The past few decades presented an outstanding market environment for the asset management industry . Global assets under management (AuM) rose at a generally steady pace between 2001 and 2021, thanks largely to the strength of the world’s equity markets, which were able to rebound even after several severe downturns. And 2021 was even stronger. Global AuM grew at 12% last year, to more than $112 trillion, a growth rate well above the 7% average of the previous 20 years. Net flow rates were also higher than average in 2021, reaching 4.4% of total AuM, or $4.4 trillion, at the beginning of the year.

In BCG’s 20th annual report on the global asset management industry, we offer a retrospective analysis of the effects of this strong market—and as the industry enters a more uncertain era, we look ahead to the expected impact of new technologies such as direct indexing, increasing investor demand for alternative products, and a focus on decarbonization.

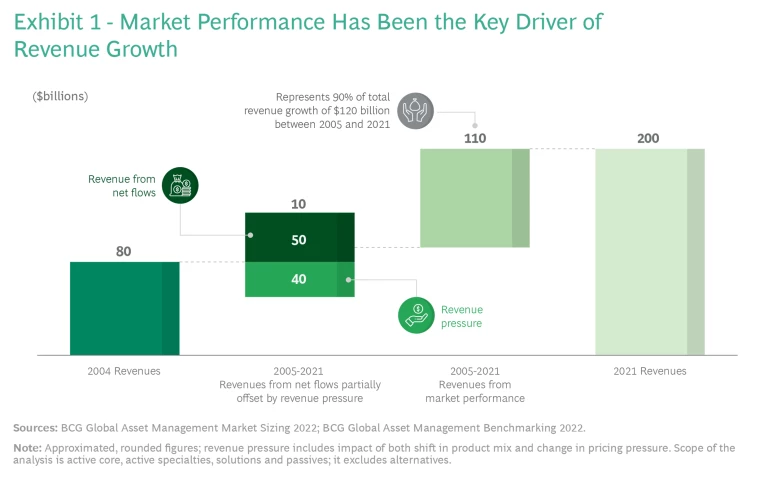

Strong performance in equity markets has been the key driver of growth, representing 90% of the revenue growth between 2005 and 2021. During the same period, revenues from net flows have been almost fully offset by revenue pressures as investors change their asset-class mix toward lower priced products and fee pressure continues. Despite rising costs, operating profit margin rose to a healthy 38% in 2021, up from 36% a year earlier, as average AuM growth outpaced the increase in costs. (See Exhibit 1.)

One of the most conspicuous implications of the long period of asset appreciation has been that the majority of global AuM in mutual funds and ETFs sits in legacy products. As such, it has been very difficult for new funds to stand out. Actively managed products as an overall category have been hard pressed to beat overall market performance; many investors have gravitated to passively managed products that can capture market returns with lower fees or to alternative assets, which offer large illiquidity premiums in return for long lock-in periods and complex deals.

The passive space has become increasingly concentrated, however, with almost 75% of all new capital over the past 5 to 10 years flowing to the top 10 global players—compared to around a quarter of positive net new inflows in the active market. As a result, the active market is currently offering players more opportunities to differentiate.

There is plenty of room in the industry for skill and talent in active management.

Yet our research finds that demand for active managers that can deliver top returns over the long term has not wavered; we found that winners in active products provide not just strong performance but also value for money. There is plenty of room in the industry for skill and talent in active management—especially considering that the active space still represents 77% of the asset management market.

As market dynamics change, asset managers will need to apply those skills and talents to deliver returns. The firms likely to be the winners of the future are those that can adapt to new ways of thinking and new approaches to the competitive marketplace. New technologies, notably direct indexing, are effectively democratizing the ability to personalize products for the end investor. This trend presents a challenge, but asset managers can overcome it if they identify new ways to differentiate themselves.

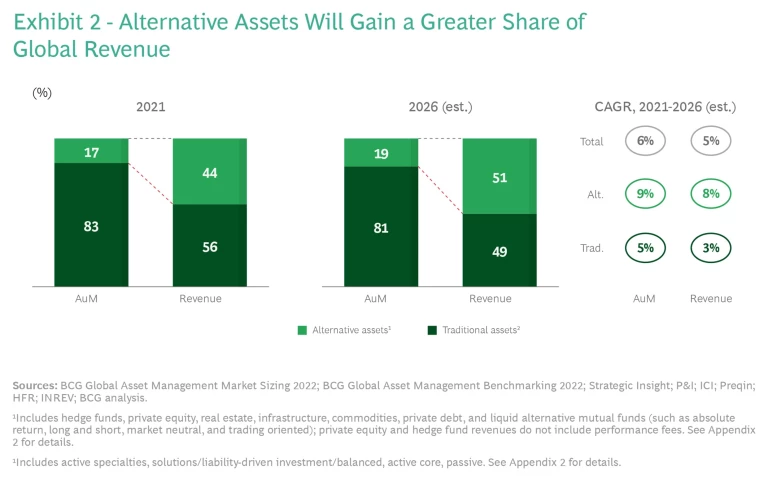

Rising investor interest in alternatives means that asset managers will need to build the capabilities for investing in these assets and distributing them to retail investors. We expect to see alternatives grow to more than half of all global revenues over the next five years. (See Exhibit 2.)

In addition, the global push to achieve net-zero carbon emissions by 2050 is both mission critical for the planet and presents a great many opportunities to develop portfolios that support sustainable practices. The sustainable investing market could translate to $20 to $30 trillion in bond and equity allocations over the next 30 years, with much of this capital frontloaded over the next several years so that it can be invested in long-term climate transition projects.

Subscribe to our Financial Institutions E-Alert.

The tailwinds that helped the asset management industry reach such impressive heights in recent decades are shifting. But while a certain degree of turbulence lies ahead, the future also presents multiple opportunities and a range of ways to win.