions vary widely. Consider, for instance, the distinctions between the Amazon Basin and the Brazilian Highlands; the topographical diversity of an island archipelago such as Indonesia; or the proximity to undersea fiber-optic cables for people on the coast of Kenya or Nigeria, compared with those in villages 200 to 300 kilometers inland. These factors are big reasons why so many people today have no Internet connection and, when combined with the first factor, are big reasons why emerging markets are home to so many unconnected consumers.

The fourth and fifth causes of e-friction relate to literacy (basic and digital) and English-language skills. Economies with high literacy rates tend to have low e-friction scores. More than 900 million illiterate people live in the economies covered by the index, mostly in the economies with the highest levels of e-friction. Since the majority of these people live in predominantly rural countries, the problem is particularly difficult to address.

One solution is to increase the availability of content in local languages and dialects. This is easier said than done, however. Some of the largest countries covered in our index—India, Indonesia, and Nigeria, for example—have hundreds of languages and dialects. Some 55 percent of all websites today use English, while estimates of the percentage of people speaking English range from 20 to 25 percent of the global population. Approximately 35 percent speak Arabic, Hindi, Mandarin, and Spanish, but these languages are used on less than 10 percent of websites globally. The lack of local content online contributes to a lack of interest on the part of consumers. This is one reason why Internet penetration trails coverage in many countries, especially in emerging markets.

Common Problems, Similar Solutions

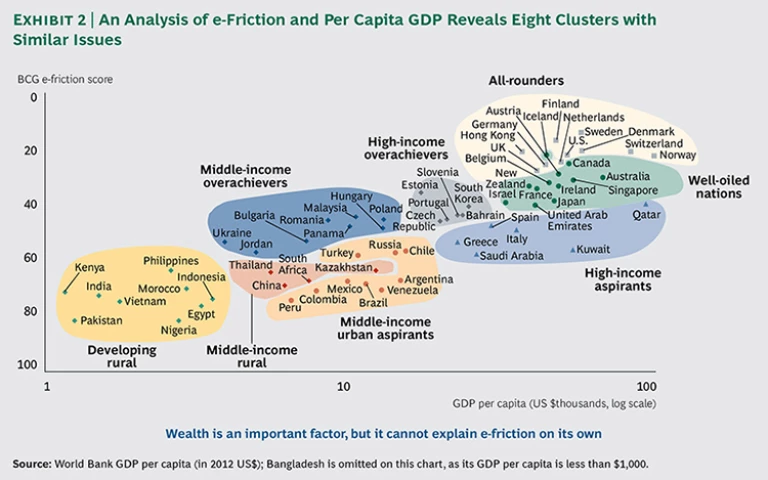

The analysis of economies by their e-friction scores and their per capita GDP points up some interesting—and potentially useful—groupings. Eight clusters emerge, split into three groups by income levels. (See Exhibit 2.) Among high-income economies, “all-rounders” and “well-oiled nations” have generally low e-friction scores, although the well-oiled set performs less consistently across the 55 indicators than the all-rounders do. “High-income overachievers”—mostly small economies such as the Czech Republic, Estonia, and South Korea—excel, owing to successful and focused digital-economy initiatives in areas such as infrastructure deployment and e-government. “High-income aspirants” have a high per capita GDP despite, rather than because of, the level of friction in their digital economies. Their performance across the e-friction metrics is generally moderate to poor.

Among “middle-income overachievers,” economies such as Malaysia outperform on e-friction, while “middle-income rural” economies (Kazakhstan and Thailand, for example) and “middle-income urban aspirants” (such as Brazil, Colombia, and Turkey) face equally big challenges, although of different types. For the first group, the question is how to deploy infrastructure to large rural populations given the economic realities of big capital expenditures, high operating costs, and low average revenues per user. The question for the second and third groups is whether to make the trade-offs between the large urban, unconnected populations and those in rural areas.

Finally, the economies with the lowest GDP per capita and with poor e-friction performance across the board face multiple challenges owing to low income levels, rural populations, and often low literacy rates. The economic and social potential of successfully addressing these challenges is correspondingly large. There are some good examples of success. In Kenya, undersea fiber-optic connections have brought down prices and expanded broadband access. Of the country’s 40 million people, nearly 12 million now use the Internet—three times the number that were online in 2009. Kenya’s fast-growing IT sector, nicknamed Silicon Savannah, accounts for 5 percent of the country’s GDP, and the government has projected the sector to grow and account for 35 percent.

Analyzing and addressing the 55 indicators can help any economy reduce e-friction, increase Internet use, and further digital economic activity. Economies will reap benefits from doing so. But those economies looking to take large leaps would be well advised to address the five major causes of e-friction. Economies should start by prioritizing the relative significance of each cause for their economy and then developing a strategy for each. They should recognize that their strategies may differ from those of other economies, although economies in the same cluster face common challenges and are likely in some, but by no means all, instances to pursue similar solutions.

Developing rural nations, for example, face multiple issues regarding basic infrastructure. The economics of connectivity are determined by a variety of factors, only some of which are related to technology. Governments need to determine the specifics of their broadband-access aspirations and develop a country-specific approach—one that is both technology agnostic and allows for experimentation. Such an approach involves choices and trade-offs, particularly with respect to rural areas. But the general rule should be that faster is better. Countries should aspire to the fastest broadband speeds that technology and economics permit.

A number of emerging markets are experimenting with innovative business models and new forms of funding. The optimal technology depends on local conditions, with a combination of mobile and fixed wireless generally the most cost effective for rural areas and satellite typically the best bet for truly remote areas. A number of companies are experimenting with innovative approaches involving satellites, balloons, and drones. Governments can use tax policy to keep down the cost of mobile device ownership and to promote mobile Internet usage. (See the forthcoming World Economic Forum report produced in conjunction with The Boston Consulting Group, Expanding Participation and Boosting Growth: The Infrastructure Needs of the Digital Economy , March 2015.)

Middle-income economies, particularly those in the rural and urban-aspirant clusters, may benefit substantially from efforts to demonstrate to their populations the value of the Internet and bring more people online. There are good models to follow in four key areas: furthering the development of local content, building digital literacy, simplifying access and use, and bringing down cost. Governments, network operators, and content providers can also help overcome barriers to adoption by reaching out directly to women and other underserved groups. Initiatives that bring more businesses online by reducing red tape and taxes and tariffs on digital equipment, or that further education and training in information and communications technology, can have a big, long-term impact.

Many countries can benefit particularly from efforts to develop local content, and governments can play a big role. Governments can help further digital engagement with their own online services. BCG’s research of 12 countries in 2014 found that 94 percent of Internet users have accessed at least one government service online in the past two years and that an average of 32 percent use online government services more than once a week. People in developing countries are especially heavy users of services that have a significant impact on life and livelihood, such as those related to health care and education.

The private sector can help, too. A number of companies have boosted usage with programs to develop ecosystems of local content. Network operators can simplify pricing by offering “data packs” organized around access to information on popular pastimes—such as sports and movies, as well as social networking and video apps—instead of megabyte- or gigabyte-based data plans. Network operators can help support the development of local content and apps by handling administrative functions, such as billing, and by providing cloud-based services to developers (who often are sole entrepreneurs or have a small business).

Economies in the all-rounder and well-oiled categories should not rest on their laurels. Even the all-rounders face thorny digital issues, such as privacy and data security, that clumsily handled or left unresolved can throw sand in the gears. Well-oiled economies have more sources of friction to address, such as those related to outdated regulation, excessive bureaucracy, and impediments to investment; these economies need to focus their interventions with care.

BCG’s research has shown repeatedly that small and medium-sized enterprises (SMEs) benefit enormously from the adoption and use of Internet and online tools, especially in terms of revenue growth. The Internet helps SMEs both sell and buy goods and services more widely, furthering SMEs’ integration into their national economy and the global economy. When compared with SMEs that are medium or light Web users, SMEs that are heavy Web users are almost 50 percent more likely to sell products and services outside their immediate region and 63 percent more likely to source products and services from farther afield. However, SMEs too often encounter various types of friction that slow or prevent them from fully exploiting the Internet’s potential, and SMEs in high-friction economies generally lag behind SMEs in low-friction economies in the level of Internet adoption and use.

Today, world trade represents about 30 percent of global GDP, which is an increase of 20 percent since the early days of the Internet and three times the level of 50 years ago. The experience of small businesses seeking to do more online illustrates how the Internet is shaping the future of world trade and contributing to its growth.

No country or economy can stand still. The global digital ecosystem is evolving at a breakneck pace, and national competitiveness will increasingly depend on the health and strength of a country’s Internet economy. Those that act decisively now to identify their major causes of e-friction and address the impact have the opportunity to generate higher economic growth, develop stronger trade balances, and create more jobs.

Acknowledgments

This report would not have been possible without the efforts of BCG colleagues Lauren Daum, Nicolas Naranjo, and Camila Penazzo. In addition, the authors are indebted to Wolfgang Bock, Philip Evans, Patrick Forth, and numerous other colleagues and external experts for their support and guidance.