It’s easy to create value in an expanding economy with strong tailwinds. However, steering a company through an economic crisis is far more difficult. Recently, one of the longest, toughest periods in Brazil’s history produced critical challenges for both local companies and multinationals operating in the country. Some organizations thrived nevertheless, offering lessons on succeeding amid uncertainty.

Over the past two decades, the Brazilian economy has been more volatile and slower to grow than at any point in the past century. The most recent crisis, from 2014 to 2018, was particularly difficult, and the recovery since then has been sluggish. Given such an environment, many companies may be tempted to hunker down and wait it out. Others, however, will take action in order to emerge from tough conditions even stronger than they were before, with better prospects for growth and an increased ability to create value for shareholders and other stakeholders. BCG research has identified specific ways to find Advantage in Adversity: Winning the Next Downturn .

Using the analysis from that research, we recently looked at more than 100 publicly traded companies in Brazil. The goal was to identify those that were underperforming before the start of the country’s most recent economic crisis but able to dramatically turn around their performance when the crisis hit. These organizations didn’t just ride out the storm or use it as an excuse for lagging their peers; they seized the initiative and took bold steps to improve. In particular, our research identified five characteristics common to these organizations:

- Obsessive focus on efficiency

- Growth orientation

- A formal transformation program

- Early and decisive action

- Excellence in execution

These are critical measures for companies looking to capitalize on a crisis and turn around their performance.

The New Normal: Uncertainty

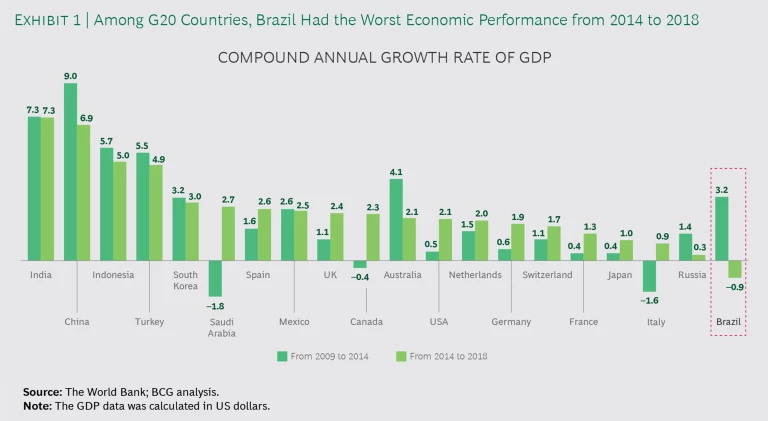

Even when compared with other developing markets, Brazil’s economic environment remains challenging for companies. From 2009 through 2013, the country rebounded strongly from the global financial crisis, only to hit an additional set of problems that were more localized. Several financial challenges led to the biggest one-year decline in GDP in a hundred years. From 2014 to 2018, Brazil posted the worst economic performance of any G20 country. (See Exhibit 1.) The depression was particularly severe, with a steep drop in retail sales, increased corporate leverage, and high unemployment.

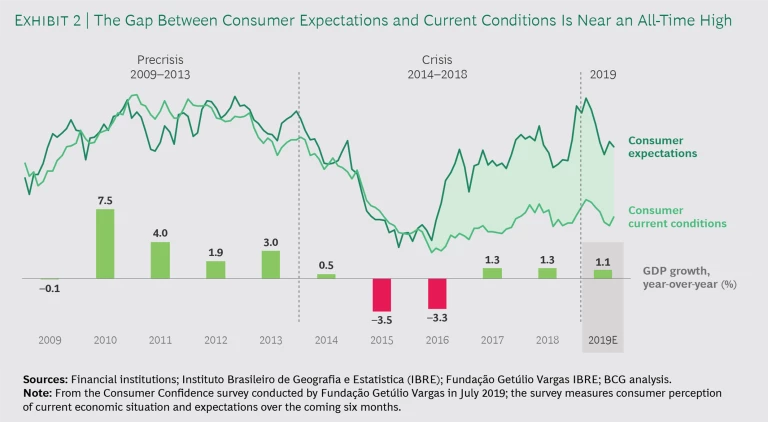

Since the beginning of 2017, however, the country’s economy has bottomed out and begun to recover—but only slightly. Brazil’s per-capita GDP remains roughly at 2012 levels, resulting in stagnated living standards (in sharp contrast with those of other developing economies). Furthermore, current projections indicate that the country’s GDP won’t return to prerecession levels for at least another four years—a far longer recovery period than most had anticipated. And although consumers’ current financial situations are unstable, there is a huge gap between consumers’ expectations and current consumer conditions. (See Exhibit 2.)

In all, these conditions point to a period of volatility with fewer catalysts for growth. Management teams that accept these conditions and understand the steps required to capitalize on the current adversity can gain a significant advantage. The question is how.

Management teams that understand the steps required to capitalize on the current adversity can gain a significant advantage.

Identifying the Turnaround Experts

Our analysis included 110 companies, all with revenues and market caps of more than R$1 billion (about US$230 million as of early February 2020), which constituted approximately 80% of the total market cap on Brazil’s B3 stock exchange.

Most sectors posted a decline in TSR performance during the recent crisis in Brazil. The biggest contributing factors were a drop in revenue growth and lower valuation multiples, reflecting lower investor expectations.

However, a subset of companies in our analysis thrived during the crisis, actually improving their TSR performance. They went from lagging the overall average TSR to exceeding it, essentially using economic adversity to make needed upgrades to their business models, operations, and financial positions, among other things. This group of companies returned 32% average annual TSR during the four years of the crisis, significantly outperforming the rest of the companies we examined, through a combination of faster growth and dramatically improved margins. We call these companies turnaround experts.

Turnaround experts used economic adversity to make needed upgrades to their business models, operations, and financial positions.

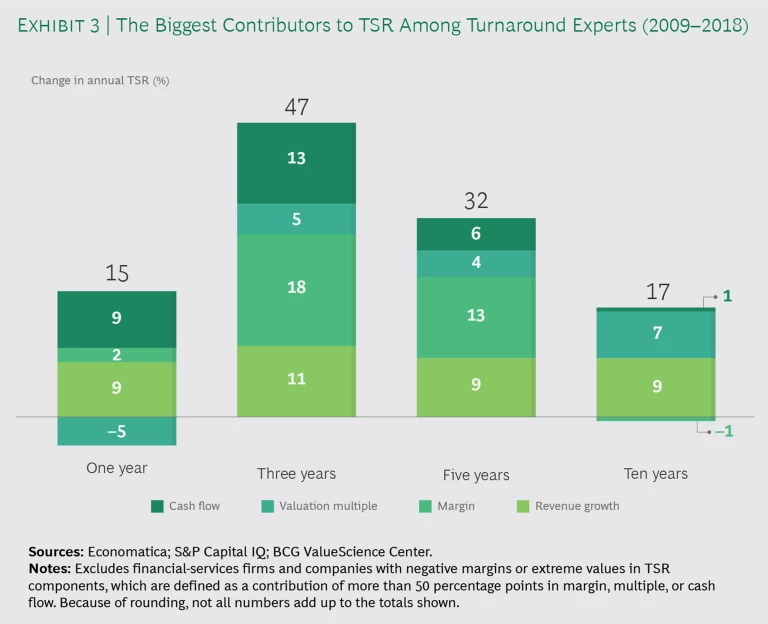

One other aspect of the TSR analysis worth noting is that the key contributors to strong performance for turnaround experts change over time. (See Exhibit 3.) In the short term, changes to cash flow can have a disproportionate effect upon TSR; margin improvements are the biggest contributor in the medium term (within the three-year and five-year marks); and increased revenue and multiples produce long-term, sustainable TSR over ten years.

Finding Advantage in Adversity

Let’s take a closer look at the five traits these successful companies share.

Obsessive Focus on Efficiency. The turnaround experts in our analysis were far more relentless about improving efficiency than the other companies in our sample, taking active measures throughout the crisis to reduce costs. More than half of the companies in the group reduced selling, general, and accounting expenses as a share of revenue by at least 5 percentage points, and many notched even greater gains.

Growth Orientation. These companies did not try to cut their way to success. Instead, they maintained a growth orientation despite major uncertainty. Collectively, they posted a compound annual growth rate of more than 10% from 2014 to 2018—performance that would be impressive even in a nonrecessionary economy. (By comparison, the underperforming companies in our study grew at a compound annual growth rate of 6.5% over the same time period.) Some achieved this growth through M&A; others grew organically, often by rolling out new products and services. Yet virtually all these companies created value in the early years of the turnaround through margin improvements and in the longer term through revenue growth.

A Formal Transformation Program. Turnaround experts did not try to make ad hoc structural adjustments. Instead, the vast majority (80%) launched a formal transformation program—announced publicly in company filings—that typically centered on the goals of restructuring operations, streamlining balance sheets, reducing employee headcounts, and cutting costs. In the underperforming group, by comparison, only about two in every five companies announced a transformation program.

Formal programs are critical for turnaround success because they lay out explicit goals for the company and allow management to prioritize measures that will deliver larger benefits early on—potentially freeing up capital and resources in the early stages to fund subsequent aspects of the journey, such as revenue growth. Formal transformation programs also help management think through the interdependencies of various pieces of the program. Crucially, they create transparency both for internal stakeholders (such as employees and managers) and external stakeholders (for example, investors, suppliers, and partners) as well. Communication and transparency can help align expectations and generate buy-in to achieve a common goal, increasing the odds that the transformation will succeed.

Early and Decisive Action. Related to the idea of a formal transformation program is the timing of the launch of such an initiative. Rather than waiting and hoping for conditions to improve, roughly two-thirds of the turnaround experts in our sample took early and decisive action, launching their initiatives in the early stages of the crisis—or, in some cases, even before it hit. In contrast, the rest of the companies we reviewed were more likely to wait until 2016 or 2017, when the situation had already worsened substantially.

Excellence in Execution. The turnaround experts in our sample were highly disciplined about sticking to the initiatives they established early on. Transformation programs can often be years long, and companies can get thrown off course by such developments as new objectives, distractions, or a change in management. By crafting a careful plan and rigorously sticking to it—through KPIs, clear milestones, and a link between specific actions and value creation—turnaround experts generated better outcomes in the long term.

How Two Companies Put These Principles to Work

Among the turnaround experts in Brazil that we identified, two organizations warrant a closer look.

Grupo Fleury. This company conducts diagnostic tests for the health care industry. Grupo Fleury had been on an aggressive M&A-driven expansion before the crisis, spending about R$1.3 billion on competing labs and other assets from 2009 through 2012. In 2012, Grupo Fleury also launched a new brand, called a+, which allowed the company to capture volume at a lower price point and continue to grow during the crisis. Together, those actions helped Fleury double its size from 2010 through 2012. However, the rapid growth also led to inefficiencies, higher operating costs, and shrinking margins. The company’s market cap fell in response, shedding R$600 million by 2013. Although the company was not in distress at the time, management recognized that there was room to improve performance.

Also that year—before the crisis had even started—the company announced a formal turnaround plan, initially focused on streamlining the portfolio and reducing headcount. During the subsequent 12 months, the company trimmed the workforce by roughly 9% and decreased the number of business units by 16%, in order to simplify the organizational structure. In 2014, a new CEO took over—Carlos Marinelli, who had been at the company since 2005. He redoubled the company’s efforts to reduce costs and boost efficiencies.

Marinelli identified three factors that were key to the turnaround:

- Maintaining strict quality and service levels for customers

- Setting specific KPIs and targets to quantify gains

- Engaging the workforce in the transformation

Because Grupo Fleury had grown through M&A, it needed to take into account regional differences in the organization while still transforming the overall culture. The company also adopted a much more analytical approach to management, including new tools to oversee processes and people and to better control costs and revenues.

By 2017, the turnaround effort had begun to generate results. Operating expenses had declined from 91% of revenue to 81%. Redesigning processes such as procurement and receivables led to a major drop in working-capital requirements. In the product portfolio, Fleury repositioned several of its brands to focus on higher-margin testing segments while sustaining its emphasis on innovation and solidly reliable quality of its testing services.

By mid-2019, those measures had delivered dramatic improvements along several measures:

- Revenue—a compound annual growth rate of roughly 11%

- Earnings before interest, taxes, depreciation, and amortization (EBITDA) margins—up 5 percentage points, to 24%

- Return on invested capital—nearly doubling from 8% to 14%

- Market cap—nearly tripling, from R$2.5 billion in 2015 to R$6.7 billion

Gol Airlines. In less than five years, Gol Airlines, the low-cost carrier with the leading market share in its home market of Brazil, faced two successive crises and emerged from both even stronger than it had been before. It has been on a turnaround journey marked by a balanced focus on the top line, costs, efficiency, and the balance sheet. The airline business is challenging in any market because of high external costs that lie outside management’s control, but it’s particularly hard in Brazil, where those costs largely accrue in foreign currencies, while revenue is tied to the country’s more volatile currency, the real.

The first crisis, in 2011, was an industry-specific contraction. In the wake of the global recession of 2008, travel demand among consumers in Brazil was low. Rising oil prices compounded the pain, pushing Gol into negative margins.

In 2012, a new governance structure was put in place, and it launched a plan to restructure operations and restore the carrier to profitability. The company reduced capacity, adjusted the route network, improved customer service, and increased its focus on the corporate segment. It also cut the workforce by 14%. And it spun off its loyalty business, unlocking value and creating liquidity through an IPO—a major step to strengthen its balance sheet.

Just as those measures were generating results, the broader economic crisis in the country hit. As the US dollar strengthened against the Brazilian real in 2015, the company’s debt burden increased by nearly 50%, and consumer demand for plane tickets decreased as a result of the stagnant Brazilian economy. By early 2016, the company was again facing headwinds, and management launched a renewed effort to reduce leverage and strengthen the balance sheet. Gol returned some planes, canceled new orders, and negotiated flexible contracts with OEMs. The carrier also restructured much of its debt. Such measures funded the transformation journey over the subsequent years.

Throughout this journey, Gol continued investing in measures to boost revenue and strengthen its strategic positioning in the market. For example, the company has consistently invested in revenue management capabilities to increase yields. It has also focused on improving the customer experience in areas such as online ticketing, in-flight WiFi, extra leg room, and entertainment—all key means of making Gol more attractive to the corporate market segment. Another key area of overinvestment has been the strengthening of its international business, by both increasing its footprint of international flights and strengthening its partnership with international carriers, including Air France and KLM. (Both are now shareholders of Gol.)

Collectively, the proactive turnaround measures led to a dramatic improvement in Gol’s financials and competitive positioning. From 2013 to the second quarter of 2019, passenger revenue divided by available seat kilometers grew by an average annual rate of 9%, and EBITDA margins more than doubled, from 9.2% to 25.9%. Leverage, measured by net debt as a percentage of EBITDA, was reduced by 60%. Gol became the number-one Brazilian player in 2016 and maintained that position in 2019 with a 38% share of the Brazilian market. It also claimed the dominant share of the corporate segment and substantially increased revenue from international flights and connecting passengers from partner airlines. Those gains were rewarded by investors, who bid the company’s market cap from R$2.9 billion to R$11.4 billion during that period, helping generate an annual TSR of 22.1%.

Companies sometimes point to economic uncertainty as an excuse for their poor performance. We believe that, with the right perspective, it can be an opportunity instead. The turnaround experts we identified all faced extremely dim prospects due to challenging conditions in Brazil. However, they took the steps needed to dramatically improve performance. They did so by maintaining a clear focus on value creation and by simultaneously searching for growth and efficiency in a structured and sustained way. Brazilian companies and multinationals operating in the country should follow the example set by these successful organizations.

BCG TURN

is a special unit of BCG that helps CEOs and business leaders deliver rapid, visible, and sustainable step-change improvement in business performance while strengthening their organizations and positioning them to win in the years ahead. BCG TURN helps organizations change their trajectories by turning their upside potential into radical performance gains. The BCG TURN team consists of transformation practitioners and battle-tested experts with a proven track record in large-scale transformation. BCG TURN is invested in the sustainable success of clients, with a focus on performance acceleration and a commitment to value delivered.