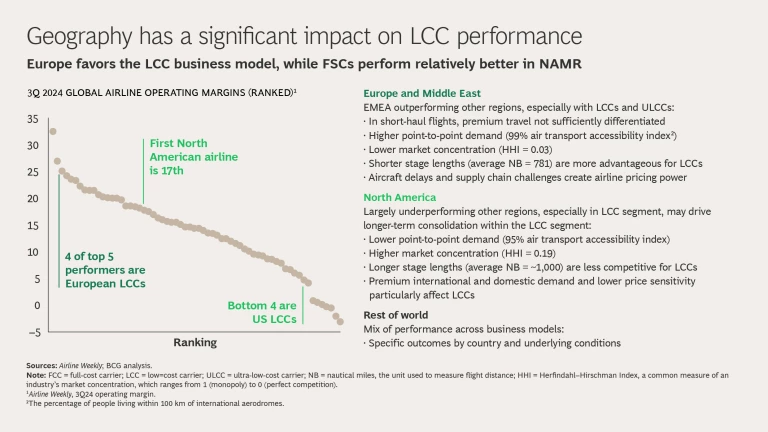

Airlines around the world are emerging from a good recovery year in 2024 and should see steady growth in 2025. Nonetheless, capacity will remain constrained due to delivery delays for airplanes and essential engine parts such as airfoils. Airlines globally share this challenge; however, industry dynamics will vary by region and carrier, with low-cost carriers primarily dealing with higher costs while full-cost airlines look for new growth. (See the slideshow.)

The 2024 State of Play

Despite late 2023 concerns about economic uncertainty, global air travel grew 6.5% in 2024 as international air travel largely returned to prepandemic levels. Growth was accelerated by a drop in fuel prices of about 20%, leading to lower ticket prices and greater demand. Many airlines also invested in top-line growth during the year, with a greater focus on advanced retailing strategies, such as streamlined booking and dynamic pricing.

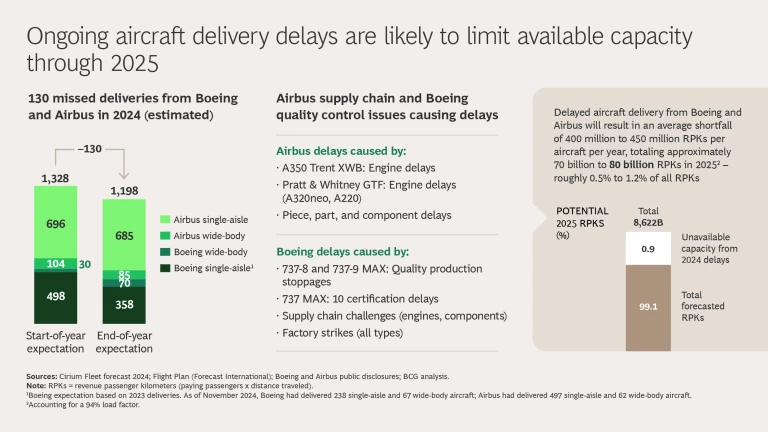

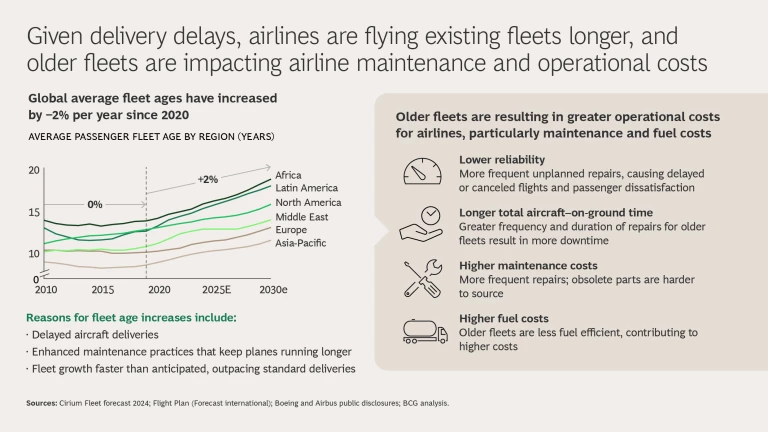

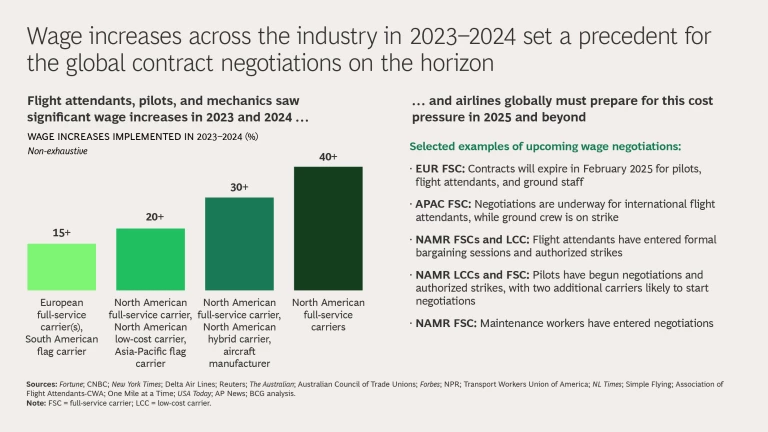

Nonetheless, airlines were hit by several obstacles during 2024, including aircraft delivery delays and wage increases for flight crews and mechanics. In addition, conflict zones limited routes and airspace over Eastern Europe and the Middle East while geopolitical tensions affected international travel growth between North America and Asia.

What 2025 May Hold

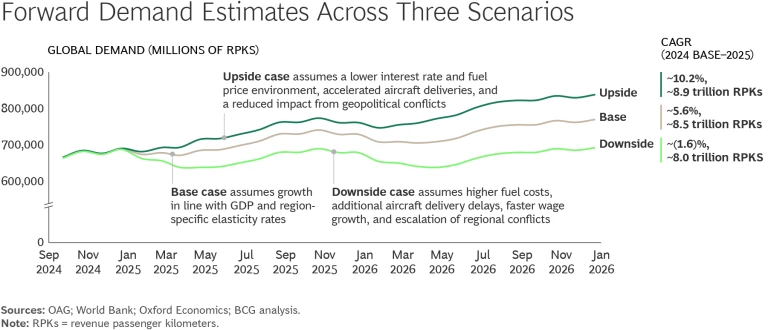

As we look to 2025, we expect similar variables to affect the industry, along with economic factors such as variations in interest rates and GDP growth, all of which contribute to our forward demand estimates for the year. (See Exhibit 1.) (Our analysis was completed in January 2025 and therefore does not include the potential impact of recent tariffs on the industry.)

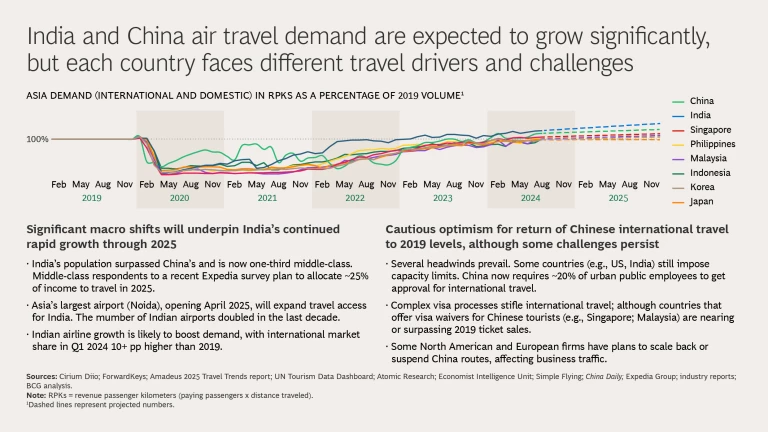

Our base case assumes that air travel will grow at a CAGR of about 5.6%, in line with country- and region-specific GDP forecasts and elasticities. Aircraft and supply chain delivery delays will continue at a similar rate to that seen in 2024, and growth from China and India will maintain its current momentum, with China’s international travel forecasted to finally return to 2019 levels by the year-end. At the same time, wage growth pressures will continue, hurting margins and raising ticket prices.

Our upside case projects growth in air travel at an approximately 10.2% CAGR, spurred by accelerated GDP, lower fuel costs, improved supply chains, and an easing of geopolitical conflicts. More positive economic sentiment will lead to greater stability, with follow-on effects such as lower interest rates and inflation, and wage increases will not materialize as dramatically as expected.

Our downside case, in contrast, estimates a decrease in air travel demand of about 1.6%, arising from fuel price and wage increases along with worsening regional conflicts, global economic uncertainty, and additional delays across aircraft and other supply chain deliveries.

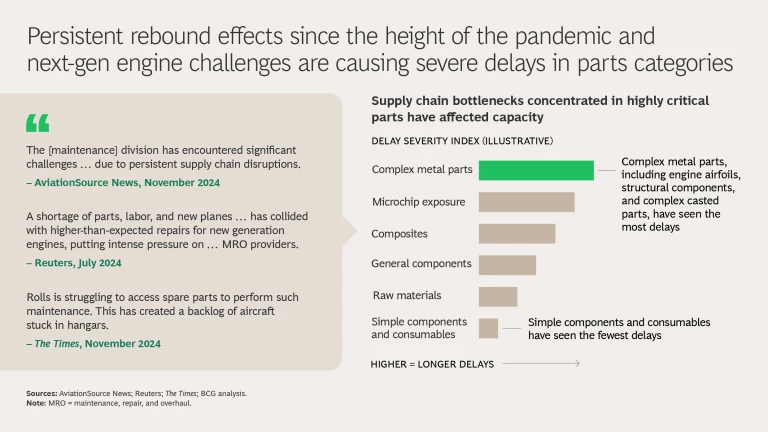

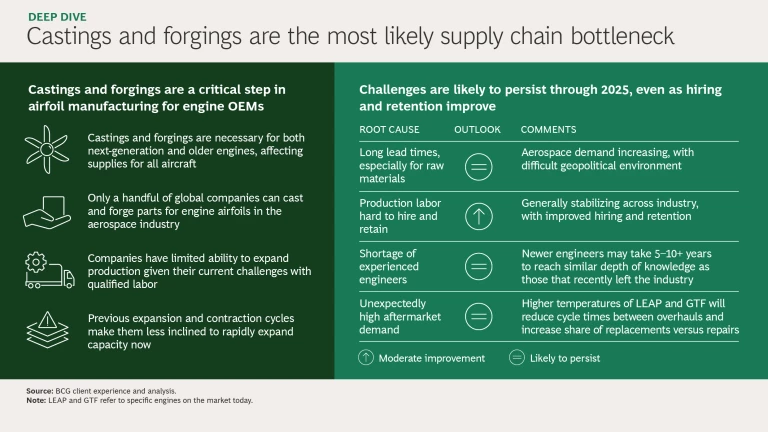

In every scenario, broad supply chain challenges will continue to affect carriers, including ongoing bottlenecks in the casting and forging of airfoils, with follow-on impacts for maintenance, capacity, costs, and pricing.

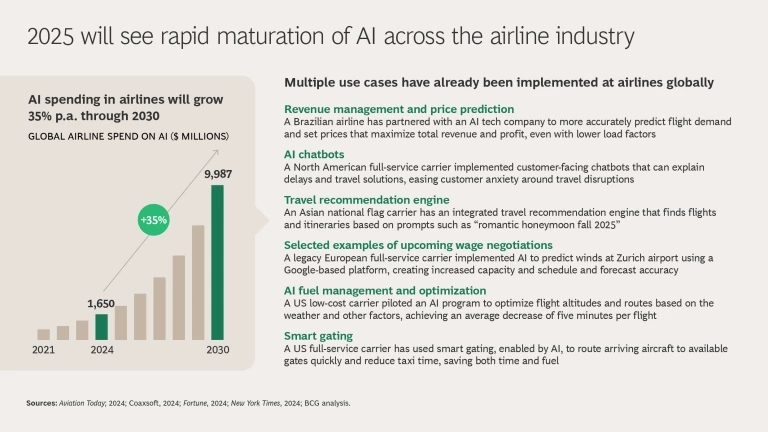

In addition, airlines will continue to grow the use of AI to drive efficiency and customer satisfaction, with spending anticipated to increase 35% per annum through 2030, reaching close to $10 billion. Many airlines have already implemented successful AI use cases, including a US full-service carrier employing smart gating technology and a Brazilian airline partnering with an AI tech company to more accurately predict flight demand.

This thought piece hopes to foster discussion on likely trends and potential disruptions in the year ahead. We hope it will serve as an input to industry leaders as they develop their own perspective on 2025 and refine their commercial and operational plans.