Emerging technologies are reshaping the world at an accelerating pace. As the GCC races ahead with its ambitious economic development plans, the region has already well progressed on its technology infrastructure and has provided many needed legislative, investment, and entrepreneurial environments for digital-first leading organizations to emerge within the region.

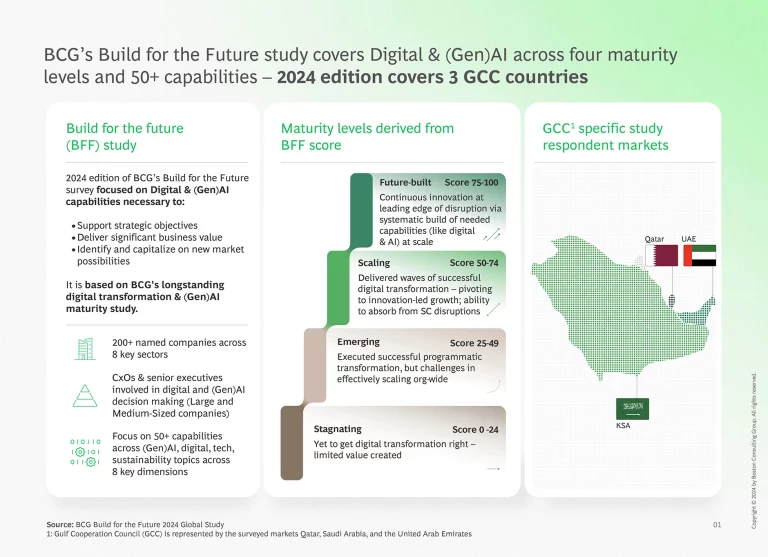

To gauge this digital and AI readiness, BCG’s 2024 Build for the Future (BFF) study examined the digital maturity of organizations in the GCC with a special focus on AI as a most transformative emerging technology. The study surveyed C-suite executives and senior leaders from 200+ organizations across eight sectors in Qatar, Saudi Arabia, and the United Arab Emirates.

Upon evaluating organizations across 53 core capabilities pertaining to digital maturity and AI readiness, the BFF study methodology categorizes each surveyed organization into one of four categories representing their stage of digital transformation, from least to most mature: Stagnating, Emerging, Scaling, and Future-Built.

Core Capabilities: GCC Organizations to Catchup with Global Digital and AI Maturity Levels

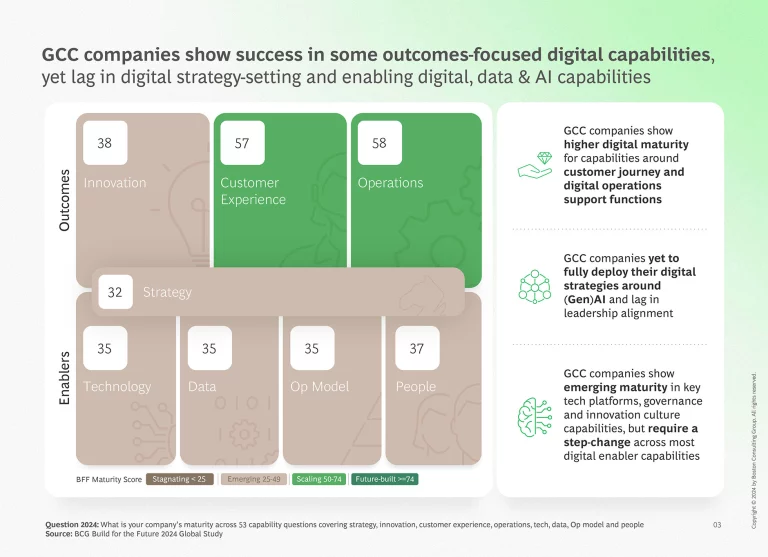

GCC organizations are presented with a unique opportunity and a matching challenge to build on their capabilities to leap into global-level digital and AI maturity. In 2024, GCC organizations show higher maturity around customer journey and digital operations capabilities, however, have yet to fully possess many of the critical enabler capabilities that would allow them to fully deploy their digital and (Gen)AI strategies, and will need a step-change, particularly in their data and technology capabilities.

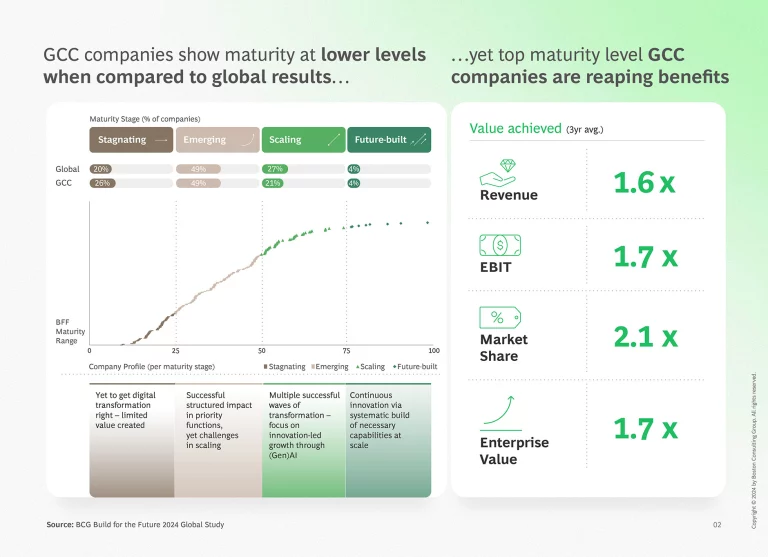

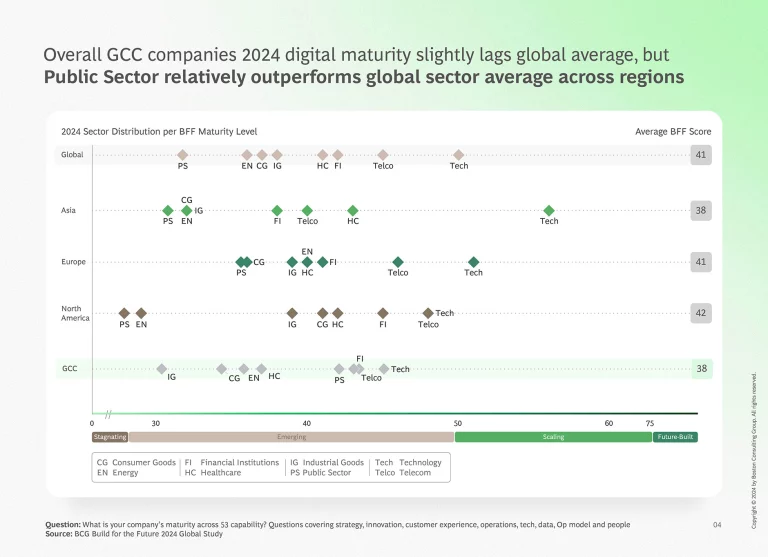

Where fast-changing technology landscapes and rapid AI adoption are paramount to future success, GCC organizations have a tangible opportunity to catch up with their global counterparts at the overall digital maturity level. While 25% of GCC organizations fall into the top two scaling or future-built maturity levels the global share is 31%. At a sector level, the Public Sector in the GCC exhibits key areas at world-class digital maturity levels, while Financial Institutions and Tech companies exhibited the highest digital and AI maturity scores across the GCC. Overall, however, digital and AI maturity in the GCC in 2024 fell behind the global average.

Challenges & Opportunities: GCC Organizations on the Road to AI Value Delivery

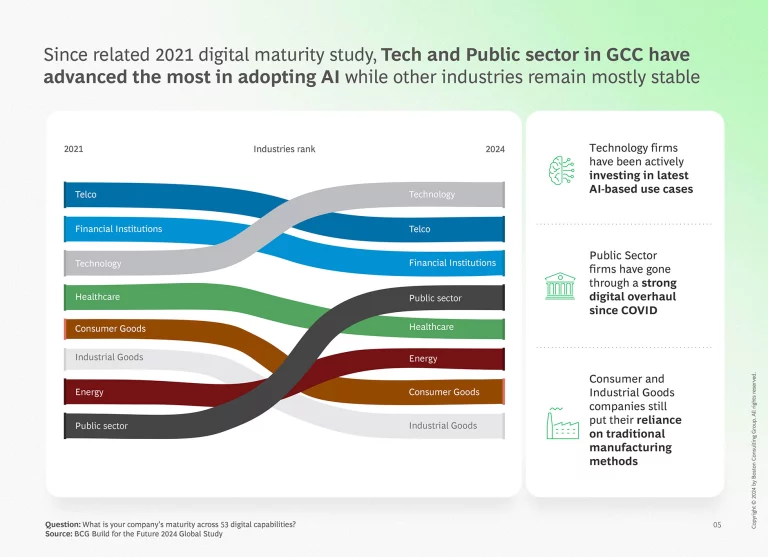

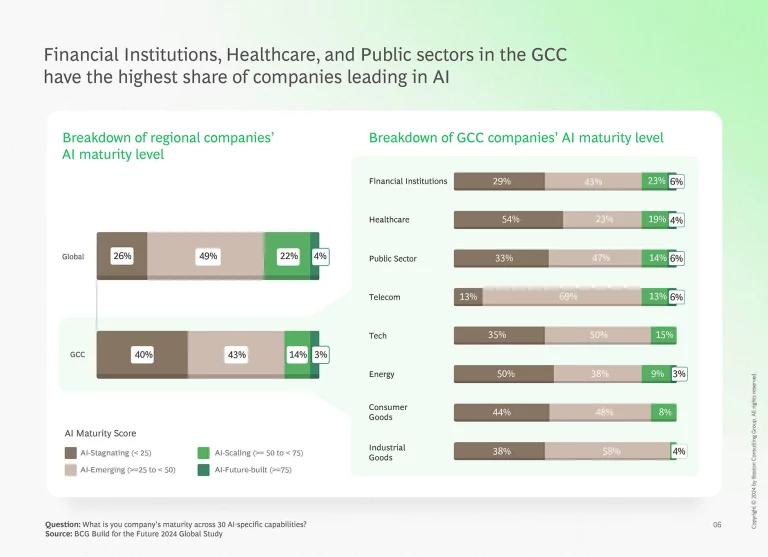

In 2024, 17% of organizations in the GCC scored into the top two AI maturity levels (AI-scaling & AI-Future-Built). In this regard, the Financial Institutions sector had the highest share of top-level AI-maturity

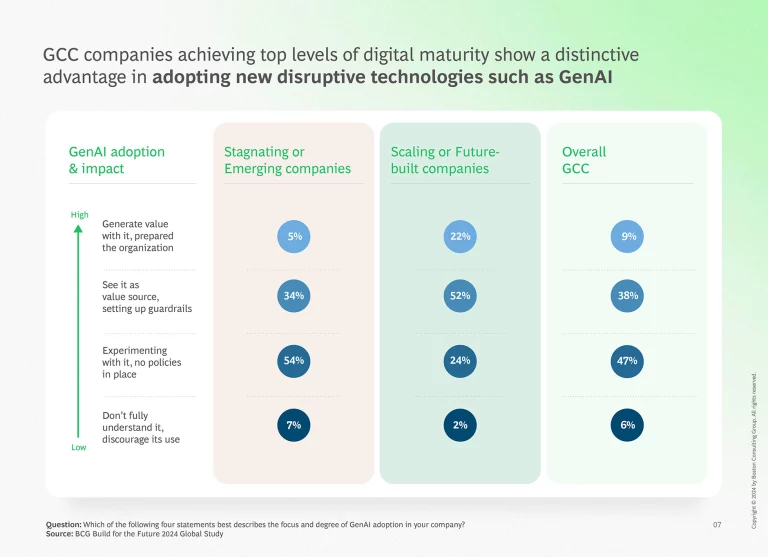

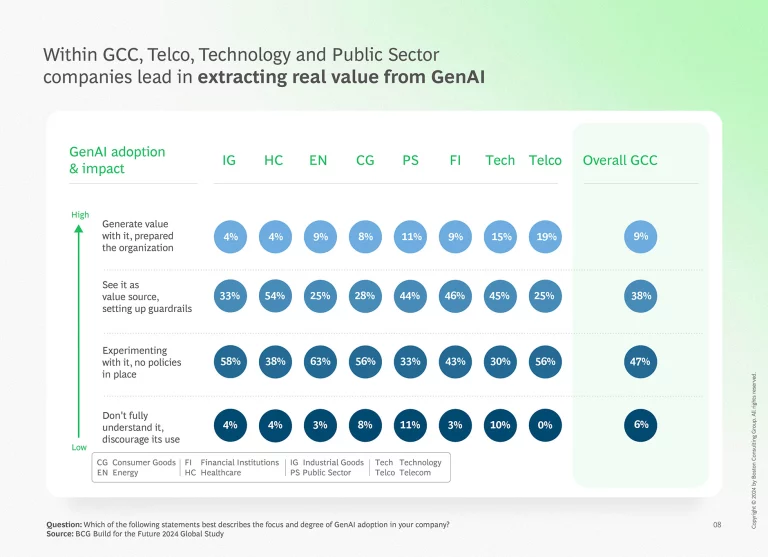

Additionally, our study found that the highest AI maturity organizations have three times the rate of success extracting value from GenAI (more on this below). Yet, the GCC remains at the early stages of (Gen)AI adoption, with only 9% of organizations surveyed at this level of value delivery. Overall half of all organizations surveyed (53%) are either still experimenting with GenAI with no official policies set in place, or not actively using it at all. The remaining (38%) recognize the value of adoption and are planning to scale up with guardrails. Similar to the overall digital and AI maturity trend in the GCC, sectors with highest share of organizations generating value with (Gen)AI are the Public Sector, as well as the Tech and Telco sectors.

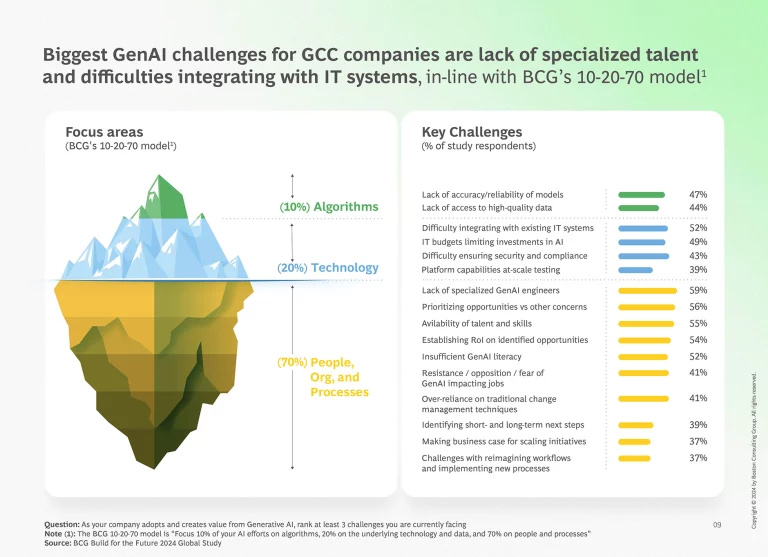

While every AI journey is tailored to each organization, we found common challenges in the region. For instance, 6% of surveyed organizations have expressed not fully understanding GenAI, which lies in the critical need for leadership initiatives to educate and upskill while setting an AI-and People, Org, and Process-first strategy. For organizations further down the line of (Gen)AI adoption, several challenges have been marked across BCG’s. “10-20-70” Algorithm- Technology- and People, Org, and

In fact, the highest share of GCC organizations observed gaps in the people, processes, and organizational dimension as the biggest barriers to AI maturity. This includes limited specialized talent, a gap in overall AI literacy, and a lack of sufficient incentives for innovation and GenAI adoption in working processes. Difficulty integrating AI within exiting IT systems and lack of access to unified and high-quality data further hinders progress.

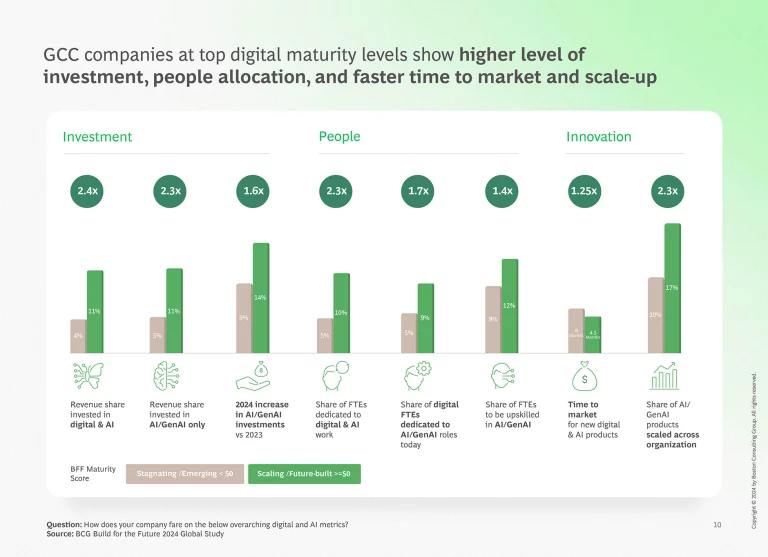

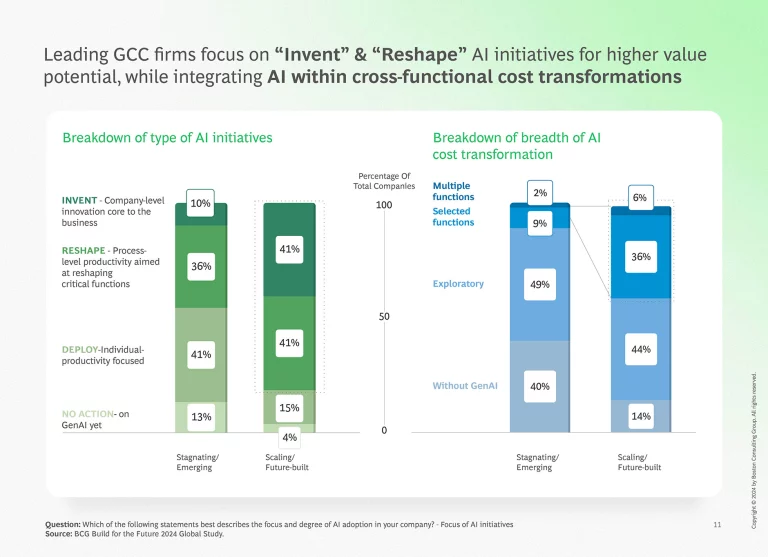

On the other hand, compared to stagnating and emerging organizations, AI leaders have been successful in embedding AI for process-level productivity aimed at reshaping critical business and customer-facing functions as well as at integrating innovation in core corporate functions. To do so, AI leaders in the GCC have focused on key enablers including increased investment and focused budget allocation, as well as digital-first resource planning. High-maturity organizations allocated 2.4x more funding to AI initiatives as well as a 2.3x higher share of FTEs were dedicated to digital & AI transformation, achieving a 1.7x higher share of (Gen)AI products scaled organization-wide and reflecting a long-term commitment to embedding innovation.

Value Makers: Digital & AI-First Strategy for Future-built Organizations

The 2024 BFF study highlights the need for most GCC organizations to progress beyond incremental moves and embrace comprehensive digital and AI strategies to unlock transformative value across sectors. While GCC organizations have made impressive progress in digital and AI capabilities, there remain opportunities to further enhance their maturity levels in critical areas and continue building on their strengths to lead globally in digital transformation and AI adoption.

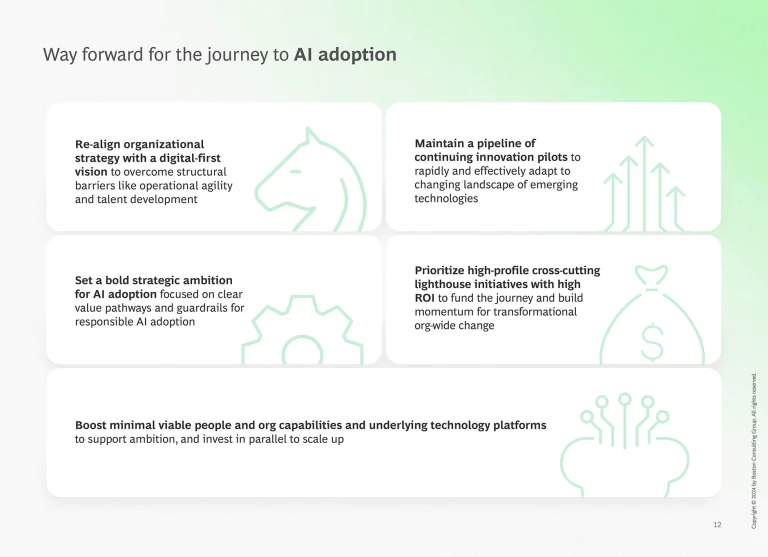

To bridge the global maturity gap and accelerate impact, GCC organizations must embrace a bold, digital & AI-first strategy, across 5 key recommendations:

- Re-align organizational strategy with a digital-first vision to overcome structural barriers like operational agility and talent development.

- Set a bold strategic ambition for AI adoption focused on clear value pathways and guardrails for responsible AI adoption.

- Boost viable people and org capabilities and underlying technology platforms to support ambition and invest in parallel to scale up.

- Maintain a pipeline of continuing innovation pilots to rapidly and effectively adapt to changing landscape of emerging technologies.

- Prioritize high-profile cross-cutting lighthouse initiatives with high ROI to fund the journey and build momentum for transformational org-wide change.

The GCC stands at a crossroads where technological advancements intersect with the region's aspirations to lead in digital and AI innovation. By addressing these priorities, GCC organizations can unlock transformative potential, enabling them to capitalize on emerging opportunities, catch-up to global peers, and earn their position as future-ready pioneers in an increasingly digital world.

The authors are grateful to their BCG colleagues, whose insights and experience contributed to this report. In particular, they thank Marc Roman Franke, Clemens Nopp, Michael Leyh, Vikas Singh, and Lakshay Arora.