The surging popularity of streaming services, gaming, and digital and social media over the past two years added to the industry’s substantial shareholder returns.

The past two years gave media companies a big boost. As the pandemic shut down in-person events, people flocked to screens, bolstering subscription streaming services, gaming platforms, and digital and social media . Many stayed put even after social and entertainment outlets started to reopen. The upsurge in subscribers, viewers, and gamers, along with the related bump in online advertising, buoyed media companies’ performance and added to the already substantial market value of numerous media players.

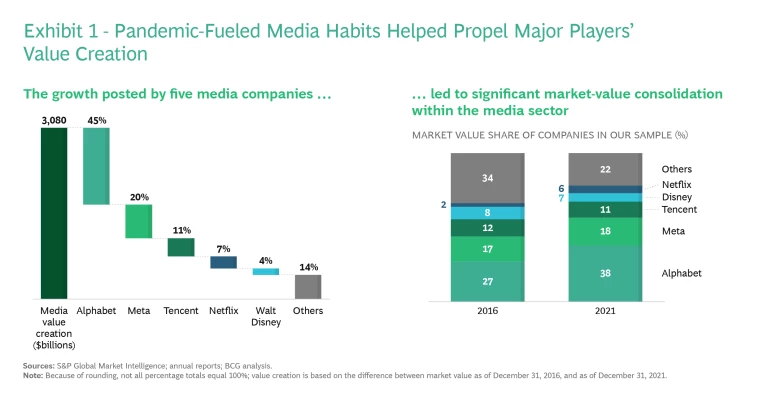

Our analysis of the media industry for BCG’s 2022 Value Creators rankings shows just how well the industry performed. From 2016 to 2021, the combined market value of the 63 media companies in our sample more than doubled, to $5 trillion. A significant portion (60%) of the increase in valuation came during the peak of the COVID-19 pandemic, the 21-month period from March 2020 to November 2021. Five media giants—Alphabet, Meta, Tencent, Walt Disney, and Netflix—accounted for more than 85% of the shareholder value that the industry added during that time.

Continuing to create value once the pandemic subsides isn’t a given. That hit home in early 2022, when equity markets turned volatile on investor anxieties about inflation, monetary policy, and moderating earnings growth. Adding to the turbulence was anxiety over some media players’ investments in the budding metaverse market, and over how much time may elapse before those investments begin to pay off.

Media companies need to take multiple steps to address investors’ concerns and to set themselves up for future growth and returns. For one, they have to navigate intensifying competition for subscribers and users, which has kicked off consolidation within industry segments, as evidenced by ongoing

mergers and acquisitions

in the video game and publishing market segments. They also have to cater to the diverging preferences of some consumers who are eager to get back to attending live events and other consumers who will continue to avoid in-person entertainment for the foreseeable future. Yet another consideration is how to participate in the burgeoning creator economy. Finally, media companies should decide whether to pursue opportunities in the emerging metaverse market, and if so, what approach works best for their business and investors.

Top Media Companies for TSR

Media players large and small profited from trends fueled by the pandemic. Growth of streaming services, for example, helped boost large media players’ valuations and accelerated the consolidation of overall industry value during the five-year period we analyzed. (See Exhibit 1.) From 2016 to 2021, the share of total market value of the five media giants in our sample grew from 66% to 78%.

Big media players also outperformed the overall industry in total shareholder return (TSR). In our latest analysis, Alphabet, Meta, Tencent, Walt Disney, and Netflix had an annualized median TSR of 29%, compared with a median TSR of 14% for all of the media companies in our sample.

But media giants weren’t the only ones that created value. Higher revenues from subscriptions, user fees, and advertising propelled the fortunes of many other media companies.

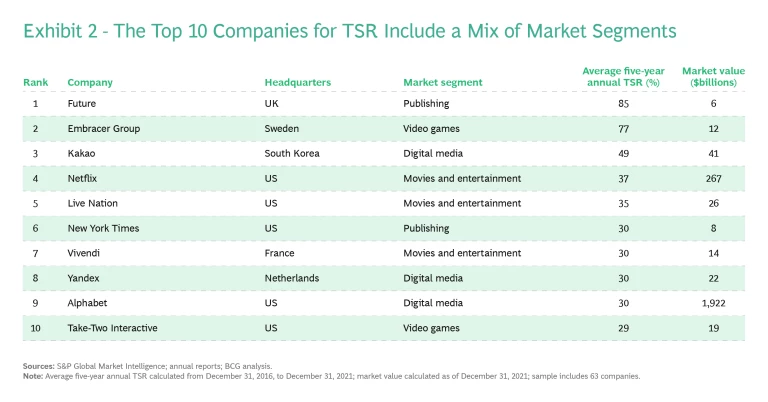

Future was one. The company, a global digital platform for specialist media, saw its e-commerce revenue jump 36% last year thanks in part to investments in proprietary technology and an acquisition spree, which contributed to its annualized TSR of 85%. That figure put it at the head of our list of top media players for TSR. (See Exhibit 2.)

Live Nation was another top performer for TSR. The concert and live events promoter benefited from a trend among people who are eager to go back to concerts and other live entertainment to buy tickets for future performances. A full concert slate for 2022 and beyond helped push the company’s average annual TSR to 35%.

Video game makers Embracer Group and Take-Two Interactive also earned places in the top 10 for TSR. They are representative of the wave of consolidation sweeping through the video-game industry and of companies that are setting themselves up to compete in the metaverse market.

Half of the top 10 media companies for TSR performance are appearing on the list for the first time. One is Kakao, the South Korean digital media company that parlayed a popular messaging app into a digital media ecosystem. It continues to expand through mergers and acquisitions, and is now reorganizing operations to focus on metaverse market opportunities. The company’s five-year annual average TSR of 49% landed it in the number three spot in our ranking.

In 2021, Vivendi spun off its largest business, Universal Music Group, in the latest in a series of asset sales it has undertaken since an activist investor bought a stake in the French media conglomerate a decade ago. The company—which retains interests in TV, advertising, and publishing properties—saw its average annual TSR jump to 30%, pushing it from 45th on our 2020 list to number seven this year.

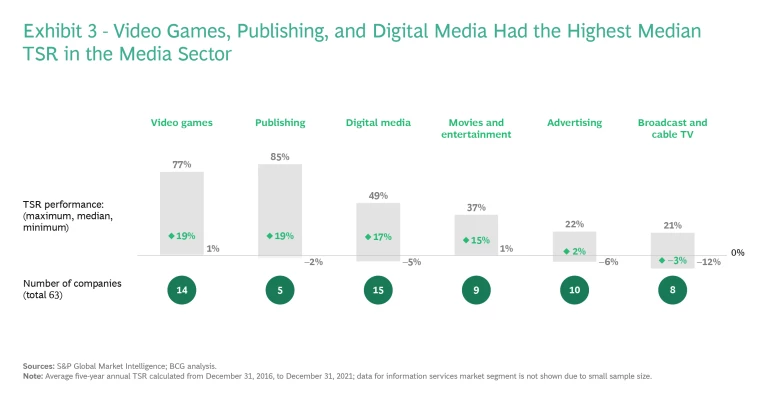

Pandemic-era entertainment preferences had the biggest impact on value creation in the video game, publishing, digital media, and entertainment market segments. (See Exhibit 3). Companies in the video game segment of our sample such as Embracer and Take-Two recorded a median annualized TSR of 19%. Global video-game revenue surpassed global revenue for both movies and music, supported by the popularity of top gaming titles and a growing number of players who now use gaming platforms as de facto social-media channels to chat and hang out with friends.

The 19% median TSR performance for publishing companies in our sample reflects higher growth of digital subscriptions for companies such as Future and the New York Times; the latter recently reached 10 million subscribers to its various media properties. The uptick in digital-media companies’ users led to higher ad revenue and, ultimately, higher growth, as evidenced by that subsector’s median TSR of 17%. And movie and entertainment companies benefited from growth of streaming services during pandemic-era lockdowns to post a median TSR of 15%.

How Media Companies Can Create Value in the Future

To continue to create value in the future, the media industry must appeal both to consumers who are eager to resume going to movies, plays, concerts, and other live events, and to those who are more risk-averse and will continue to avoid in-person entertainment for the foreseeable future. If media companies haven’t already, they must also develop a strategy to support the budding creator economy, and determine how best to compete in the developing metaverse market, which by some estimates could reach $1 trillion by 2030.

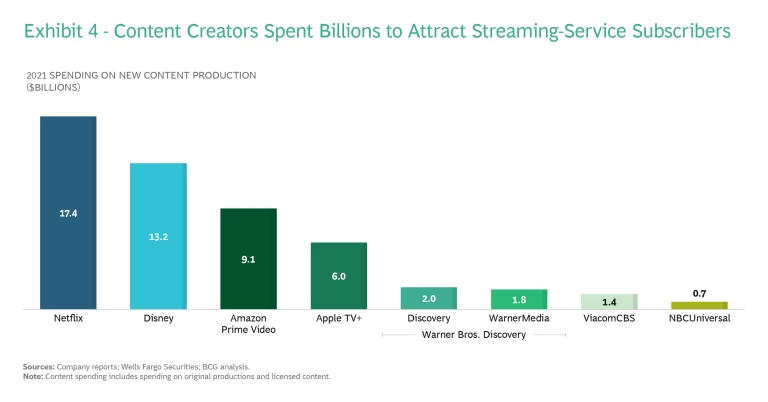

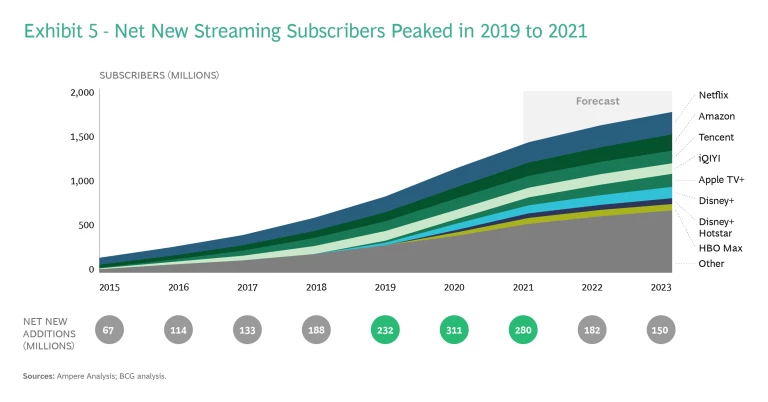

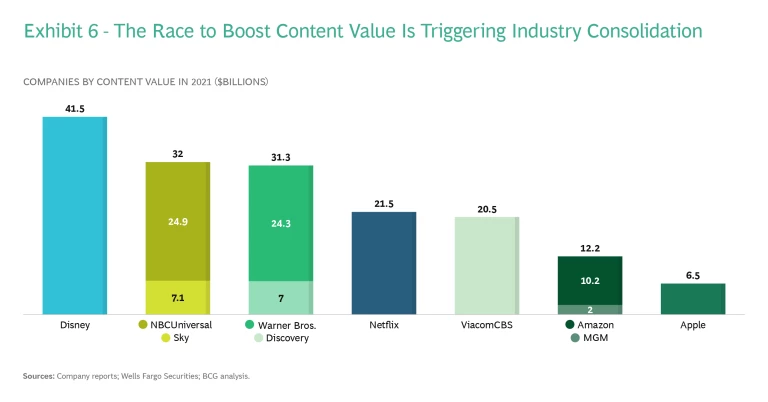

Spend on content. Consumers’ seemingly insatiable desire for new things to watch or interact with led media companies to invest billions in content development, with Netflix, Disney, Amazon, and Apple TV alone spending close to $46 billion last year. (See Exhibit 4.) According to BCG research, about 72% of consumers expect to spend at least as much time watching streaming content once the pandemic era is over as they did during the crisis. But attracting and retaining streaming-services customers could prove difficult. (See Exhibit 5.) Media platforms will likely need to continue spending on content and look for ways to diversify their offerings—ambitions that are triggering consolidation in the industry. (See Exhibit 6.) Investing in audio content such as podcasts is one area that shows promise for growth.

Dive into the creator economy. In the future, media companies will of course need to continue to create new content, experiences, and environments. But they will also need to go a step further and help audiences become content creators—and then share the revenue that flows from that content with those users. Companies such as Roblox are already seeing the benefits of that business model. Gamers on the company’s video game platform earn in-game currency by building games that others can play. By combining gaming and a social network, the company attracts 200 million players a month, making it the most popular gaming platform in the US and Europe.

Craft a metaverse strategy. Many see the metaverse—a virtual interconnected reality seamlessly woven into our physical world—as the next iteration of the internet. Media leaders are making investments to establish themselves; Meta alone spent $10 billion on its metaverse business in 2021. With COVID-19 cementing consumers’ willingness to spend time and money on virtual experiences, companies should consider their plans for participating in the metaverse ecosystem. Video game companies can use their expertise to develop robust VR and AR hardware and infrastructures, and then build on their established user base to expand the content they offer. Media companies are in the best position to produce metaverse content, including VR- and AR-based immersive experiences.

Have a clear mergers-and-acquisitions game plan. As media players look for additional ways to add value, we expect to see more consolidation through M&A. That’s already happening in the gaming sector of the business, where players such as Microsoft, Sony, and Take-Two have acquired well-known game properties to bulk up their pipeline of future titles and presumably to strategically position themselves for a metaverse-focused future. Companies need to be clear on what their strategy is, including determining what acquisition targets would create value and how to realize the greatest potential value from an acquisition or merger.

Use customization and personalization to appeal to customer segments. To provide services capable of turning the broadest range of people into long-term customers, companies must increase their investments in artificial intelligence and other technologies to customize the customer experience . Companies such as Netflix that have first-party data collection capabilities—collecting user data directly from customers—can capitalize on that to offer additional personalization , a practice that companies now reliant on third-party data collection methods should consider following.

Media industry valuations benefited from the tumult of the past few years, but the drop in equity markets in early 2022 shows that what created value in the past might not be what works in the future. As the world reopens, companies will have to use content and a superior customer experience to appeal to people who are hungry to return to in-person experiences as well as to those who are happy to stick with recently acquired viewing, gaming, and online reading habits. And companies have to position themselves to take full advantage of the opportunity presented by the metaverse market while minimizing the financial risks associated with it.